Loading Search...

The Binance Effect reversed completely. 98% of tokens dump post-listing. Here's what killed this pump signal.

Author: Tanishq Bodh

A few years ago, getting listed on Binance was the closest thing crypto had to a guaranteed pump. Traders would front-run the announcement. Prices would spike on the news. Retail piled in. Everyone went home happy, or at least most people did. That era is over. Not slowly, not quietly, and not because of one bad cycle. The data has been screaming this for over a year now. The Binance Effect, one of the most cited phenomena in crypto market behavior, has not just weakened. Instead, it has structurally reversed. And the people who haven’t figured that out yet are the ones funding the exits of the people who have.

Understanding the Binance Effect reversal isn’t just about avoiding bad trades. Rather, it’s about recognizing that the most powerful listing signal in crypto has become a contrarian sell indicator. The announcement that once meant validation now signals an exit ramp for insiders. Consequently, retail investors who still believe in the old playbook are getting systematically destroyed.

This isn’t revisionism. The Binance Effect genuinely existed, and researchers documented it thoroughly. A 2023 analysis tracking 26 tokens over 18 months found that prices surged an average of 41% within the first 24 hours of a Binance listing. Within 30 days, tokens were hitting peaks averaging 73% above their listing price. Individual examples were even more dramatic. For instance, Stargate Finance’s STG surged 152% on its first day of listing in August 2022.

The logic was straightforward. Binance controls somewhere between 36% and 38% of all global CEX trading volume, more than its next several competitors combined. When a token got listed there, it gained exposure to the deepest pool of retail liquidity in the world, overnight. Analysts at Messari described it as a function of Binance’s easy-to-use UX acting as a simple gateway for both crypto natives and newcomers to access a token, combined with the exchange’s sheer volume creating instant price discovery.

A Binance listing meant you had made it. It represented validation, liquidity, and a catalyst, all packaged in a single announcement. The Coinbase Effect had been the dominant version of this idea in 2021. However, by 2023, researchers were confirming that the Binance Effect had surpassed it. The transition felt natural. Binance had the volume, the global reach, and the community engagement that Coinbase simply couldn’t match outside the US.

Then 2024 happened, and the data started telling a very different story about the Binance Effect.

