Loading Search...

The AI bubble 2026 reached its peak when belief outpaced reality. Discover how $80M vanished, tokens collapsed, and why talent is leaving.

Author: Tanishq Bodh

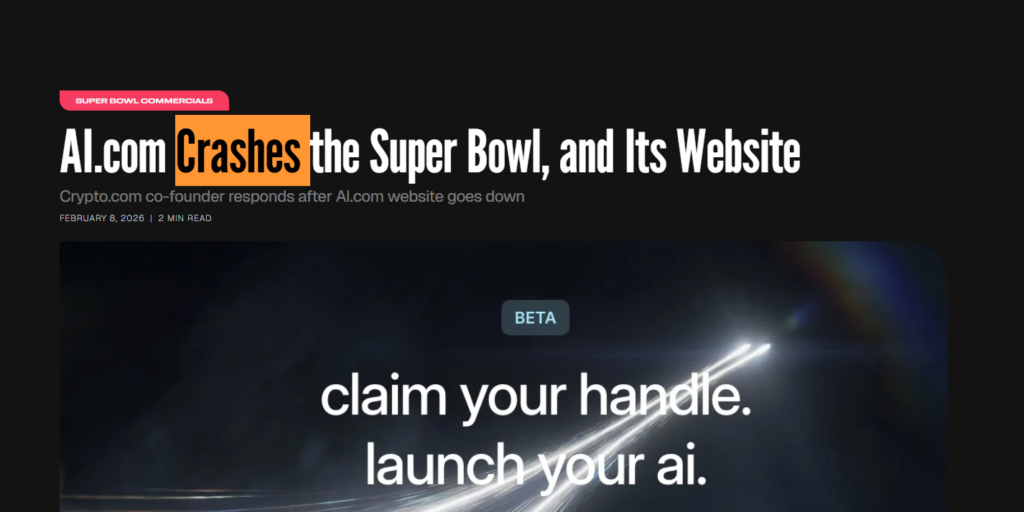

On Super Bowl Sunday 2026, ten million dollars evaporated in real time. Crypto.com spent $70 million acquiring ai.com and ran a Super Bowl ad promising to accelerate AGI. Instead, users got a 504 Gateway Time-out error. The site crashed before anyone could test anything, and the UI looked like a weekend hackathon project. If you’ve been wondering whether the AI bubble 2026 has reached its peak, stop wondering. The emperor just spent $80 million on clothes that don’t exist and tripped on the runway in front of 115 million people.

This wasn’t a technical glitch. It was a signal. When a company with zero AI credentials can spend this much on marketing vaporware, and when the infrastructure fails under predictable traffic, you’re witnessing the absolute top. The AI bubble 2026 didn’t pop because the technology failed. It popped because belief outpaced reality by orders of magnitude.

Every bubble has a birth moment. For AI, it was November 30, 2022, when OpenAI released ChatGPT to the public. The numbers were unprecedented. One million users in five days. One hundred million monthly users by January 2023. ChatGPT became the fastest-growing consumer app in history, faster than Instagram, Spotify, or TikTok. Unlike those platforms, ChatGPT wasn’t entertainment or social validation. It looked like intelligence. That was enough.

