Loading Search...

FTX saga explained, examining Sam Bankman-Fried’s claims that the exchange was never bankrupt and what the evidence really shows.

Author: Tanishq Bodh

Few collapses in crypto history rival the scale and shock of the FTX saga. In November 2022, one of the largest centralized exchanges imploded in a matter of days, wiping out billions in user funds and shattering trust across the industry. The narrative seemed settled. Fraud. Mismanagement. Insolvency. Prison.

Then, in February 2026, Sam Bankman-Fried reignited the debate.

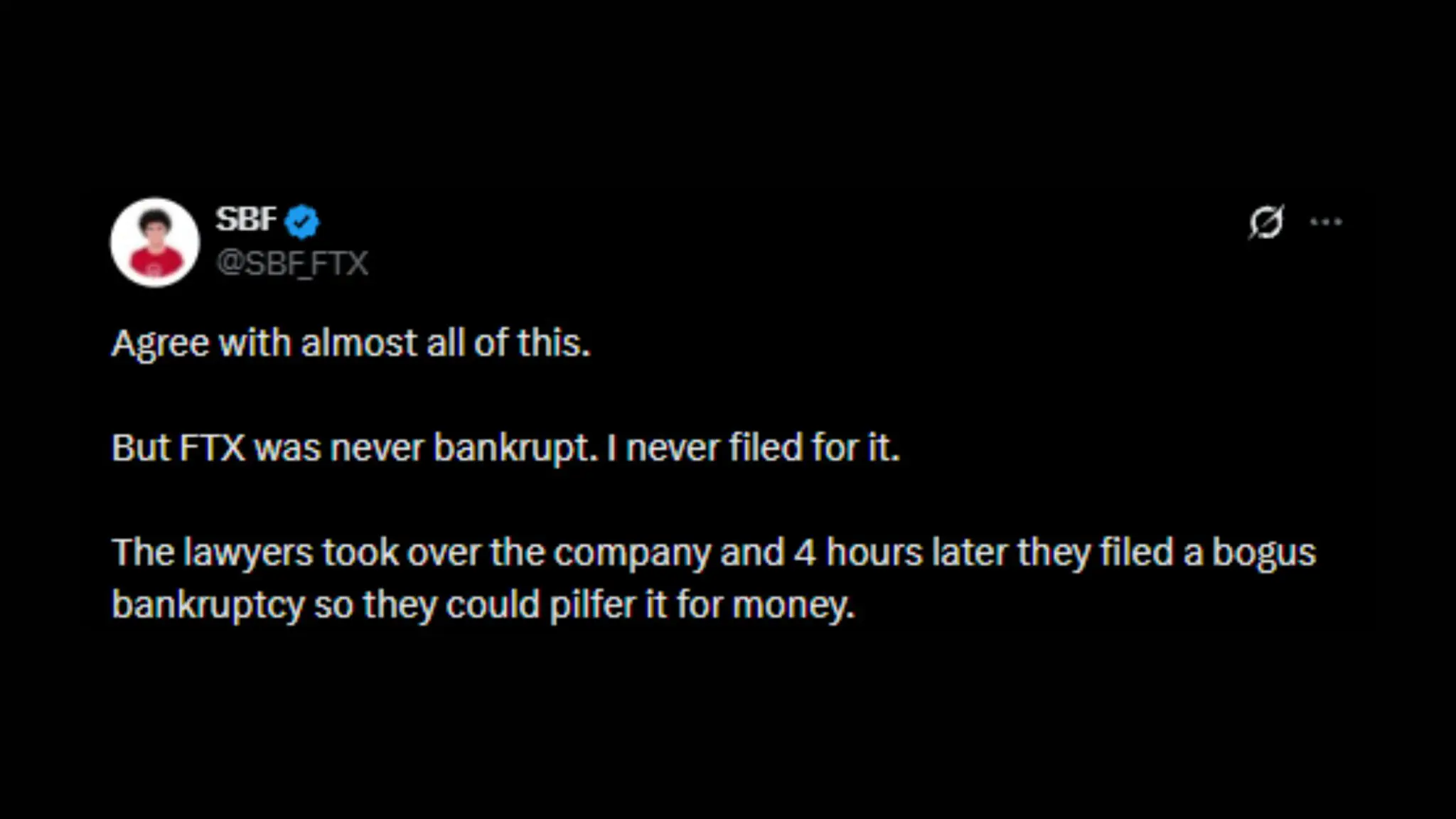

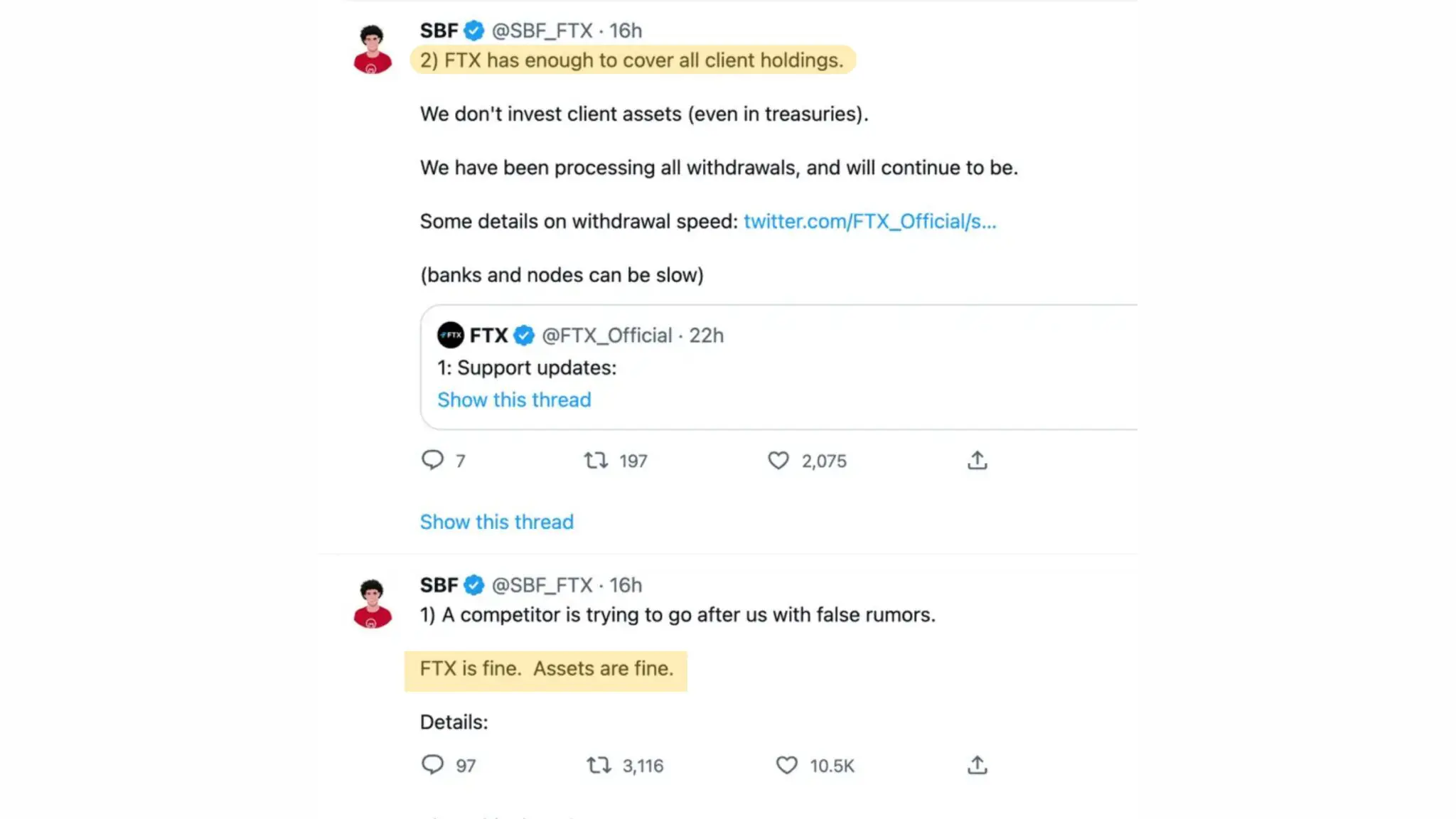

From prison, SBF claimed that FTX was never bankrupt. He argued that he never filed for bankruptcy, that the company was solvent, and that lawyers rushed a Chapter 11 filing to seize control and extract fees. According to him, the collapse was a liquidity crisis, not insolvency.