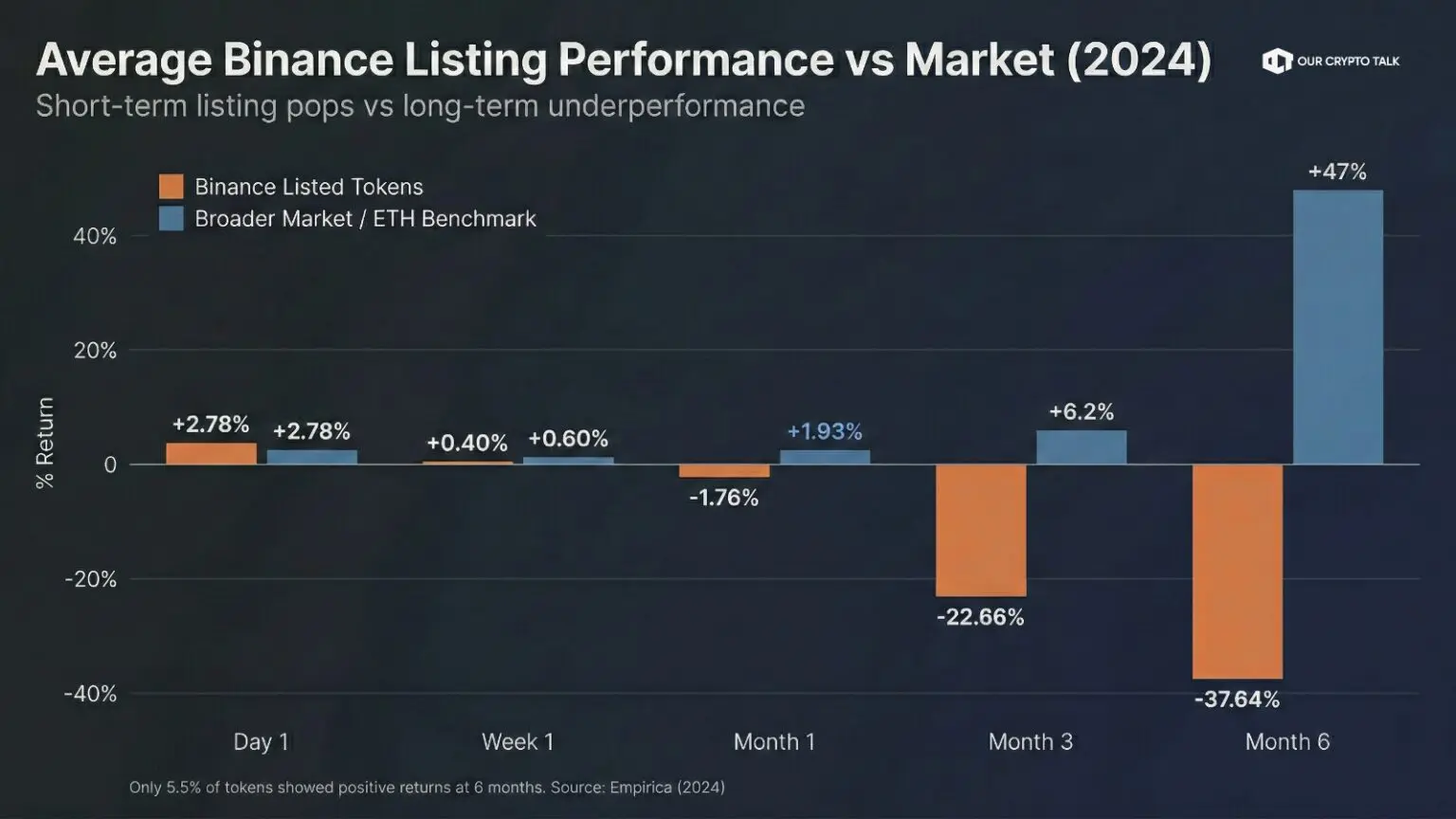

Researchers at Empirica ran a comprehensive analysis of every Binance listing in 2024. The results were not ambiguous, and they revealed the complete Binance Effect reversal.

The average return the day after listing reached just +2.78%. After one week, it dropped to +0.40%, after one month, it fell to -1.76%. After three months, it plunged to -22.66%. Finally, after six months, it crashed to -37.64%.

Only 5.5% of tokens that completed six months of trading showed positive returns. Moreover, just one token in the entire 2024 cohort outperformed the broader market on a relative basis.

To put that in context, Bitcoin went from $42,000 to nearly $70,000 over the same period. The broader market was in an upswing. Yet newly listed tokens on the world’s largest exchange were, as a category, going down. The Binance Effect had not just weakened. It had inverted.

The Empirica analysis went further. When they looked at all 500+ tokens listed on Binance since the exchange’s founding, the six-month performance trailed the market by an average of 39.46%. Meaning if you had invested equal amounts into every single Binance listing since inception and held for six months, you would have dramatically underperformed simply holding ETH.

A separate study by CryptoNinjas and Storible analyzed 389 tokens listed across major CEXs in 2024. Their headline finding confirmed the Binance Effect reversal: 98% of Binance-listed tokens dump after the initial pump. The typical sequence runs as follows: a 54% price surge at listing, followed by an average 52% decline. And 37% of tokens hit their all-time high on the day of listing and never recover it.

The listing had become the peak. Not the launchpad. The Binance Effect had transformed from a buy signal into a distribution event.

Here is the part retail was not supposed to figure out, at least not this quickly. The Binance Effect reversal happened because the listing mechanism changed from a market discovery event to a coordinated exit strategy.