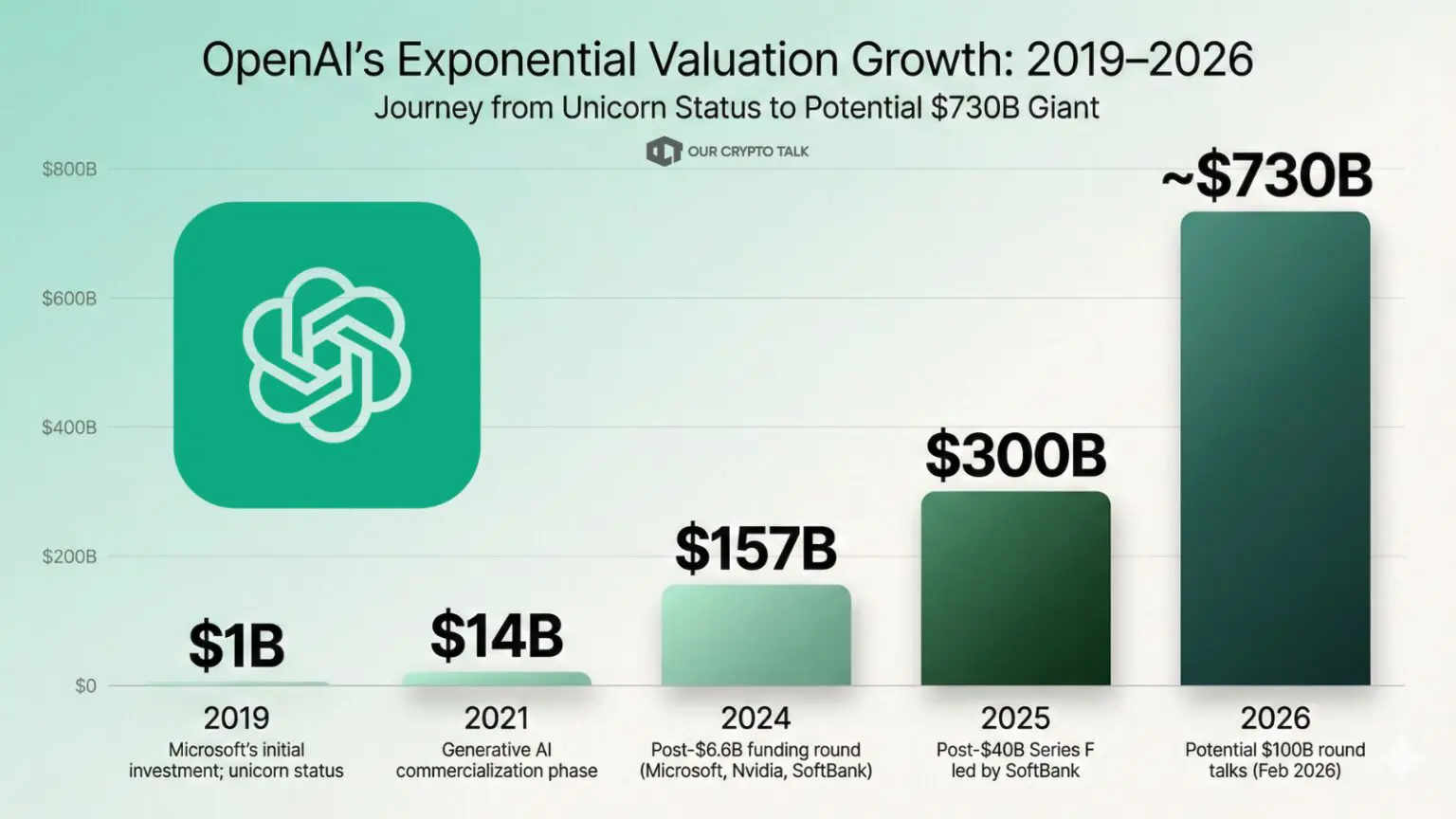

Investors lost their minds. Executives panicked. Microsoft poured $10 billion into OpenAI in early 2023. OpenAI’s valuation jumped to $29 billion, then quietly to $86 billion by late 2023. Revenue was roughly $1.6 billion annualized. That’s 50x sales for a company still burning cash and capped by compute constraints. For context, Google trades around 6–7x sales. Nobody cared. Capital was stampeding.

According to PitchBook, AI startups raised over $50 billion in 2023 alone. Every major tech company scrambled. Google panic-launched Bard, which hallucinated in the demo. Alphabet lost $100 billion in market cap in one day. Meta open-sourced LLaMA. Salesforce launched Einstein GPT. Anthropic raised $450 million at a $4.1 billion valuation. Character.ai raised $150 million at $1 billion with no clear monetization path. The rule was simple: attach AI to anything and watch money fall from the sky.

Then entrepreneurs realized something important. You didn’t need to build AI. Building real models costs hundreds of millions, massive datasets, and teams of PhDs. You just needed to wrap someone else’s API. The wrapper economy was born, and the margins were absurd.