These claims resurfaced amid a changing political backdrop, partial creditor repayments, and renewed scrutiny of the legal process. They raise an uncomfortable question for crypto and regulators alike.

Was FTX truly bankrupt, or was it forced into bankruptcy while still solvent?

This explained article unpacks the full FTX saga through that lens. We examine SBF’s claims, the evidence supporting and contradicting them, and what the case reveals about crypto, law, and financial collapses in the digital age.

At the core of the renewed controversy is a simple assertion.

FTX, according to SBF, had more assets than liabilities at the time of collapse.

In multiple statements from late 2025 through February 2026, he argued that FTX held roughly $25 billion in assets against approximately $13 billion in liabilities before withdrawals froze. He cited internal balance sheets, venture investments, and token holdings, including FTT, as proof.

Also claimed that customer funds were not stolen but temporarily lent to Alameda Research under a margin framework and he described the shortfall as an accounting and liquidity mismatch rather than fraud.

Most controversially, SBF blamed the bankruptcy process itself. He accused Sullivan & Cromwell of pushing a rushed Chapter 11 filing within hours of taking control. According to him, this decision destroyed value, forced asset liquidations at market lows, and generated hundreds of millions in legal fees.

In his telling, FTX could have survived without bankruptcy, much like Bitfinex did after its 2016 hack.

To assess whether FTX was ever truly bankrupt, the timeline matters.

FTX grew rapidly between 2019 and 2022 by offering crypto derivatives, leveraged trading, and deep liquidity. Alameda Research, SBF’s trading firm, operated closely alongside the exchange.

That proximity became fatal.

In early November 2022, a CoinDesk report revealed Alameda’s balance sheet relied heavily on FTT, a token issued by FTX itself. This raised concerns about circular collateral and leverage.

When Binance announced it would sell its FTT holdings, confidence evaporated. Users withdrew more than $6 billion in days. FTX could not meet redemption demands.

