Loading Search...

Learn how tokenization is transforming real-world assets like real estate, art, and bonds into tradable tokens.

Author: Tanishq Bodh

Tokenization is fundamentally transforming how we invest in real-world assets (RWAs). Blockchain now allows us to digitally represent ownership of physical or intangible assets as tokens. These tokens exist on a blockchain. Users can buy, sell, or trade them with the same ease as cryptocurrencies. They unlock new forms of liquidity, allow for fractional ownership, and operate on a transparent, efficient, and global infrastructure.

Think of it this way: if you own a house worth $1 million, you could divide its ownership into 1,000 tokens, each representing 0.1%. Instead of needing to buy the entire house, investors could purchase one or more of these tokens and benefit from any appreciation or rental income. The blockchain records who owns what, enables transactions around the clock, and removes many traditional middlemen and delays.

In this ultimate guide, we’ll cover everything you need to know—from beginner-friendly analogies to the technical backbone, regulatory frameworks, real-world examples, challenges, and where the industry is headed. By the end, you’ll understand why tokenization is not just a passing trend, but a foundational piece of the future financial system.

Tokenization converts ownership of a physical or intangible asset into a digital token that exists on a blockchain. Each token serves as a claim to a share of the asset—just like stock certificates represent company ownership.

Let’s say you own 1 token of a property divided into 1,000 tokens. That token proves you own 0.1% of the property and entitles you to a corresponding share of its income or proceeds. This works similarly to shares in a business but applies to nearly any type of asset.

Two analogies make this concept more accessible:

Historically, we’ve had tools like securitization—REITs, bonds, shares—to pool ownership and make investment accessible. Tokenization is the next evolution. Blockchain makes this process cheaper, faster, more transparent, and available globally. A token transfer takes seconds. Settlement is immediate. Ownership is verifiable by anyone. Markets never close.

Tokenization democratizes finance. With fractional tokens, someone with $100 can invest in a property worth millions. It opens doors that were previously reserved for institutional investors or ultra-wealthy individuals.

Let’s break down the tokenization process step by step:

The first move is identifying the asset—be it a house, bond, gold bar, or intellectual property. To tokenize it legally, it often needs to be housed in a special legal structure, like a Special Purpose Vehicle (SPV) or an LLC. This entity is what investors actually hold shares in through tokens.

Ethereum is the most commonly used blockchain due to its smart contract capabilities, but others like Polygon, Algorand, and Aptos are also popular. The token standard (like ERC-20, ERC-721, ERC-1400, or ERC-3643) determines the behavior and capabilities of the tokens.

Developers write smart contracts to create and manage the tokens. These contracts specify how many tokens exist, how they’re distributed, whether they’re fungible, and what rules govern them. For example, if a $500,000 property is divided into 5,000 tokens, each token represents 0.02% ownership.

If tokens qualify as securities (as many RWA tokens do), compliance mechanisms must be built in. This includes KYC/AML verification, investor whitelisting, and restricting transferability to only approved parties. Standards like ERC-1400 and ERC-3643 were designed specifically to embed these features.

Once minted, tokens are sold to investors. This can be done via a private offering, crowdfunding platform, or public sale—depending on local laws. Investors receive the tokens in their crypto wallets, granting them ownership rights.

While tokens live on-chain, the physical asset still needs managing. Property managers collect rent, banks pay bond interest, or asset custodians handle physical gold. These revenues can be automatically distributed to token holders via smart contracts.

Investors can trade tokens peer-to-peer or on secondary markets, depending on legal permissions. This brings liquidity to assets that are traditionally hard to sell in part—like a single apartment or a painting. Settlement happens in seconds, and tokens can be used as collateral or integrated into DeFi platforms.

The combination of blockchain (for record-keeping and transparency) and smart contracts (for enforcement and automation) ensures the system is secure, fast, and highly programmable.

Tokenization isn’t just about technology—it’s a collaborative effort involving:

Why It Matters: Institutional adoption hinges on this infrastructure. For example, BlackRock’s BUIDL fund (tokenized Treasuries) uses Securitize for compliance, demonstrating how traditional finance is merging with crypto.