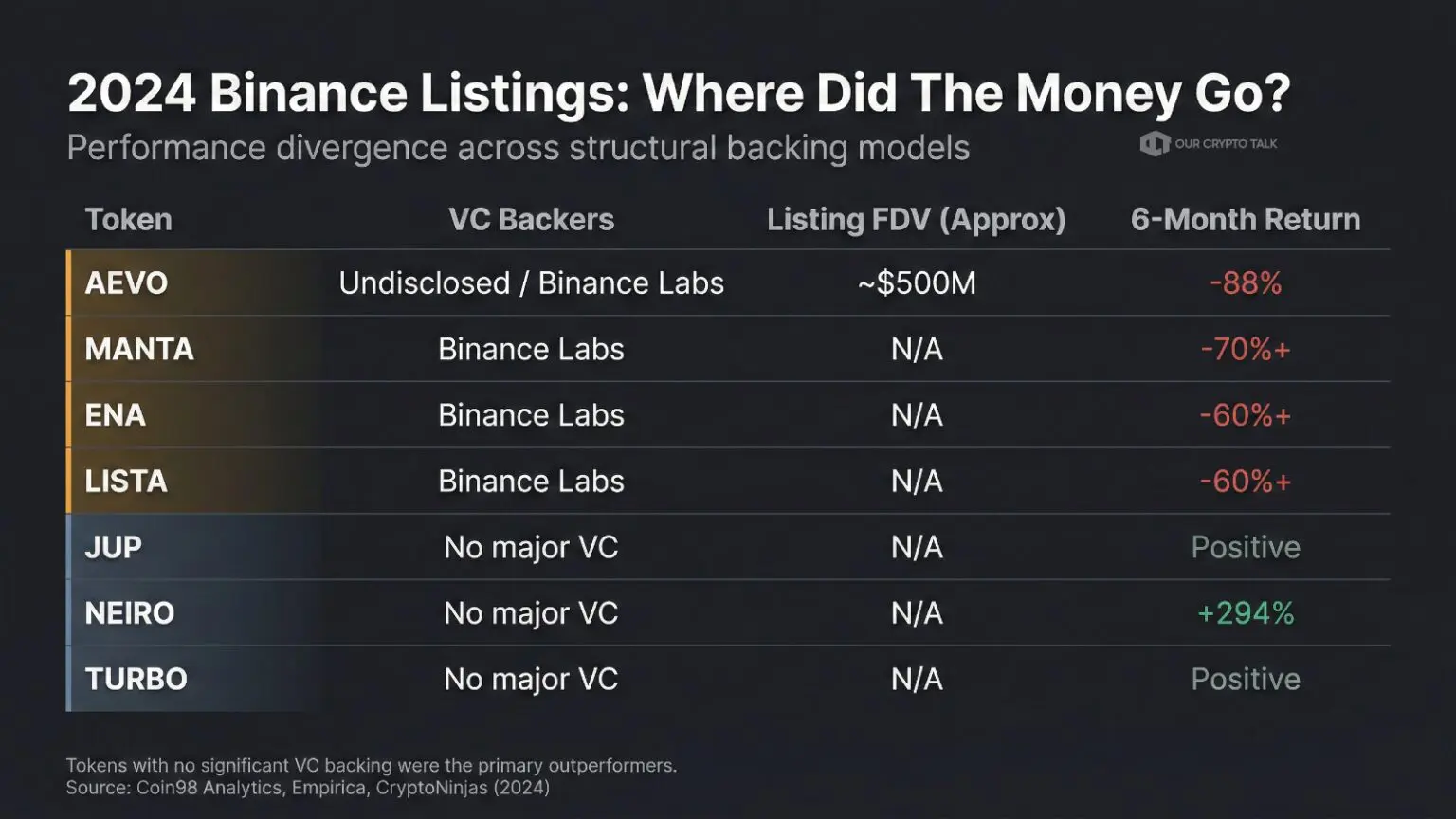

Researcher Flow analyzed 31 recently listed Binance tokens and found only 5 had seen price increases after listing. Those five were almost exclusively meme coins or projects with no significant venture capital backing. The rest followed a more structured script.

Projects would raise funding from tier-one VCs at early-stage valuations. They would then list on Binance at a fully diluted valuation averaging over $4.2 billion, in some cases reaching $11 billion. Retail, seeing the Binance badge and the announcement, would buy in. Meanwhile, the VCs, holding tokens they acquired at a fraction of the listing price, would sell into that retail liquidity.

Dragonfly’s Haseeb Qureshi described it bluntly in mid-2024: teams and VCs owned between 30% and 50% of token supply on many of these projects. When retail investors collectively realized that, around April 2024, they began exiting not just the tokens but the entire VC-backed narrative category en masse.

Researcher Flow put it plainly: “Most new Binance listings are not investment vehicles anymore. All their upside potential is already taken. They represent exit liquidity for insiders who capitalize on retail’s lack of access to quality early investment opportunities.”

The Binance listing was not the beginning of the trade. Instead, it was the end of theirs. This dynamic explains the core mechanism behind the Binance Effect reversal.