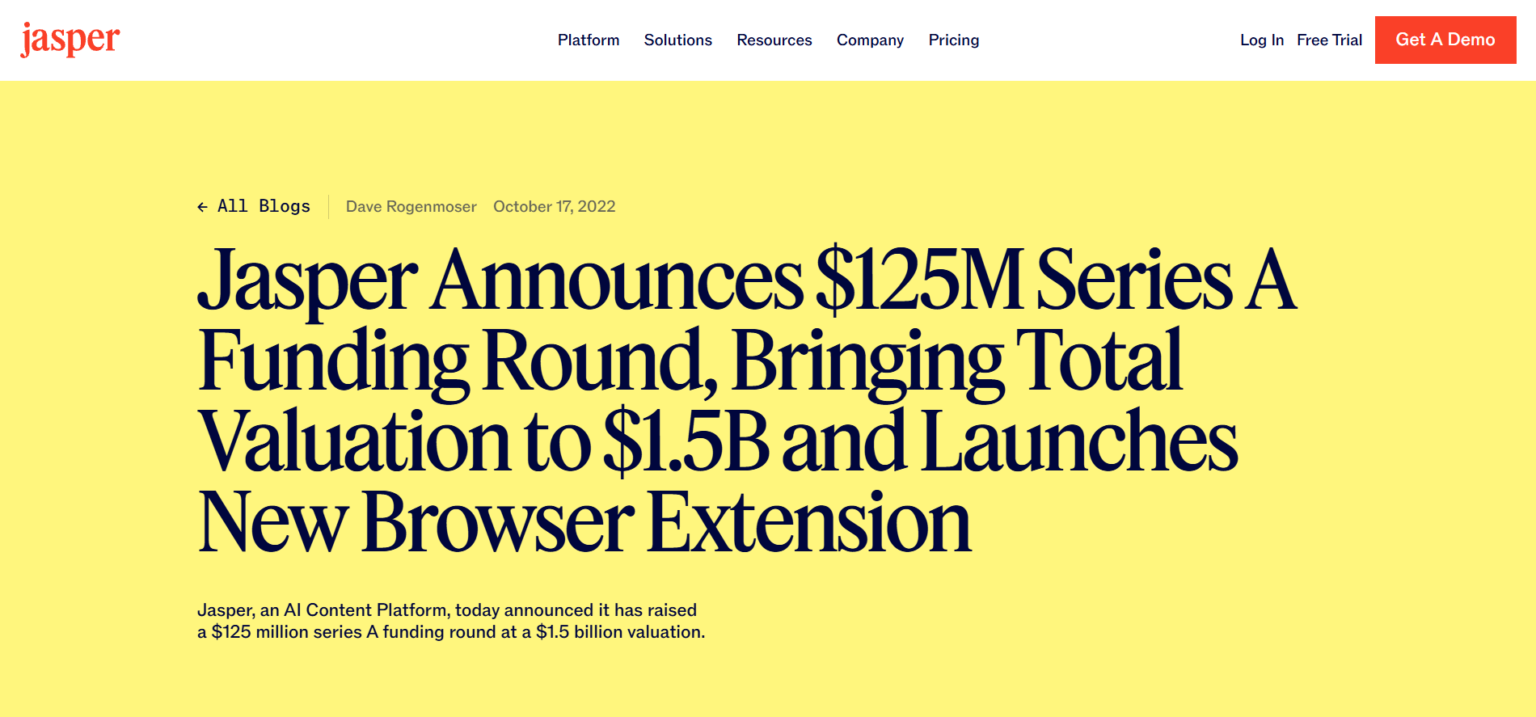

Take Jasper AI. By October 2022, it had raised $125 million and was valued at $1.5 billion. Its core technology was OpenAI’s API plus prompt templates. OpenAI charged around $0.002 per 1,000 tokens. Wrapper companies charged $49, $99, or $199 per month for what amounted to $2–5 in actual API usage. Gross margins north of 90 percent. Copy.ai, Writesonic, Rytr, Article Forge, and ContentBot followed. All the same product. Different landing pages.

Then OpenAI launched ChatGPT Plus at $20 per month. Overnight, the entire wrapper category was commoditized. The moat vanished. Differentiation collapsed. But venture funding didn’t stop. By 2024, AI companies raised over $100 billion in two years. Most of them didn’t own the models, the data, or the infrastructure. They owned branding.

Crypto was bleeding. The year 2022 destroyed $1.4 trillion in market cap with Luna, FTX, 3AC, collapsing DeFi yields, dead NFTs, and a forgotten metaverse. The industry needed a lifeline. AI became it. Early 2024 saw any token mentioning AI pump 200–500 percent with zero product changes. Insiders distributed. AI-related crypto market cap went from $2–3 billion to $25–30 billion on pure narrative momentum.

Fetch.ai, SingularityNET, and Ocean Protocol got new coats of paint. FET went from $150 million to $6 billion market cap. Then came pure vapor. ai16z, a memecoin with zero relation to a16z, hit $2 billion fully diluted valuation with no product and massive marketing. Terminal token hit $400–500 million for a ChatGPT interface that could execute Solana transactions. Users quickly realized they could just use ChatGPT and click approve themselves. The token collapsed 90 percent.

