Loading Search...

Avici Review: A crypto-native neobank offering self-custodial wallets, stablecoin payments, and Visa cards to bring everyday banking onchain.

Author: Akshat Thakur

Global finance is still dominated by centralized banking systems that control custody, payments, and credit infrastructure. While cryptocurrencies introduced self-custody and permissionless value transfer, the ecosystem still lacks the everyday banking tools people rely on: credit cards, fiat accounts, and payment rails accepted by millions of merchants. In this Avici Review, we examine how global finance is still dominated by centralized banking systems that control custody, payments, and credit infrastructure.

Most crypto users still depend on traditional banks to convert fiat, make payments, or access credit. This dependency creates friction and contradicts the original vision of decentralized finance.

This Avici Review examines Avici, a crypto-native financial platform attempting to build an internet-native neobank. The project connects fiat infrastructure with self-custodial crypto wallets, enabling users to spend, receive, and manage funds without giving up ownership of their assets. Instead of forcing users to abandon traditional financial rails entirely, Avici integrates them with blockchain infrastructure. The platform provides crypto credit cards, fiat onramps, smart wallets, and payment tools designed to make stablecoins usable for everyday financial activity.

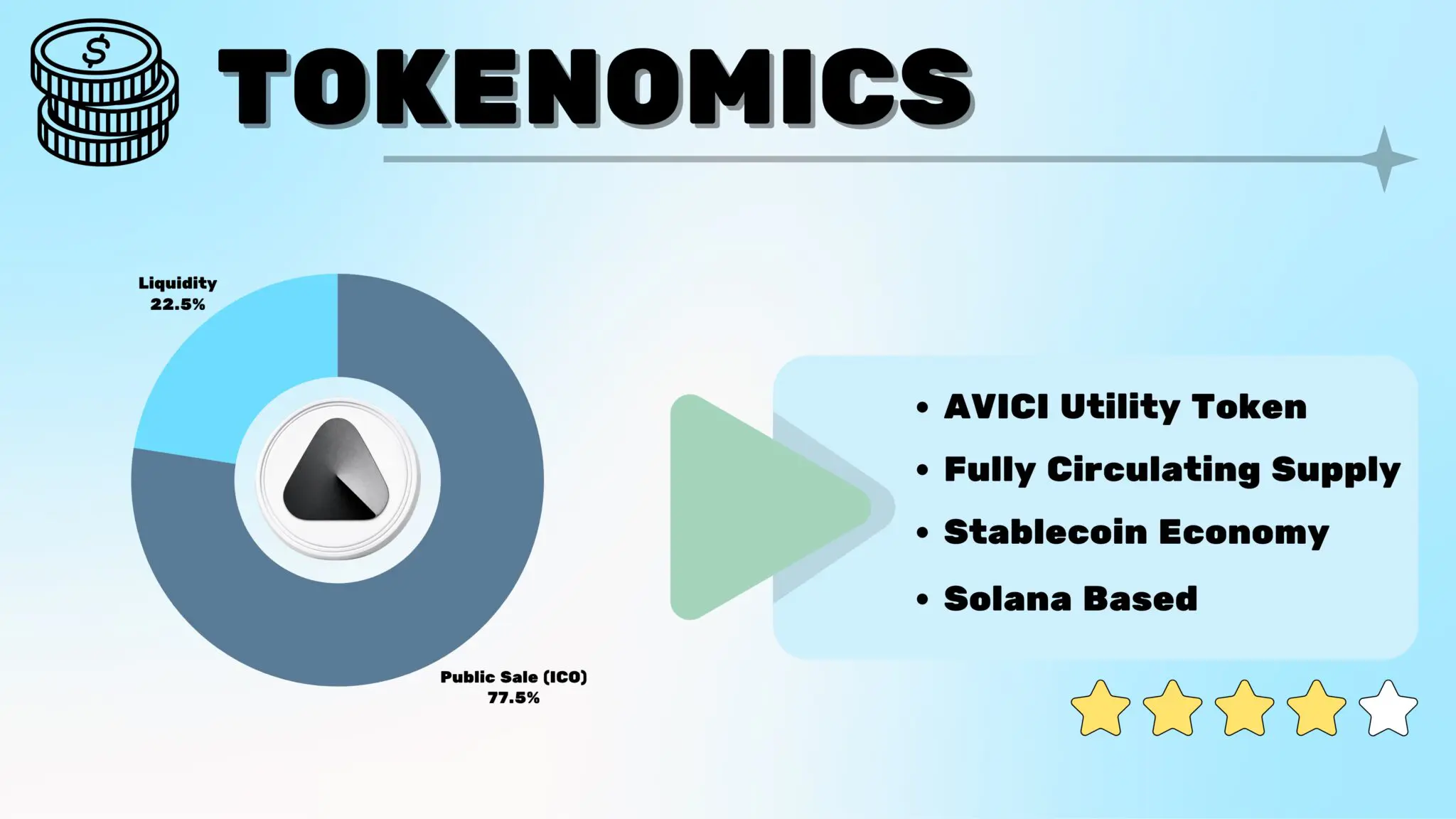

Avici introduces the AVICI token as the utility and economic coordination asset of the Avici ecosystem. The protocol operates on a Solana-native environment, enabling seamless interoperability for crypto payments and credit while aligning incentives with long-term protocol growth, sustainability, and bridging fiat and crypto markets.

The AVICI token functions as the utility, coordination, and value accrual asset of the Avici protocol. It enables ecosystem participation, payments, and access to incentives and rewards.

Avici currently focuses primarily on product infrastructure rather than speculative token economics. The ecosystem is built around stablecoin usage and financial services rather than a traditional utility token model.

Stablecoins such as USDC are used for card balances, spending, and transfers within the platform. Deposits made to card escrow contracts generate corresponding fiat credit balances that can be used for payments.

This design positions stablecoins as the core economic layer of the ecosystem, aligning with the platform’s goal of enabling everyday crypto-based banking.

Avici operates with a product-driven approach focused on building infrastructure for internet-native banking. The project positions itself as part of a broader movement toward decentralized financial systems where users retain full control of their assets.

The long-term governance vision involves expanding the ecosystem toward decentralized coordination while maintaining compliance where required for payment infrastructure.