Tokens backed by Binance Labs itself, including MANTA, AXL, ENA, REZ, BB, and LISTA, fell between 44% and 90% from their listing prices. Similarly, tokens backed by a16z, Paradigm, Coinbase Ventures, Galaxy, and Pantera showed similar patterns. The prestige of the backer did not help. In some cases, it made the dynamic worse, because those names attracted more retail participation.

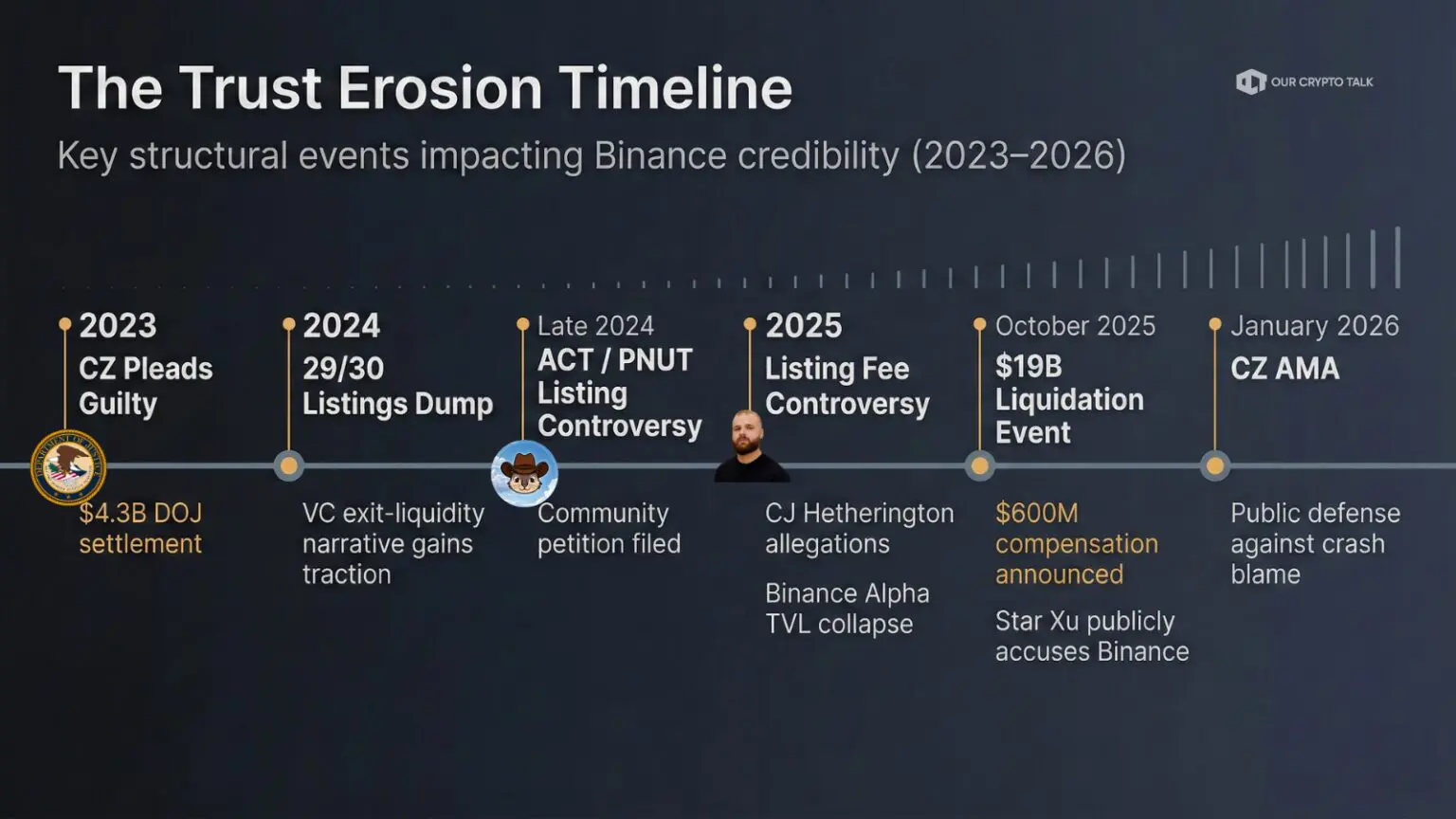

For years, the economics of getting listed on Binance existed in a kind of enforced silence. NDAs were standard. Founders who spoke about terms did so anonymously, if at all. Then, in late 2025, a founder named CJ Hetherington changed that.

