Loading Search...

Token buybacks often fail without real demand, as weak utility and artificial price support limit long-term growth and sustainability.

Author: Arushi Garg

Every few weeks, a crypto protocol announces a token buyback and the community reacts immediately. Prices spike, Crypto Twitter celebrates, and threads quickly appear claiming that the announcement changes everything. But two weeks later, the token is often back where it started or even lower. The buyback ends up having little to no real impact on the price. This does not happen because token buybacks are useless. It happens because the underlying demand was already weak, and very few people actually looked at the numbers before getting excited.

Token buybacks are one of the most misunderstood mechanisms in crypto. The idea comes from traditional finance, where share buybacks often signal confidence and return value to shareholders. However, crypto tokens are not equities. They exist inside ecosystems with continuous emissions, vesting unlock schedules, inflationary reward structures, and relatively thin liquidity.

Because of these dynamics, a buyback that sounds impressive in a press release can end up being economically invisible or, in some cases, a distraction from weakening fundamentals. The right way to evaluate a crypto buyback is not emotional. It requires a simple supply-and-demand calculation. At the end of the analysis, one question matters most: is net circulating supply shrinking while real demand is growing?

The psychological appeal of a buyback is easy to understand. A protocol is spending money to purchase its own token from the open market. That creates the impression of organic demand. It signals confidence and introduces a buyer where there might otherwise be none. However, the context behind that purchase matters far more than the announcement itself.

Consider a protocol with 8 percent annual staking emissions, a twelve-month token unlock schedule for early investors, and daily trading volume of around $2 million. If the buyback amounts to $50,000 per week, that equals roughly $7,100 per day. This means the buyback absorbs only about 0.35 percent of daily trading volume. At the same time, validators, stakers, and liquidity miners may be distributing thousands of tokens into the market every day. Early investors who bought tokens at a fraction of the current price may also be reaching the end of their lock-up periods and placing sell orders they planned many months earlier.

In that context, the buyback becomes extremely small compared to the overall supply entering the market. In practical terms, the buyback becomes a drop of ink in a river.

The announcement effect around token buybacks is real, but it is usually temporary. It acts as a sentiment catalyst rather than a structural change. Prices move because traders expect others to react to the news and buy the token. Once that reactive demand fades, the underlying supply dynamics return to controlling the market. Those dynamics are based on actual token flows, and they do not respond to press releases.

The first number to calculate when evaluating a token buyback is daily sell pressure. This is not the same as daily trading volume. Trading volume includes both buyers and sellers, while sell pressure specifically measures the amount of tokens likely to enter the market through structural mechanisms.

A rough estimate of daily sell pressure can be built by combining the main sources of consistent selling. Staking and validator rewards are one of the most common sources. Every day, new tokens are emitted to validators and stakers. Some of these tokens are restaked, but many are sold to realize profits or cover operating costs.

Treasury grants and contributor payments also create structural sell pressure. Protocols that compensate developers, researchers, or ecosystem contributors in native tokens indirectly introduce those tokens into the market because those contributors often convert part of their compensation into fiat or stablecoins.

Liquidity mining programs add another layer of supply. When liquidity providers receive native tokens as rewards, a significant portion of those rewards is often sold shortly after becoming claimable on decentralized exchanges. Vesting unlocks also increase the potential for selling. Whenever a new tranche of tokens unlocks for early investors or team members, the amount of supply that can enter the market rises significantly.