| Project | Core Focus | Execution Architecture | Programmability | Token Utility | Notes |

|---|---|---|---|---|---|

|

|

The emergence of crypto-native financial platforms reflects a broader shift in how people think about money, custody, and financial access. While blockchain technology introduced the concept of self-sovereign assets, the surrounding financial infrastructure has remained incomplete. Everyday financial tools such as payment cards, bank accounts, and credit systems are still largely controlled by traditional institutions.

Avici attempts to address this gap by combining self-custodial blockchain infrastructure with familiar fintech-style services. Through smart contract wallets, crypto-backed credit cards, and fiat onramp accounts, the platform aims to make stablecoins and digital assets usable for everyday financial activity rather than limiting them to trading or speculation.

Rather than forcing users to abandon traditional financial systems entirely, Avici integrates with existing payment rails such as Visa and bank transfers. This hybrid approach allows crypto holders to interact with the global financial system while maintaining ownership of their assets onchain. If executed effectively, it could lower the barriers that currently prevent crypto from functioning as practical money.

Ultimately, Avici represents an experiment in building a new form of internet-native banking infrastructure. By blending decentralized custody with global payment compatibility, the project aims to move crypto closer to fulfilling its original promise: a financial system where individuals can spend, save, and manage wealth without relying on centralized banks.

Exchange Listings:

Liquidity:

| Decentralized neobank on Solana for self-custodial crypto banking |

| Smart contracts on Solana |

| Full (Rust-based) |

| Governance via DAO with futarchy |

| Raised $3.5M and refunded 90%; app live on iOS and Android; revenue from fees; partnership with MoonPay; virtual accounts plus physical and virtual cards; launched Oct 2025 |

|

| Liquid restaking and yield-bearing stablecoin infrastructure | Smart contracts on Ethereum and multichain deployments | Full (EVM) | Governance, staking (ETHFI) | Strong monthly spend metrics; yield-focused product suite; multichain strategy |

|

| Modular Layer-2 for DeFi and real-world assets | Mantle Network on Ethereum Layer-2 | Full (EVM) | Governance, staking (MNT) | Leads the neobank category narrative; compliance-focused; supports RWA vault structures |

|

| Decentralized lending and borrowing | Smart contracts on Algorand | Full (TEAL) | Governance (FOLKS) | Non-custodial design with focus on emerging market credit access |

|

| Yield optimization and DeFi tooling | Smart contracts on multichain networks | Full (EVM) | Governance (LMTS) | Auto-compounding vault strategies with ongoing multichain expansion |

|

| High-throughput Layer-1 for payments | Plasma consensus with Proof-of-Stake | Full (EVM-compatible) | Fees, staking (XPL) | Low-fee payment focus; enterprise adoption narrative; supply-chain-oriented integrations |