Loading Search...

In this article we go through the entire lawsuit and insider allegations against Jane Street that have shocked the crypto industry.

Author: Sahil Thakur

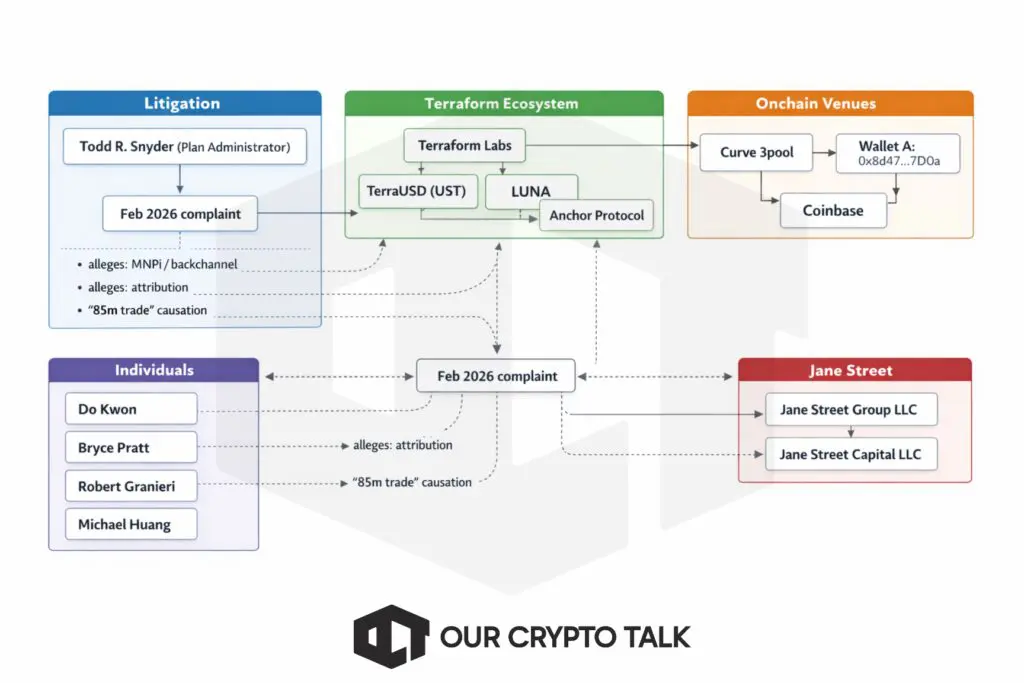

A new civil lawsuit filed on 23 February 2026 in the U.S. District Court for the Southern District of New York claims that Jane Street entities and three individuals traded Terra-related tokens using material non-public information. It also alleges market manipulation tied to the May 2022 TerraUSD (UST) and LUNA collapse.

The plaintiff is Todd R. Snyder. He is acting as plan administrator for a “Wind Down Trust” created under Terraform’s Chapter 11 liquidation plan. He is also an assignee of certain claims from Luna Foundation Guard and individual claimants.

The public version of the complaint runs 83 pages, but large portions are redacted. At least one exhibit it references, “Exhibit A,” which reportedly lists individual victims, does not appear in the public PDF. Because of that, the filing alone leaves key details hard to verify.

Even so, the complaint ties the alleged conduct to a familiar on-chain storyline. It points to a liquidity move by Terraform or Luna Foundation Guard, followed by an “85 million” swap on Curve’s 3pool. The complaint describes that swap as the largest single trade on that pool. It also argues the swap helped trigger a sharp UST sell-off.

Several on-chain analyses cited since 2022 describe a similar sequence. They say an LFG-associated wallet moved roughly 150 million UST. Soon after, a newly created Ethereum address carried out an 85 million UST swap, often labeled “Wallet A” in public write-ups. After that, funds moved onward, including transfers that researchers say went to Coinbase. Importantly, Nansen did not settle on a simple “single attacker” narrative. Instead, it described a de-peg driven by multiple well-funded actors taking advantage of thin Curve liquidity and broader market structure.

Chainalysis described the collapse in stages as well. It said two large traders helped kick off the de-peg. Then came efforts to defend the peg. After that, renewed selling pressure pushed the system into what it called a “death spiral.”