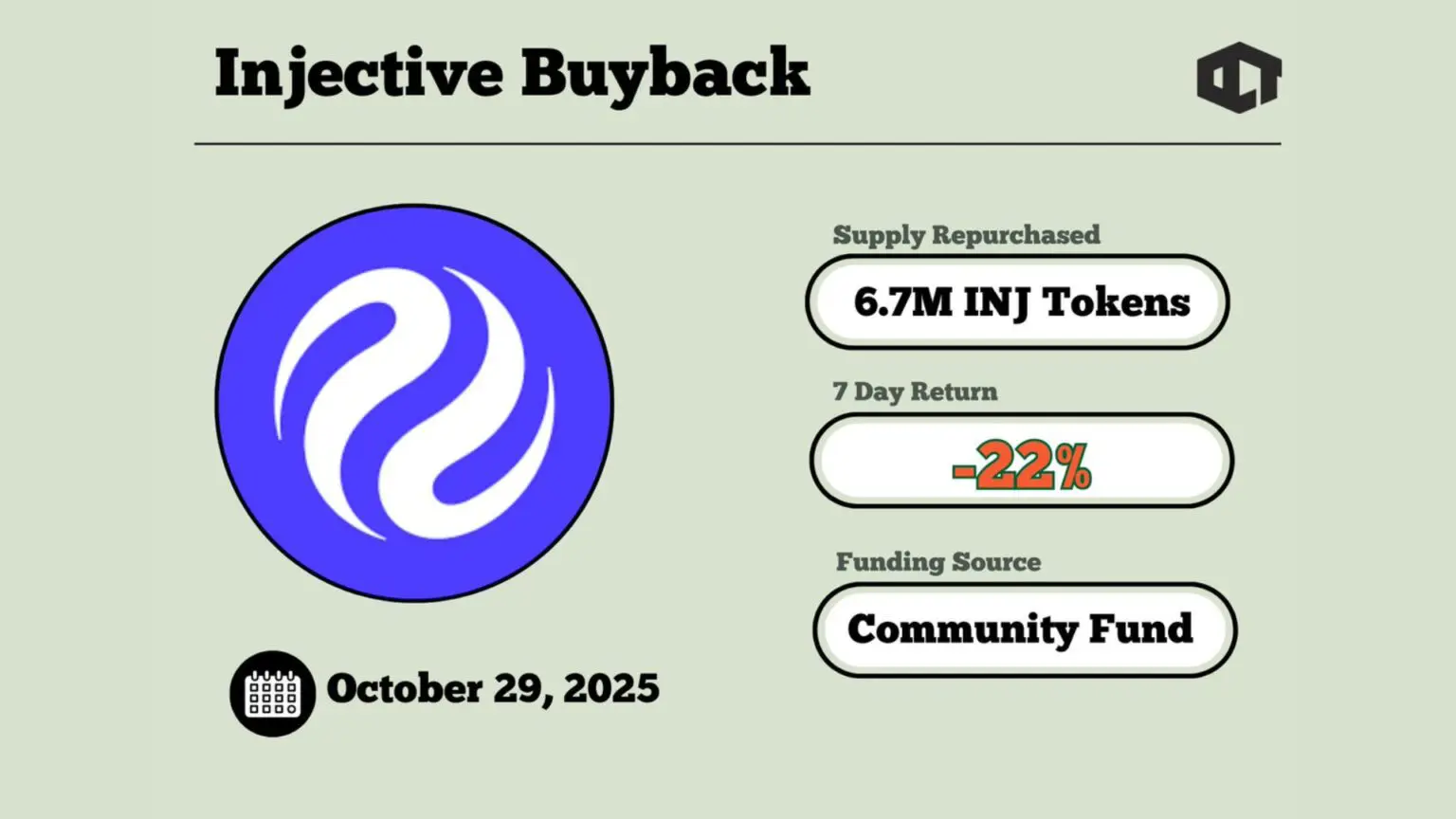

Once a rough estimate of daily sell pressure is calculated, it should be compared with the daily buyback rate. Most buyback programs are announced in aggregate terms, such as “$5 million over the next quarter.” When broken down, this typically equals around $55,000 per day. In some cases, the program is even smaller. The Injective (INJ) buyback, for example, was not even $100,000 in total. The outcome of that program illustrates why the size of the buyback relative to daily sell pressure matters far more than the headline announcement.

If your estimated daily sell pressure is around $300,000, a buyback of roughly $55,000 per day is covering less than 20 percent of the structural outflow. The remaining supply still has to be absorbed by the market.

If demand is stagnant, new users are not entering the ecosystem, total value locked (TVL) is flat, and protocol revenue is declining, that excess supply usually appears as gradual price depreciation. In these cases, a buyback does not solve the problem. It simply slows it down. The buyback buys time, not survival.

Nothing cancels out a token buyback faster than a major unlock event. Yet unlock schedules are often underestimated in community analysis because they feel abstract until they actually happen.