Hetherington, founder of a prediction market project on Base called Limitless Labs, went public with the terms Binance had reportedly offered him, before they had even asked him to sign a confidentiality agreement. According to his account, Binance demanded 8% of the total token supply, plus a multi-million-dollar security deposit, as the conditions for listing.

Binance responded quickly, denying it profits from listings, accusing Hetherington of leaking confidential communications, and signaling potential legal action. The exchange maintained that any tokens received are returned to the ecosystem through airdrops, user incentives, or refunds.

However, the conversation was already public, and Hetherington was not alone. Multiple founders had been saying similar things off the record for months.

Third-party estimates now place the 2025 Binance listing fee at $300,000 to $800,000, paid in project tokens and allocated toward marketing. That is before factoring in liquidity reserves ($50,000 to $150,000), security deposits (from $100,000 upward), audit costs, and any additional promotional spending. The total launch budget for a Binance listing in 2025 could realistically run into the millions.

For comparison, Coinbase states publicly that listing with them is, and has always been, free.

The question this raises is not complicated. If you are charging projects up to $800,000 in tokens to list on your platform, you are receiving tokens that you will, at some point, need to sell or distribute. If the tokens you receive are then listed on your own platform and prices decline sharply, the math of who absorbed that decline is not hard to follow.

Binance’s position is that the tokens go back to users. However, critics argue the effects show up in that first-week sell pattern, which Empirica specifically flagged: “In the first week, prices of newly listed tokens fall by 6.34%. This is likely due to profit-taking by listing speculators, insiders, or the exchange itself selling tokens received as listing fees.”

The listing fee controversy became central to understanding the Binance Effect reversal, because it revealed the economic incentives driving the post-listing dumps.