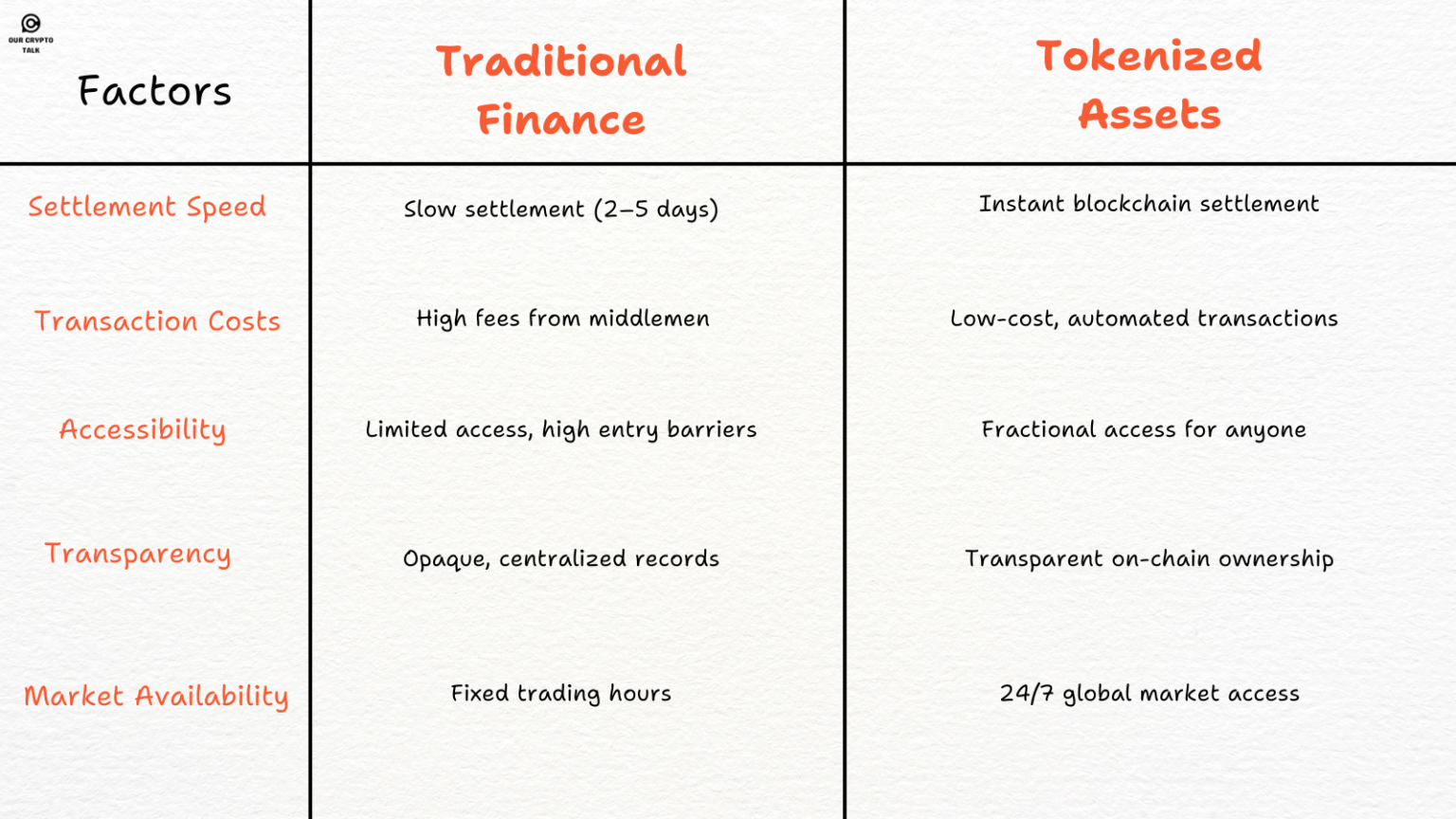

| Factor | Traditional Securitization | Tokenization |

|---|---|---|

| Settlement Time | 2–5 days (T+2 standard) | Seconds |

| Cost | High (underwriting, legal fees) | Low (automated smart contracts) |

| Fractional Ownership | Limited (e.g., REITs at $1k+) | Micro-fractions (e.g., $10 stakes) |

| Transparency | Opaque (trust-based audits) | On-chain verifiability |

| Market Hours | 9 AM–5 PM, weekdays | 24/7 global trading |

Example: A $10M commercial property securitized via REITs requires a syndicate of banks. Tokenized on Ethereum, the same property could be split into 10M tokens ($1 each), traded globally with instant settlement.