During a Token Generation Event (TGE), tokens are typically distributed to founders, early investors, ecosystem funds, and advisors. These allocations usually come with lockup periods that range from six months to three years. Even though these tokens exist on-chain, they are not part of the circulating supply until their lockup expires.

When the lockup period ends, it does not necessarily mean every token is sold immediately. However, the capacity to sell increases dramatically overnight, which can significantly change the supply dynamics in the market. For any protocol running a buyback program, it is important to compare the unlock calendar with the buyback timeline. The first question to ask is how much supply is unlocking soon.

Look at what percentage of total supply unlocks in the next 30, 60, and 90 days. If 8 percent of the total supply unlocks next month while the buyback removes only 0.5 percent of supply over the same period, the buyback becomes mathematically irrelevant to overall supply dynamics. In practical terms, this situation is similar to fighting a forest fire with a garden hose.

The second question is who is unlocking tokens. Seed round investors who bought tokens at very low prices and are sitting on large gains often behave differently from ecosystem treasury allocations that are later distributed as grants. Early investors represent direct sell pressure, while treasury distributions usually become delayed sell pressure as grants turn into contributor salaries that eventually reach the market.

The third question concerns timing. Some protocols announce buyback programs at the exact moment their token unlock curve is about to accelerate. Whether intentional or not, this timing can act as a sentiment buffer for what would otherwise be a large supply shock. Recognizing this pattern helps distinguish genuine token buyback strategies from tactical price management ahead of dilutive events.

Nothing cancels out a token buyback faster than a major unlock event. Yet unlock schedules are often underestimated in community analysis because they feel abstract until they actually happen.

During a Token Generation Event (TGE), tokens are typically distributed to founders, early investors, ecosystem funds, and advisors. These allocations usually come with lockup periods that range from six months to three years. Even though these tokens exist on-chain, they are not part of the circulating supply until their lockup expires.

When the lockup period ends, it does not necessarily mean every token is sold immediately. However, the capacity to sell increases dramatically overnight, which can significantly change the supply dynamics in the market. For any protocol running a buyback program, it is important to compare the unlock calendar with the buyback timeline. The first question to ask is how much supply is unlocking soon.

Look at what percentage of total supply unlocks in the next 30, 60, and 90 days. If 8 percent of the total supply unlocks next month while the buyback removes only 0.5 percent of supply over the same period, the buyback becomes mathematically irrelevant to overall supply dynamics. In practical terms, this situation is similar to fighting a forest fire with a garden hose.

The second question is who is unlocking tokens. Seed round investors who bought tokens at very low prices and are sitting on large gains often behave differently from ecosystem treasury allocations that are later distributed as grants. Early investors represent direct sell pressure, while treasury distributions usually become delayed sell pressure as grants turn into contributor salaries that eventually reach the market.

The third question concerns timing. Some protocols announce buyback programs at the exact moment their token unlock curve is about to accelerate. Whether intentional or not, this timing can act as a sentiment buffer for what would otherwise be a large supply shock. Recognizing this pattern helps distinguish genuine token buyback strategies from tactical price management ahead of dilutive events.

Throughout 2025 and early 2026, several crypto protocols experimented with different token buyback mechanisms. Some programs successfully removed supply from the market and strengthened price structure. Others spent millions of dollars with almost no measurable impact on price. Across the industry, total capital deployed into token buyback programs exceeded $1.4 billion. However, the results varied widely depending on how each program was designed and executed.

Here is what actually happened.