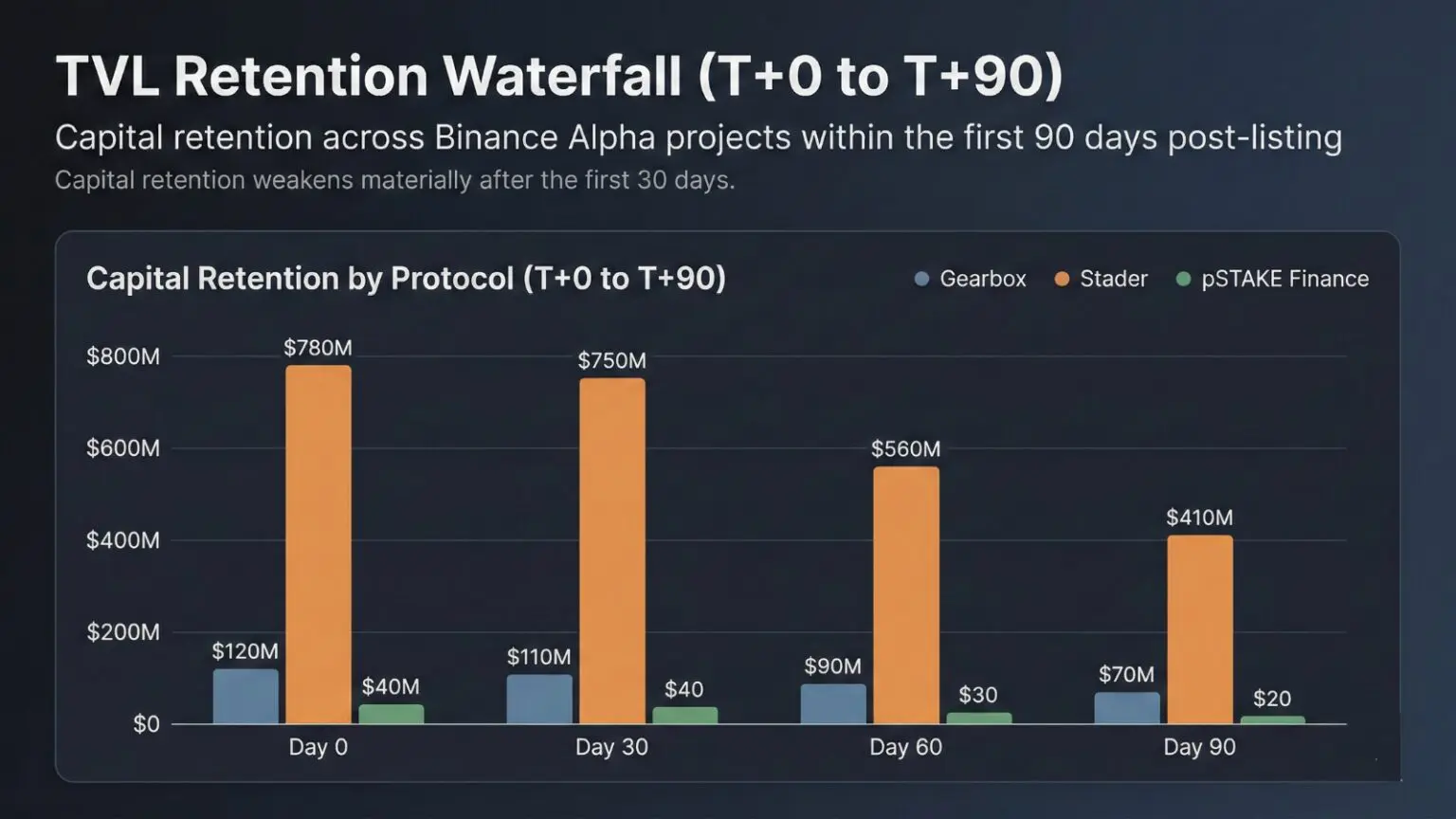

Binance’s response to the broader memecoin cycle of 2024-2025 was to launch Alpha, a fast-track listing mechanism designed to surface community-driven tokens and give projects a pipeline into the main exchange. The pitch was reasonable enough. Faster listings, broader access, a way to capture the Solana-driven memecoin energy without missing it entirely.

The outcomes were not good.

According to historical data from DeFiLlama, over 70% of the TVL of projects launched via Binance Alpha was halved within three months of listing. The Binance Effect reversal was even more pronounced in the Alpha category than in standard listings.

In November 2024, the Alpha dynamic came into sharp focus when Binance unexpectedly listed two low-cap Solana memecoins: ACT (The AI Prophecy) and PNUT (Peanut the Squirrel). Both had seen minimal trading activity before the announcement.

Following the listings, ACT surged over 1,000% to a market cap above $400 million. Meanwhile, PNUT rose roughly 100%. What followed was a public petition from Leonidas, co-founder of Bitcoin Ordinals explorer Ord.io.

He argued that Binance was deliberately targeting dormant, low-cap memecoins, specifically because projects with concentrated supply, where a small number of insiders hold most of the tokens, could afford to pay the largest percentage of supply as a listing fee. The exchange, he alleged, would then sell those tokens into the spike it had just created.

We can only assume that Binance is specifically targeting low-cap ‘dead’ memecoins that are controlled by a small number of insiders because these are the ones that are able to pay the largest percentage of the supply as the listing fee, which Binance then dumps to generate revenue,” Leonidas wrote.

Binance denied it. However, the petition went viral because the timeline fit the thesis. The pattern of obscure memecoin, sudden listing announcement, massive spike, then gradual or rapid decline had repeated itself enough times that people had started tracking it in real time. This became another data point supporting the Binance Effect reversal narrative.

On October 10, 2025, crypto had its worst single day in recorded history. This event accelerated the recognition of the Binance Effect reversal across the entire community.

$19 billion in leveraged positions were wiped out. That is the largest single-day liquidation event across the entire 16-year history of the asset class. Traders across every major exchange were hit simultaneously with sudden price swings, technical disruptions, liquidity gaps, and cascading forced sells that fed on each other.

Binance experienced system glitches and pricing discrepancies during the chaos. The platform ultimately confirmed it would pay out approximately $600 million in compensation to affected users and businesses.

The community did not accept the official narrative quietly. OKX founder Star Xu went on record publicly blaming Binance for the event. Crypto Twitter assigned blame in real time. The specific accusations varied: that Binance had dumped $1 billion in Bitcoin to trigger the initial drop, that CZ’s earlier comment expressing he was less confident in the crypto supercycle had been a deliberate sentiment signal, that Binance’s announced plan to convert its $1 billion SAFU fund from stablecoins into Bitcoin had been timed or executed in a way that added sell pressure.