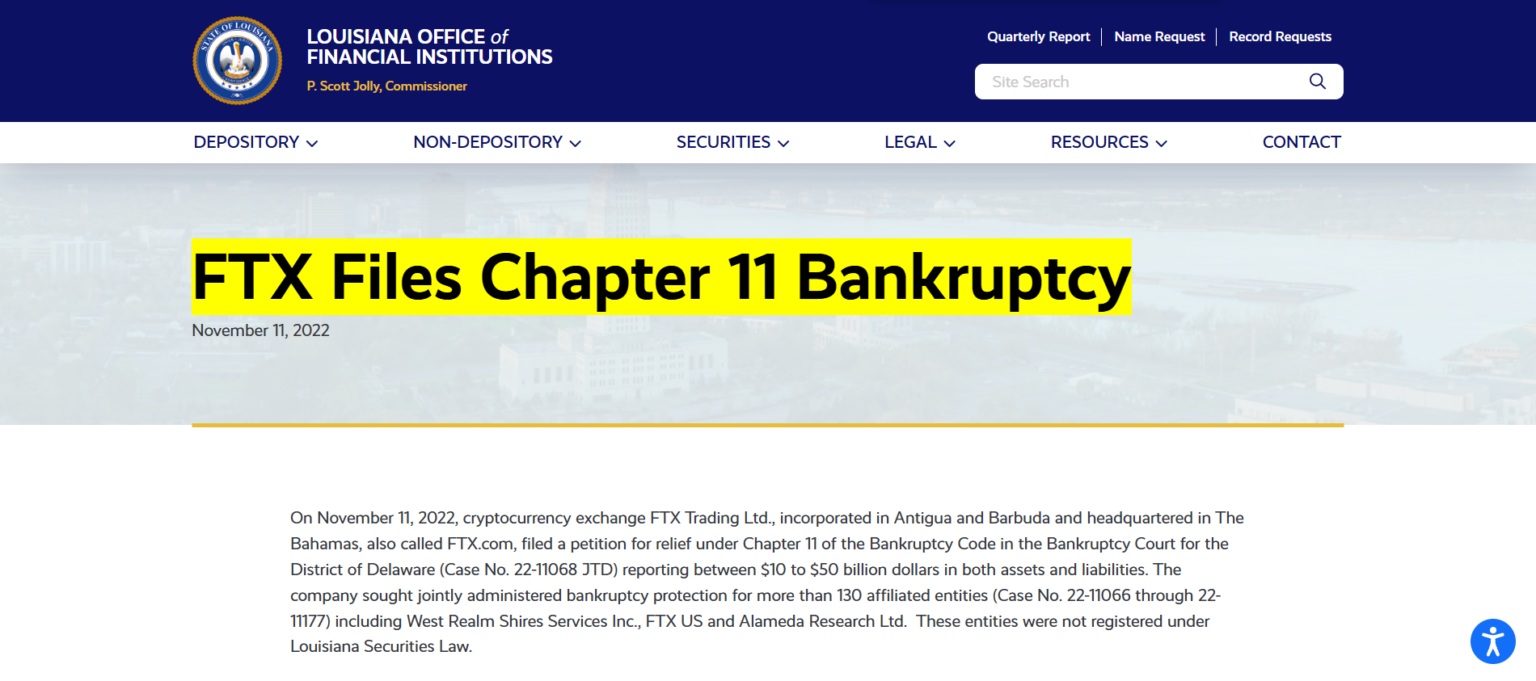

On November 11, 2022, FTX filed for Chapter 11 bankruptcy.

SBF maintains that the exchange failed due to a classic bank run. Critics argue that the run exposed structural insolvency caused by commingled funds and hidden leverage.

Much of the debate hinges on definitions.

A company becomes insolvent when liabilities exceed assets. A company faces a liquidity crisis when it cannot meet short-term obligations despite having valuable assets.

SBF claims FTX suffered the latter.

Evidence exists that FTX held large venture stakes, tokens, and receivables that were illiquid but potentially valuable. Years later, the bankruptcy estate recovered enough assets to repay most customers in full, with some receiving more than 100 percent of claims.

This recovery fuels SBF’s argument that insolvency never existed.

However, prosecutors and the court focused on something else.

They argued that FTX used customer funds without consent, regardless of solvency. That act alone constituted fraud, even if assets eventually exceeded liabilities.

In short, solvency does not excuse misuse.

The criminal case against SBF did not hinge on whether FTX could have recovered.

It focused on intent, misrepresentation, and control.

Prosecutors showed that SBF authorized Alameda Research to draw on FTX customer funds without disclosure. Witnesses testified that risk controls were bypassed. Financial records lacked basic safeguards.

The court accepted the testimony of insiders who described deliberate decisions, not accounting errors.