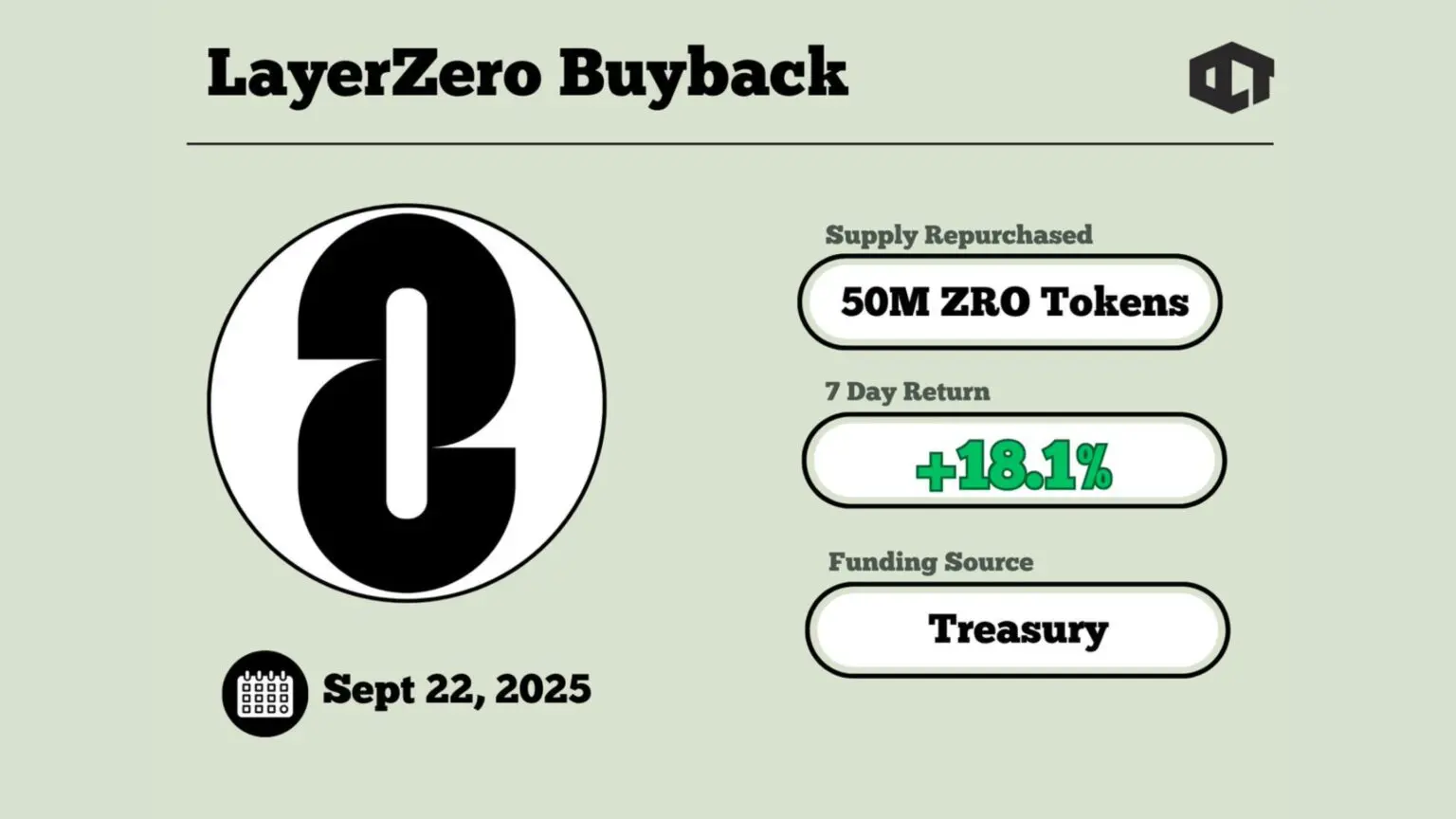

LayerZero executed a direct negotiated repurchase from early investors instead of buying tokens through open market orders. This approach allowed the protocol to remove a known block of potential sell pressure in a single transaction.

This program worked because it eliminated real and identifiable sellers from the market. Rather than trying to counter ongoing sell pressure with daily buy orders, LayerZero removed the supply overhang directly. The impact was immediate because a large source of potential selling was taken out of circulation at once. However, a one-time repurchase does not solve long-term token supply dynamics. Future emissions and upcoming unlock schedules can still introduce new supply into the market. Because of this, long-term price sustainability still depends on continued protocol adoption and demand growth.

Classification: Real Impact (One-Time)

Injective carried out a community-driven burn event, permanently destroying tokens instead of holding them in the treasury.