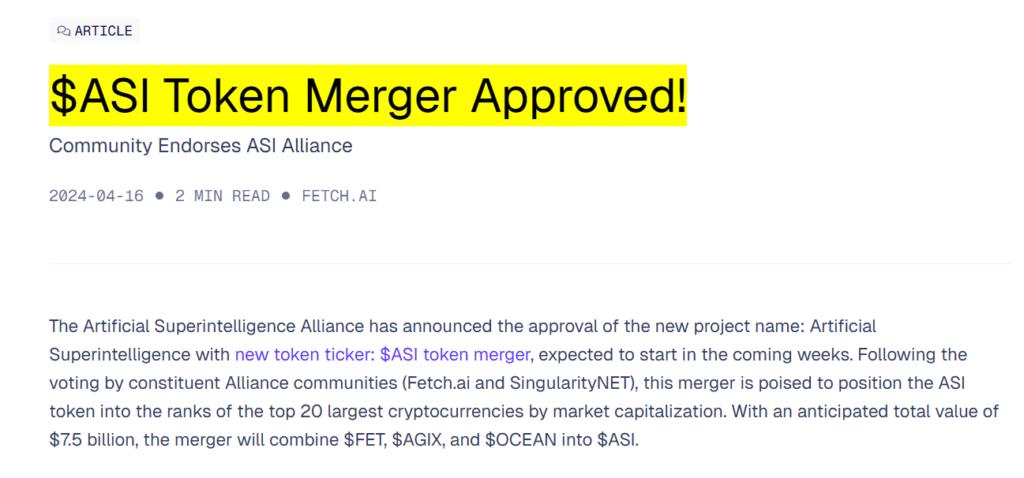

In March 2024, Fetch.ai, SingularityNET, and Ocean announced a merger. The new token, $ASI, was valued at $7.5 billion fully diluted valuation. The pitch was decentralized superintelligence, on-chain AI agents, and a people’s alternative to OpenAI. The reality was a vague roadmap, no competitive models, and a governance nightmare that was slower and worse than centralized APIs. By 2025, the merger had stalled, tokens never converted, and FET was down roughly 70 percent. AGIX and OCEAN were down 80 percent or more. You can’t rebrand 2017 infrastructure into frontier AI. Narratives don’t change physics.

The crypto-AI marriage sounded poetic. Decentralized intelligence. Autonomous agents. Tokenized coordination. The future of computation. In practice, it failed for four unavoidable reasons.

First, speed kills blockchains. AI inference happens in milliseconds. Blockchains finalize transactions in seconds, minutes, or sometimes longer. Consensus is a tax. Finality is friction. You cannot run meaningful AI workloads on-chain without destroying performance. Every on-chain agent demo quietly moved the actual intelligence off-chain, then used the blockchain as a glorified database or payment rail. If the intelligence isn’t on-chain, why is the token necessary? No one answered that convincingly.

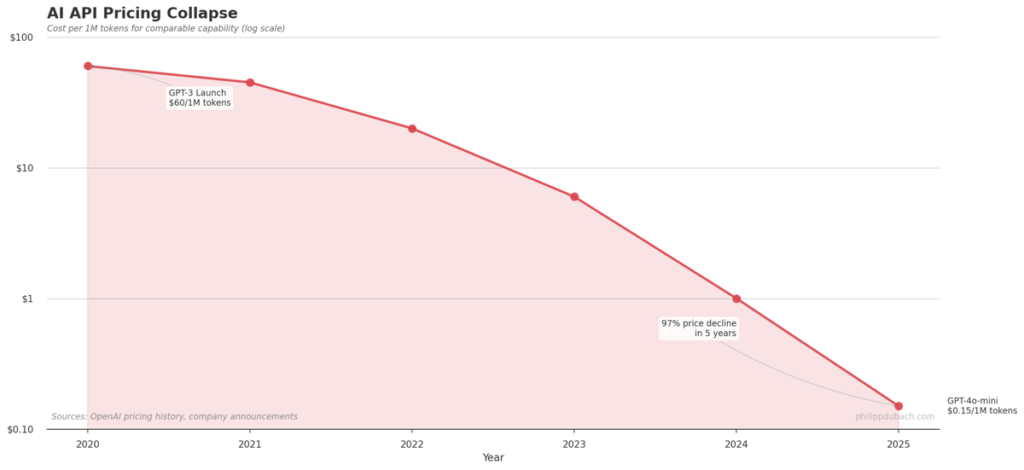

Second, the cost math never worked. AI API pricing collapsed violently. In just 12 months, GPT-4 class models went from roughly $0.03 to $0.002–0.005 per 1,000 tokens. That’s an 85–95 percent price collapse. Meanwhile, Ethereum gas fees fluctuated wildly, Solana had congestion and reliability issues, and crypto-AI apps charged both API costs and token costs. Why would anyone pay gas, slippage, volatility, and token inflation to access intelligence that’s cheaper, faster, and more reliable via a centralized API? They wouldn’t. And they didn’t.