This is where the public-evidence debate gets more complicated. The lawsuit claims the “85 million” activity and related trading tied back to Jane Street, and that it relied on inside information. However, the public on-chain record does not, by itself, prove that Jane Street controlled “Wallet A.” So the public case looks stronger on the order of events than on who owned which wallets. It is also thinner on questions like intent and knowledge.

Separate from the U.S. lawsuit, Jane Street has also faced regulatory action in India. On 4 July 2025, India’s market regulator issued an interim order alleging index-derivatives manipulation. Later reporting said the firm made an escrow deposit to meet conditions to resume trading while continuing to contest the allegations.

People often fold that India case into broader social-media stories about crypto market manipulation. Those posts sometimes cite “10 a.m.” patterns and the 10 October 2025 crash. Still, the public record behind those crypto-crash rumors looks much weaker than the documentation around the SEBI proceeding or the Terra and LUNA on-chain timeline.

Finally, claims that Jane Street “deleted all X posts” took off on social media in late February 2026. Some posts shared screenshots as proof. Others pushed back and argued the account never posted much in the first place. Without independent archives, it is hard to confirm what happened but in this article we discuss everything there is to know about this saga so far.

The lawsuit was filed in the U.S. District Court for the Southern District of New York as Case No. 1:26-cv-01504. In the complaint header, it also appears as “1:26-cv-1504.”

Todd R. Snyder is the plaintiff. He is acting as plan administrator for the Wind Down Trust. The defendants listed in the public complaint are Jane Street Group, LLC; Jane Street Capital, LLC; Bryce Pratt; Robert Granieri; and Michael Huang.

Docket metadata also shows a miscellaneous filing shortly before the civil case. It appears to relate to filing under seal. That lines up with the fact that the public complaint is heavily redacted.

In the complaint, Snyder says he is bringing claims on behalf of three groups. First, Terraform’s post-effective-date debtors and the Wind Down Trust. Second, Luna Foundation Guard. Third, “Individual Victims” listed in “Exhibit A.” However, Exhibit A is not included in the public PDF. Because of that, it is hard to verify the full claimant set. It also makes it harder to check any trade-by-trade schedules, if they exist.

Kirkland & Ellis LLP is listed as counsel for the plaintiff.

In broad terms, the complaint alleges three things. First, it claims Jane Street personnel had backchannel communications with Terraform insiders. Next, it alleges defendants used confidential information obtained through those communications. Finally, it claims defendants traded in ways the complaint describes as market manipulation. The complaint says this conduct worsened the UST and LUNA collapse. It also claims it helped defendants profit or limit losses.

One notable legal move is how the complaint frames the assets. It pleads UST and LUNA as crypto-asset securities under the Exchange Act. At the same time, it argues in the alternative. If the court decides crypto is not a security here, then the complaint asks the court to treat the assets as commodities under the CEA framework.

Redactions show up everywhere in the public version. Many numbered paragraphs have key language missing. Some factual statements appear to be removed entirely. For example, the complaint includes a long explanation of MEV, or maximal extractable value. It suggests MEV matters to the alleged scheme. Still, the surrounding facts that would explain how it ties in are partly redacted.

The complaint leans heavily on Curve pool dynamics. It describes a transition plan from April 2022. Terraform would move UST liquidity from Curve’s 3pool, also called Curve3, to a planned “4pool.” It also notes Terraform announced that Anchor’s roughly 20% yield would begin declining starting 1 May 2022.

Then it points to what it calls “that 85 million trade” on Curve’s 3pool. It describes this as the largest single swap on that pool. It also claims the trade helped spark a steep UST sell-off. From there, it argues, the sell-off cascaded into the broader Terra ecosystem collapse.

The complaint adds another layer after the de-peg begins. It alleges that, during the collapse, Jane Street continued using material non-public information. It says this included information tied to stabilization efforts and fundraising discussions. Also claims defendants used that information to short or trade UST and LUNA further.

The complaint includes 18 counts. They span insider-trading theories, Exchange Act fraud, and controlling-person claims. They also include CEA-based manipulation claims, including aiding-and-abetting theories. In addition, the complaint pleads unjust enrichment.