From a structural perspective, the burn was executed correctly. Tokens were permanently removed from circulation, which reduced the net circulating supply. However, the event happened during a broader market downturn. The negative macro environment outweighed the deflationary signal created by the burn. This case highlights an important lesson. Even a well-structured token burn or buyback cannot fully protect a token from wider market conditions. While the long-term supply compression improved Injective’s tokenomics, the short-term price reaction remained negative because overall market sentiment was weak.

Classification: Real Impact (Macro Override)

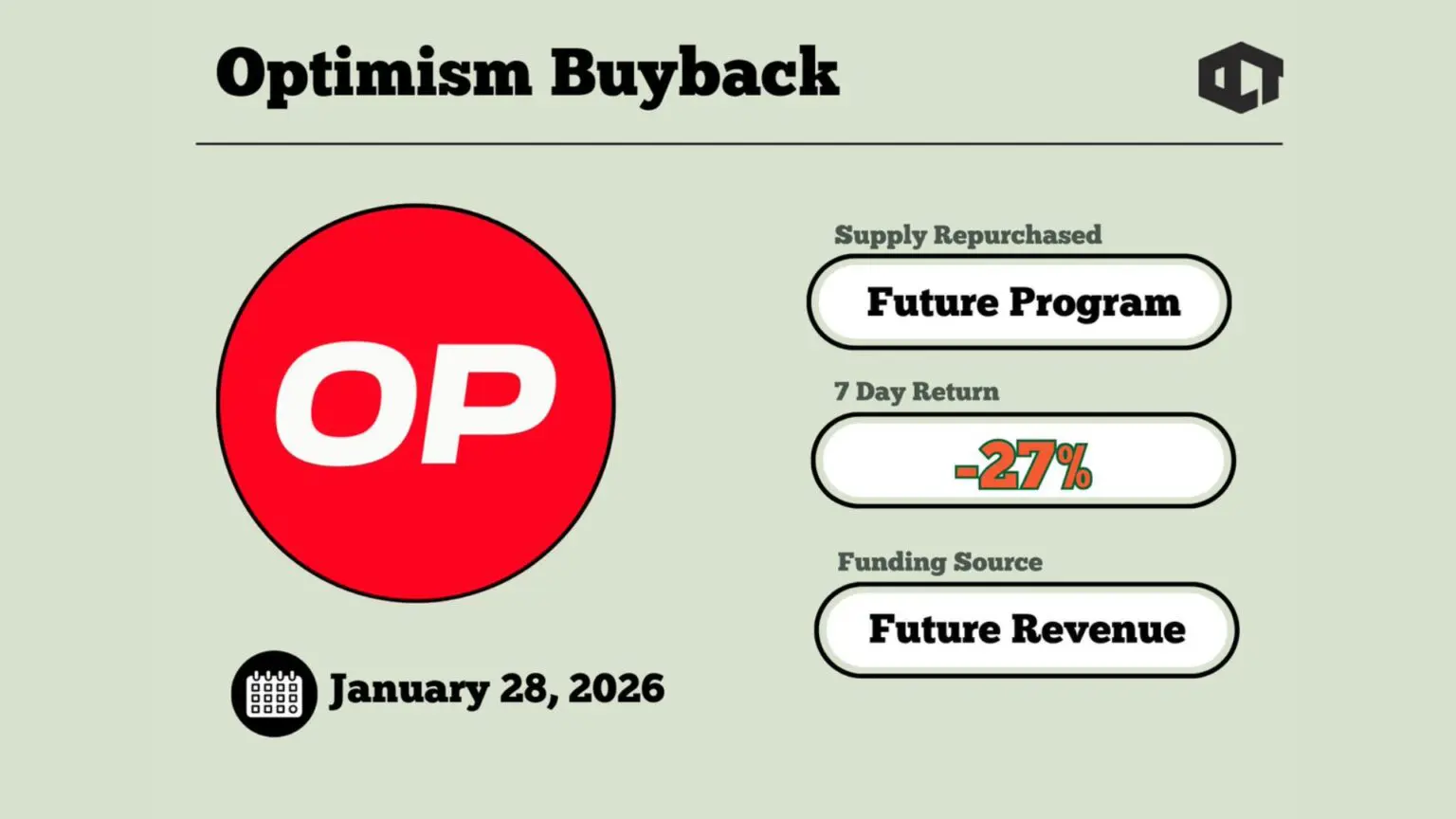

Optimism governance voted to allocate 50 percent of Superchain revenue toward future OP buybacks. However, the vote itself did not trigger any immediate reduction in circulating supply.