CZ responded across multiple platforms, including an AMA on Binance’s own social platform and posts on X. He framed the crash as a macro event driven by major tariff announcements, which rattled global financial markets and triggered a repricing across equities and risk assets simultaneously. He denied any internal manipulation. Also, pointed to Binance’s regulatory oversight under Abu Dhabi’s ADGM framework and the presence of US compliance monitors. Also, he emphasized that Binance does not trade crypto directionally to profit from price movements.

On the accusations about his supercycle comment, he was direct: “That’s all I said. If I had that power, I wouldn’t be on Crypto Twitter with you lot.”

However, the $600 million payout told a story of its own. You do not pay $600 million in compensation for a crash that had nothing to do with you. The compensation confirmed that Binance’s technical failures during the event were real and material, even if the broader crash was caused by macro factors. Critics argued that the two things were not entirely separable. When the world’s largest exchange suffers system failures during extreme volatility, its infrastructure becomes part of the causation chain, not just a bystander.

The trust gap between Binance and parts of its own community had been widening for a year before October 10. That event accelerated it, and it cemented the Binance Effect reversal in the minds of many traders.

What makes the current situation structurally different from past bear periods for Binance listings is not just the data. Rather, it is that the data is now public, widely discussed, and being acted on. The Binance Effect reversal has become common knowledge.

The Empirica research team noted it plainly: “The data is public, and investors have drawn their conclusions. A contrarian strategy of selling something that most people expect to rise but which data shows regularly falls makes sense here. Investors have likely decoded and now anticipate insider behavior.”

The mechanics have flipped. People who once bought on listing announcements now look at the same announcement as a signal to short or at minimum to stay away. The front-running that used to be bullish is now bearish. This represents the complete Binance Effect reversal in trader psychology.

And yet Binance’s structural dominance remains. In Q1 2025, the exchange controlled roughly 36.5% of global CEX trading volume. By April 2025, CoinGecko placed their share at 38%. Meanwhile, Coinbase, their closest US competitor, had dwindled to under 7% of CEX spot volume. The network effects of liquidity are not broken. When Binance has the volume, price discovery still happens there, and that keeps projects paying the listing fees regardless of outcome data.

This is what makes the dynamic self-sustaining in the short term and corrosive in the long term. Projects continue paying to list because there is nowhere else with that liquidity. VCs continue using listings as exits because retail still shows up. Retail continues showing up, less than before and more cautiously, but still showing up, because the badge still carries residual weight from a period when it genuinely meant something.

The only category that has consistently bucked the trend? Meme coins with no significant VC backing and no listing fee arrangements. JUP, NEIRO, WIF, TURBO: the tokens that outperformed in 2024 were almost all in this category. No insiders with locked allocations, no VCs needing exits, no $4 billion FDV at listing.

The community figured that out too. The fair-launch narrative and the hostility toward high-FDV VC tokens did not come from nowhere. Rather, it was a rational response to watching the data play out in real time, listing after listing, cycle after cycle. Understanding the Binance Effect reversal meant understanding that fair-launch memecoins were the only segment immune to the exit-liquidity dynamic.

Binance is not going anywhere. The exchange is bigger, more regulated, and more deeply embedded in market infrastructure than it has ever been. However, the Binance Effect, in the original sense of the term, is gone.

The effect was never really about Binance. Instead, it was about what retail believed Binance represented: quality, validation, access to something worth buying. A stamp of approval that meant the project had passed a serious bar.

That belief has been eroded by three years of data showing that the listing process, regardless of the quality bar being described, produces tokens that systematically underperform. It has been eroded by the revelation that listing fees run into the hundreds of thousands or millions. It has been eroded by the ACT and PNUT controversy, the Alpha TVL collapse, and the October crash aftermath.

For VCs, a Binance listing is still a payday. For retail buying in on listing day, the math is brutal. 37% of those tokens hit their all-time high on day one and never recover it. The exit was already in progress before you saw the announcement.

The Binance Effect reversal is complete. The signal that once meant buy now means sell. Traders who haven’t updated their playbook are funding the exits of those who have. In crypto, the most expensive mistake is believing in a pattern after the data has already killed it.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.