Snyder demands a jury trial. He also seeks damages and equitable relief. The requested remedies include compensatory damages, punitive damages, treble damages, disgorgement, and attorneys’ fees, among others.

Terraform’s ecosystem revolved around an algorithmic stablecoin, UST, and a related token, LUNA. The two were linked through a mint-and-burn mechanism. That mechanism aimed to keep UST close to $1. The complaint summarizes how this worked. It also makes a clear point: the whole setup depended on market confidence and deep liquidity.

Outside the lawsuit, research and policy sources often describe Terra’s collapse as a fast, run-like dynamic. In other words, once confidence broke, the unwind accelerated. That wiped out tens of billions of dollars. It also shows why algorithmic stablecoins can fall into what many analysts call a “death spiral.”

In the public on-chain narrative, Curve liquidity plays a central role. Stable-swap pools can tolerate normal flows. However, big imbalances quickly change effective prices and slippage. So when liquidity is shallow, the peg becomes easier to break. Nansen’s post-mortem stresses that the Curve pools had relatively shallow liquidity. It treats that as a core vulnerability that got exploited as the de-peg unfolded.

The complaint echoes this framing. It explains Curve 3pool’s importance and notes it was the largest stablecoin pool as of April 2022. It also points out that Terraform planned to move UST liquidity from 3pool to a new 4pool, which mattered because it changed the stability “buffer” available in the market.

Nansen’s 27 May 2022 report reconstructs the May 7–11 window. It flags seven wallets it says were most likely to have played a significant role. One of those is the address 0x8d47…7d0a, labeled “A.”

The key takeaway in Nansen’s write-up is what it does not claim. It does not settle on a single attacker story. Instead, it argues the de-peg likely came from several entities responding to the same weak points. They made withdrawals, bridged funds, and executed swaps. Taken together, those actions stressed the peg and drained liquidity.

In that reconstruction, Nansen says that on May 7 at 21:44 UTC an LFG-associated wallet withdrew about 150 million UST from Curve. After that, it reports an approximately 85 million UST inflow and swap by address “A.” It also notes that the address was newly created, used for the swap, and then sent USDC onward to Coinbase.

Chainalysis’ June 2022 post tells a similar story, but with a different structure. It breaks the collapse into stages. First, it says two traders broke the peg. Next, it describes efforts by Terraform and supporters to restore it. Then it describes renewed selling that overwhelmed the defense, drained supportive buying, and pushed LUNA into hyperinflation. OECD’s “Lessons from the crypto winter” later cites Chainalysis and repeats the idea that the collapse was reportedly triggered by two large trades.

The complaint uses the phrase “85 million trade” and frames it as a turning point. It says the trade precipitated a steep UST sell-off and, from there, the broader collapse. It also places that trade in context. Also points to Terraform’s planned liquidity transition on Curve and the market’s sensitivity to UST stability at the time.

Still, the complaint goes further than public on-chain sources in one major way. It tries to connect motive and identity to the on-chain sequence. It alleges defendants had material non-public information from insiders. Then it says they used that edge to profit, or to avoid losses, while trading around the de-peg.

That jump is the legal heart of the case. But it is also the part chain data cannot prove on its own. To support those claims, the case would need evidence beyond the blockchain. That means things like communications, identities behind wallets, and trading records from centralized venues.

Key milestones related to this development

Complaint references a significant UST de-peg event in May 2021 as an earlier stress test of the peg.

Complaint says Terraform announced Anchor yield would begin decreasing from ~20% starting 1 May and that UST would join a new Curve “4pool,” with plans to prefer it over Curve3/3pool.

Nansen reported an LFG-associated wallet withdrew ~150m UST from Curve; shortly after, address 0x8d47…7d0a swapped ~85m UST and later sent USDC to Coinbase.

Complaint characterizes the “85 million trade” as the largest single swap on Curve 3pool, saying it “precipitated” a steep UST sell-off and that UST volume nearly doubled over the next two days.

Complaint says UST fell below $0.80; Terraform sought stabilization and “surreptitiously enlisted” help from Jump Trading, and alleges a group message to Kwon about bidding for BTC/LUNA at discounted prices.