The market reacted to the announcement at first, but nothing actually changed in the token supply equation on day one. No tokens were purchased and no tokens were burned. At the same time, ecosystem grant emissions continued to distribute new supply into the market.

In simple terms, the event was driven by sentiment rather than a structural change in supply. Buybacks funded by future revenue can eventually become meaningful, but only once that revenue accumulates and tokens are actively removed from circulation.

Classification: Marketing-Driven Announcement

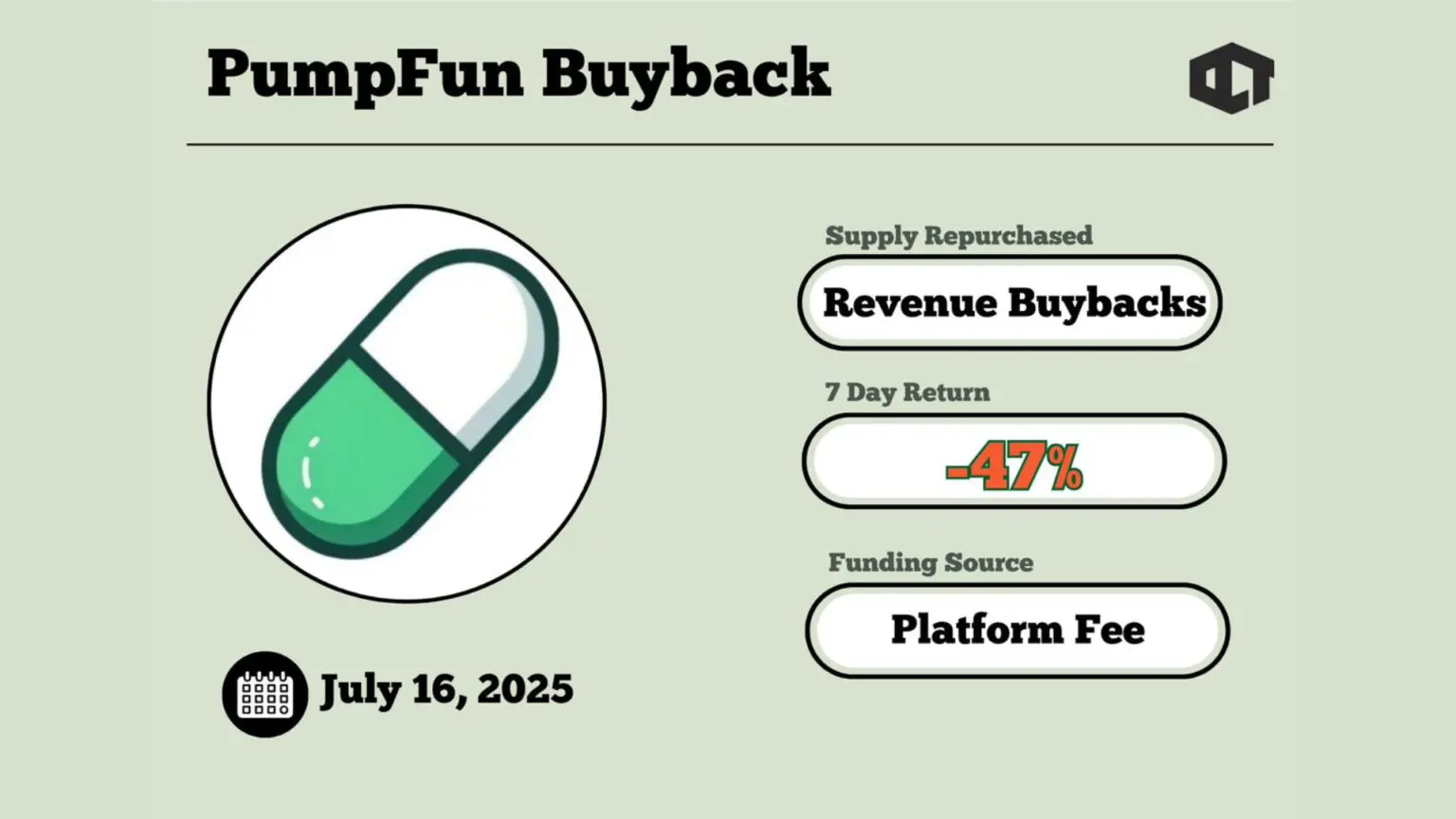

Pump.fun launched with a continuous, revenue-funded buyback model that used platform fees to repurchase tokens from the market.