Smart contracts don’t just mint tokens—they encode legal rights:

Limitation: “Oracles” (e.g., Chainlink) are needed to verify off-chain events (e.g., property damage affecting token value).

Platforms like RealT and Propbase let investors buy fractional shares of rental properties. RealT focuses on the U.S. market, paying rental income in stablecoins directly to token holders. Propbase operates in Southeast Asia and uses the Aptos blockchain to tokenize new real estate developments with investment minimums as low as $100.

Over $1 billion in U.S. Treasury notes have been tokenized on public blockchains. Ondo Finance’s OUSG and Matrixdock’s STBT are two examples. These tokens offer exposure to government bonds with daily interest payouts—giving crypto-native users access to safe, yield-bearing instruments.

Companies like Swarm and Backed Finance tokenize shares of public companies, enabling 24/7 trading and fractional ownership. Private companies and funds are also issuing security tokens to broaden access to their equity.

Tokens like PAXG and XAUT represent actual gold, with each token backed 1:1 by physical bullion. Holders benefit from the price of gold and can trade the tokens instantly—far easier than shipping gold bars.

High-end art, vintage cars, and music royalties are being tokenized. In one instance, a Picasso painting was divided into 4,000 tokens sold to investors. Sports tokens, wine, and even NFTs representing ownership of physical luxury items are also emerging use cases.

These real-world examples highlight how tokenization is already disrupting traditional finance, art, and real estate—bringing efficiency, access, and liquidity to assets that were once out of reach for most.

These projects aren’t theoretical—they’re live, regulated, and proving that tokenization isn’t just a buzzword. It’s already changing how we invest, own, and trade real-world assets.

Tokenization is reshaping traditional finance by making investments more accessible, efficient, and globally connected. Here’s why it’s generating so much buzz:

Traditionally, high-value assets like real estate, fine art, or luxury goods were reserved for the ultra-wealthy or institutional investors due to their expensive price tags. Platforms like RealT and Propbase have dropped minimum investments to $50–$100, letting retail investors enter markets traditionally reserved for millionaires.

In fact, RealT’s average investment per user is just $137, based on 2024 internal data.

Real estate, fine art, and collectibles are traditionally considered illiquid because selling them can take time and effort. Tokenization allows these assets to be divided into smaller, tradable fractions, increasing liquidity. An individual can now buy and sell parts of assets like they would stocks, making investments more liquid and accessible. For example, a property worth millions can be broken down into thousands of tokens, each representing a share of ownership, which can be traded on the blockchain. Tokenized real estate secondary markets like tZERO saw a 70% year-over-year rise in trading volume in 2024, showing growing liquidity even in previously “frozen” asset classes.

Traditional financial markets often involve delays in transaction processing and settlement times, which can take several days. Tokenized assets, however, benefit from blockchain’s speed. Transactions can be completed in seconds, and settlements are instantaneous, significantly reducing the time and effort involved in transferring ownership.

Traditional property deals take 30–60 days to close.

Tokenized real estate transactions on Ethereum platforms settle ownership in less than 10 minutes, according to 2024 research by Security Token Advisors.

This speed is crucial for enhancing efficiency and supporting the 24/7 global markets.

Traditional financial markets have operating hours, and investors are limited to trading during specific times. However, tokenized assets are traded on the blockchain, which is accessible anytime, anywhere. While stock markets operate 30–35% of the week, tokenized asset platforms like ADDX and OpenFinance Network offer continuous, global trading — matching DeFi’s always-on culture.

Blockchain technology offers an immutable and transparent ledger that records every transaction made on the network. This feature ensures that all asset transfers are publicly verifiable, preventing fraud and providing investors with confidence in the accuracy of ownership records. In a 2024 PwC study, 88% of institutional investors cited lack of transparency as a major barrier to investing in alternative assets. Tokenization directly addresses this gap with real-time auditability.

This level of transparency is a game-changer in a world where trust has historically been a barrier to wider adoption.

One of the most powerful features of tokenization is its programmability. Smart contracts—automated self-executing contracts with predefined terms—allow for automated payouts, governance decisions, and regulatory compliance. For example, token holders can automatically receive dividends from a property or art asset without the need for manual processing, and governance decisions can be made via decentralized voting protocols.