Third, AI centralizes by nature. AI improves by aggregating data, consolidating compute, and training at massive scale. Decentralization fragments all three. AI progress rewards scale, coordination, and capital intensity. Blockchains optimize for trust minimization, redundancy, and censorship resistance. Those goals are orthogonal. Decentralization isn’t a feature for AI. It’s an obstacle.

Fourth, tokens solved nothing. Strip away the whitepapers and buzzwords and you’re left with one uncomfortable question: why does this need a token? The honest answer, most of the time, was liquidity, speculation, and incentive extraction. Alignment was just a polite word for number go up. The AI-crypto narrative didn’t create intelligence. It created tradable belief.

Then reality arrived. Hard. Fast. Unforgiving. Late 2024 and early 2025 brought the DeepSeek shock. DeepSeek released models competitive with GPT-4 and Claude with a reported training cost under $6 million. The industry had spent years telling investors that frontier AI required $100 million plus training runs, infinite GPU scaling, and permanent compute moats. That story died overnight. Nvidia lost $500–600 billion in market cap in a single day.

If frontier models could be trained for one-twentieth the cost, the entire valuation stack collapsed. For crypto-AI projects, it was extinction-level. If real labs couldn’t defend moats, speculative tokens never had one. By 2025, OpenAI, Anthropic, Google, and Meta were all offering near-frontier models. Some were cheap, some were freea and some were open-source and runnable on consumer hardware. AI stopped being scarce. Scarcity is the only thing wrappers sell.

Fortune 500 companies didn’t kill the bubble with tweets. They killed it with spreadsheets. Despite spending $40–50 billion on AI initiatives in 2024, only 10–15 percent reached production. Over 50 percent failed entirely. Most ROI projections collapsed. Patterns repeated: hallucinations in edge cases, heavy human oversight, brittle integrations, and marginal productivity gains. Even Microsoft Copilot struggled to justify $30 per user per month. If enterprises couldn’t extract value from actual AI products, what chance did speculative tokens have? None.

Then something quieter started happening. The people building the models began walking out. Within 48 hours in February 2026, Yuhuai Tony Wu, co-founder and head of reasoning at xAI, resigned. Jimmy Ba, another xAI co-founder overseeing research and safety, followed the next day. xAI has now lost half of its original 12 co-founders since launch.

At the same time, over at Anthropic, Mrinank Sharma, who led the safeguards research team, stepped down with a public warning about a world in peril. Additional R&D engineers and AI scientists exited in early February. No dramatic scandal. No public implosion. Just steady senior departures from companies supposedly racing toward AGI.

This isn’t mass layoffs. It’s something subtler and potentially more telling. When hype peaks and valuations soar, talent usually locks in. Equity vests. IPO rumors circulate. Momentum builds. Instead, we’re seeing safety leads leave, co-founders depart, and researchers hint at ethical fatigue and internal strain. In bubbles, capital exits first. In deeper structural shifts, talent exits. When the architects of the future start quietly heading for the door, you pay attention.

This is not an AI winter. The technology works. Transformers matter. LLMs are useful. Productivity gains are real, just incremental, not magical. The survivors will be infrastructure providers, foundational model labs, companies with proprietary data, and boring businesses using AI as a feature. They won’t have tokens. They’ll have revenue.

Ironically, the best time to build is after the bubble bursts. When hype capital leaves, expectations reset, talent gets cheaper, and customers care about ROI again, real builders don’t need AGI narratives. They ship tools that save time, cut costs, and quietly work.

The grift taxonomy by the end was easy to classify. The pivoters were crypto and NFT teams slapping AI on dead projects. The rebranders were legacy companies adding GPT APIs and calling it transformation. The wrappers sold prompts as products. The consultants charged four figures to explain ChatGPT. All of them extracted value from confusion, not capability.

Every cycle is the same. The technology is real. The narratives are exaggerated. The middle layer is vaporized. Crypto-AI failed because it tried to merge centralization-dependent intelligence with decentralization-obsessed infrastructure. They were never compatible. When narrative exceeds substance by two orders of magnitude, you’re at the top.

The AI bubble 2026 didn’t pop because AI failed. It popped because belief outpaced reality. The memes will be brutal. The recriminations loud. The write-downs historic. AI will survive. The tokens won’t. Crypto companies chasing AI was the tell. Terminal velocity reached. Welcome to the all-time high.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.