The design of the program was structurally sound. Revenue-funded buybacks align token demand with real protocol activity because buy pressure increases as platform usage grows. However, the program launched during the heaviest distribution phase of the token’s lifecycle. Early participants, airdrop recipients, and insiders were all selling into the market at the same time.

The buyback volume generated from platform fees was simply too small to absorb that level of supply. As a result, the mechanism had little immediate effect on price. Over time, as platform revenue increased, the buyback program became more meaningful. But at launch, it was overwhelmed by the amount of sell pressure entering the market.

Classification: Neutral Impact (Timing Problem)

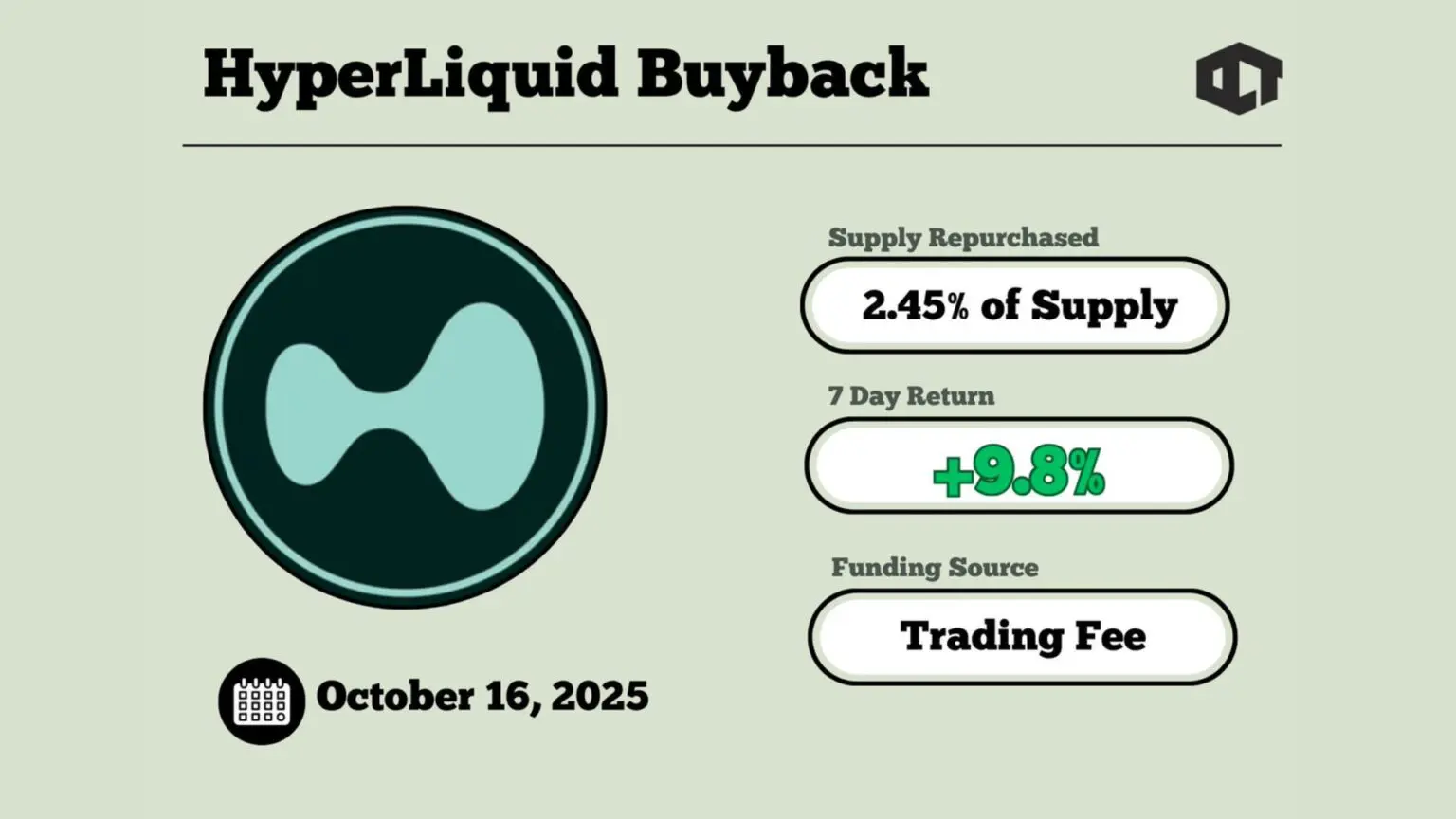

Hyperliquid implemented a continuous buyback program through its Assistance Fund, using trading fees generated directly from platform activity.

This program represents one of the most structurally effective buyback models currently operating in the crypto market. The key reason is that buy pressure scales automatically with platform usage. As trading activity increases, the fees generated by the platform also rise, which strengthens the buyback mechanism. Unlike many other buyback programs, this model does not rely on treasury allocations or governance votes. Instead, it runs continuously in the background and gradually absorbs supply from the market.

The price appreciation seen in October was not driven by speculation about a future buyback announcement. It reflected demand that had already accumulated through consistent fee generation and token repurchases.

Classification: Real Impact (Gold Standard)

When the above framework is applied across multiple protocols, a clear classification system begins to appear. Token buyback programs generally fall into three categories depending on how they interact with supply and demand dynamics.

Real impact buybacks occur when the mechanism meaningfully reduces circulating supply relative to the amount of tokens entering the market.

These programs usually share several characteristics:

These cases are relatively rare. When they appear, they represent genuine improvements in token supply and demand dynamics. Interestingly, the market often underestimates them at first because the announcement itself may not look dramatic. However, the long-term compounding effect can be meaningful.

Neutral buybacks occur when the buyback roughly offsets ongoing emissions but does not meaningfully reduce total circulating supply.

Typical characteristics include:

These programs are not necessarily harmful, but they also do not transform the token’s market structure. At best, they provide moderate price support in low-volume environments and signal that the protocol is paying attention to tokenomics management.

Marketing-driven buybacks are the most common category in the crypto market. These announcements often create short-term excitement but do little to improve the underlying supply equation.

They usually appear under the following conditions:

In many cases, these buybacks are designed to create a news cycle rather than solve structural tokenomics issues. Retail participants who react to the headline without analyzing supply dynamics often end up buying into distribution events.

At the end of the day, evaluating any token buyback can be reduced to a single core question:

Is net circulating supply shrinking while real demand is growing?

Supply shrinkage happens only when token burns and buyback burns exceed emissions and unlocks over a meaningful time horizon. This must occur consistently over months, not just as a one-time event. Demand growth must also come from real usage rather than short-term speculation. Evidence of genuine demand includes rising unique users, growing protocol revenue, increasing total value locked, higher transaction counts, or expanding real-world use cases that are not artificially created through incentives.

When both of these forces occur at the same time, the token has a strong asymmetric setup. The fundamentals and the token mechanics move in the same direction, allowing demand to absorb supply instead of simply supporting it. If only one of these conditions is present, the setup becomes incomplete.

A shrinking supply without growing demand can create a slow deflationary squeeze, but it may not translate into price appreciation if the market has little interest in the protocol. On the other hand, strong demand combined with uncontrolled emissions leads to dilution, where value created by the protocol does not fully reach token holders.

When neither condition is true, and supply continues expanding while demand stagnates or declines, a buyback announcement becomes meaningless. At that point, it is simply a headline rather than a functioning mechanism. Before reacting to the next buyback announcement, it is worth taking a few minutes to check the fundamentals.

Look at the token’s unlock schedule, analyze 30-day emission data, estimate daily sell pressure, verify whether the protocol burns or holds tokens, and compare the 90-day revenue run rate with the announced buyback commitment. If the math does not support the narrative, the announcement will not support the price either.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.