Tokenized assets can be accessed by anyone with a crypto wallet, breaking down geographical barriers and enabling investors from all over the world to participate in the same market. This global reach is especially significant for assets that are traditionally difficult to access, such as prime real estate in certain countries or highly exclusive art collections.

Tokenization reduces the need for intermediaries like brokers, banks, or custodians, which often add substantial fees to traditional investments. By eliminating or reducing these intermediaries, tokenization lowers transaction costs, making it more affordable to invest in high-value assets. This reduction in costs is a direct benefit to investors, who can retain more of their returns.

Despite its potential, tokenization comes with several challenges and risks that investors need to consider:

Security tokens are subject to a wide range of regulations, and the legal landscape is still evolving. In the U.S., there are strict regulations around tokenized securities, and failure to comply can lead to penalties or legal action. Meanwhile, Europe is working on more flexible frameworks for tokenized assets, but the overall regulatory environment is still fragmented. As such, the uncertainty around how tokenized assets will be regulated is a major hurdle that must be overcome to ensure widespread adoption.

Tokenization platforms are not immune to fraud. Since tokenized assets are digital, it’s critical to ensure that the tokens are backed by the assets they represent and that the platforms are legitimate. Scams can occur, especially in the early stages of the tokenization market, where regulatory oversight may be lacking, and some projects may not provide the transparency they promise. Investors must exercise due diligence and verify the credibility of the platform before engaging in tokenized investments.

The backbone of tokenization lies in smart contracts, which are self-executing pieces of code that automate transactions. However, these contracts are not infallible. Bugs or flaws in smart contracts can be exploited by hackers, potentially leading to loss of funds. Without proper auditing, vulnerabilities can put investor assets at risk. As the industry grows, ensuring the robustness of these contracts through rigorous testing and third-party audits will be critical.

While tokenized assets promise increased liquidity, many tokens may lack active secondary markets, especially in the early stages. This means that investors could face challenges when trying to sell or trade their tokens if there is insufficient demand. This is particularly true for niche markets or newly tokenized assets that have not yet gained widespread adoption. Liquidity concerns can make tokenized assets less attractive to investors looking for more immediate returns.

Although blockchain provides an immutable record of transactions, legal recognition of tokenized ownership can be problematic in certain jurisdictions. In some cases, ownership of tokenized assets may not be recognized by courts unless it is explicitly tied to traditional legal contracts or paperwork. This lack of legal enforceability could make it difficult for token holders to assert their rights in case of disputes, limiting the potential of tokenization as a fully-fledged legal framework for asset ownership.

The integration of traditional financial systems with blockchain technology is still in its infancy. Many traditional brokers, banks, and regulators are struggling to adapt to the new digital infrastructure that tokenization requires. This disconnect creates friction in the market and can hinder the widespread adoption of tokenized assets. Until there is seamless integration between the old and new systems, tokenization may face challenges in gaining mainstream acceptance and scaling efficiently.

In the U.S., the SEC views most RWA tokens as securities, meaning they must be registered or exempted. This limits public trading and adds compliance burdens. Several licensed ATS platforms have emerged to fill this gap.

Europe’s MiCA law doesn’t cover securities but applies to crypto assets broadly. The DLT Pilot Regime allows tokenized securities to trade under sandbox conditions. Switzerland has a dedicated legal framework for digital assets, while Singapore and the UAE are fostering innovation with clear rules.

Overall, regulators worldwide are moving toward frameworks that support tokenization while safeguarding investors. Countries that strike the right balance could become global hubs.

Tokenized RWAs rely on stablecoins for:

Future: ECB’s digital euro could enable compliant settlements for EU tokenized assets, bridging TradFi and crypto.

Pros: Democratizes access (e.g., Kenyan farmers tokenizing land).

Cons:

Counterpoint: Proper regulation (e.g., MiCA’s transparency rules) can mitigate risks.

Tokenization is more than a crypto innovation—it’s a financial revolution. It brings transparency, access, and efficiency to asset ownership on a global scale. The implications stretch across capital markets, real estate, insurance, collectibles, and beyond.

Much like the internet transformed communication, tokenization is set to transform value exchange. We are witnessing the early stages of a multi-trillion-dollar industry that could redefine how the world invests.

Whether you’re a retail investor, builder, or institution, now is the time to learn, explore, and prepare. Token by token, the future of finance is being built—and it’s arriving faster than most expect.

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?