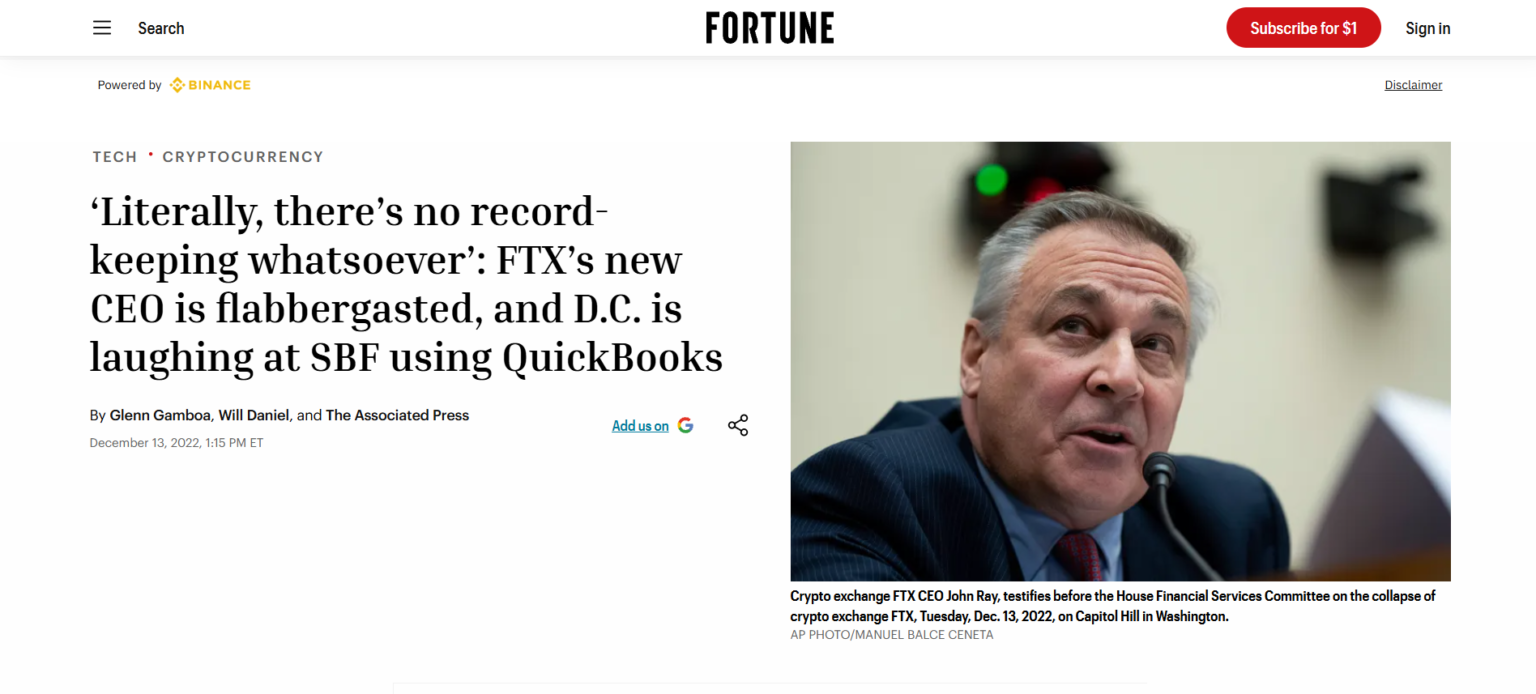

FTX’s new CEO, John Ray III, described the situation as a complete failure of corporate controls. He testified that he had never seen such chaos in his career.

The jury convicted SBF on all major counts. He received a 25-year sentence.

From a legal standpoint, the question of bankruptcy timing mattered less than the breach of trust.

Ironically, the bankruptcy process strengthened parts of SBF’s narrative.

By 2024 and 2025, the estate recovered more than $16 billion through asset sales, clawbacks, and litigation. Rising crypto prices helped. Venture stakes rebounded.

Most customers were made whole, and some received excess payouts.

Supporters argue this proves FTX saga was vague and FTX was never truly insolvent. Critics respond that recoveries do not retroactively legalize fraud.

Both can be true.

FTX may have had enough assets in theory, but mismanagement and secrecy made those assets inaccessible when users needed them most.

The numbers tell a complex story, not a simple one.

The FTX saga explained through the bankruptcy question exposes deeper issues.

First, crypto exchanges operated without clear safeguards. Liquidity risk and custody risk blurred together.

Second, bankruptcy law moves fast in crises, sometimes destroying value to preserve order.

Third, public narratives often oversimplify. Fraud and solvency are not mutually exclusive.

For crypto, the lesson is painful but clear. Transparency, segregation of funds, and governance matter more than balance sheet size.

Was FTX ever truly bankrupt?

In hindsight, the answer depends on perspective.

From an accounting standpoint, assets may have exceeded liabilities and from a legal standpoint, customer trust was broken long before the bankruptcy filing and from a market standpoint, confidence collapsed faster than assets could be realized.

SBF’s claims force an uncomfortable reexamination of how financial failures unfold in crypto. They do not erase wrongdoing. They do complicate the story.

As crypto matures, the FTX saga will remain a reference point. Not just for fraud, but for how liquidity, law, and panic intersect in digital markets.