Complaint lists UST at about $0.42 on 12 May and below about $0.15 on 13 May; LUNA at about $0.001219 on 13 May, describing the “collapse complete.”

Bankruptcy court approval reported for Terraform’s wind-down plan after an SEC settlement, setting a liquidation/distribution framework.

Plan documents/filings describe the plan’s effective date and the Wind Down Trust structure and plan administrator role.

An interim action by India’s regulator alleged index manipulation, described as a major regulatory move against a foreign investor.

Reportedly, Jane Street deposited about $567m into escrow following a SEBI directive, seeking to resume trading while contesting the claims.

FTI Consulting described $19bn+ in liquidations in a day, attributing the move to a “100% China tariff threat” headline interacting with leverage and liquidity, not fraud/insolvency.

A complaint was filed in SDNY alleging insider trading and manipulation around the Terra collapse.

Reputable outlets reported on the lawsuit and the “Bryce’s Secret” allegation; social media amplified new manipulation narratives and wallet-identity claims.

In early July 2025, India’s Securities and Exchange Board of India issued an interim order against Jane Street entities. The order alleges the firm manipulated index levels. Reporting often links the allegation to Bank Nifty constituents. SEBI also claimed “unlawful gains” and imposed restrictions.

Reuters reported that Jane Street deposited about $567 million into escrow under SEBI directives. That deposit reportedly formed part of the conditions to resume trading. At the same time, Jane Street denied wrongdoing. It also described the activity as straightforward index arbitrage.

SEBI’s public materials, including the order and related postings, lay out the regulator’s view. Meanwhile, reporting describes Jane Street as disputing SEBI’s characterization. Some reports also say the firm adopted voluntary limits, such as avoiding certain options until the matter is resolved.

This India case matters here for two reasons. First, it is recent and it comes with public documents. Second, it fuels online narratives that frame the Terra lawsuit as part of a bigger pattern of “institutional manipulation.”

Online claims about “Wallet A” often rely on indirect signals. People point to things like interactions with permissioned DeFi pools, timing overlaps, and assumptions based on exchange clustering. One commonly cited thread came from an analyst associated with Wintermute. Later, The Block referenced it. The thread argued that Clearpool’s permissioned pool announcement helped identify addresses thought to link to Jane Street. It also suggested one of those addresses tied to the “Wallet A” activity.

Still, attribution based on these methods remains uncertain. Unless someone backs it with admissions, subpoenas, or strong clustering evidence with clear methodology, it stays a hypothesis. Nansen’s report maps flows and timing in detail. However, it does not publicly state that address 0x8d47… is definitively Jane Street. In fact, Nansen’s overall framing pushes against a simple “one actor did it” storyline.

A separate set of rumors claims Jane Street caused, or at least amplified, the 10 October 2025 crypto crash. However, the most detailed public write-up often cited for that event, from FTI Consulting, points elsewhere. It attributes the crash to a macro headline, described as a “100% China tariff threat,” colliding with high leverage. It also highlights cross-margin mechanics and a sharp drop in liquidity. Together, those factors produced a liquidation spiral.

FTI also draws a clear contrast with Terra and with FTX. It says this crash did not come from fraud, insolvency, or the failure of one major institution.

Because of that, the public evidence for “Jane Street caused the 10 October 2025 crash” looks thin. The sources summarized here do not cite a regulator finding that names the firm. Instead, the strongest post-mortems focus on leverage and liquidity structure, not a specific actor. Even so, the rumor persists. It tends to spread through social-media inference rather than primary documentation.

In late February 2026, viral posts claimed Jane Street deleted all posts from its official X account. Many of those posts implied the firm acted in response to the Terra lawsuit or broader manipulation claims.

Soon after, other users disputed the story. Some said the account never posted much to begin with. Others argued the “deleted all posts” claim was simply wrong. A few aggregation accounts also framed the story as potentially false.

From an evidence standpoint, this is a weak signal without independent archives, such as third-party tweet archiving or a platform transparency record. Also, even if deletion happened, deletion alone does not prove wrongdoing. At most, it suggests a communications choice while the firm faced scrutiny.

Jane Street describes itself as a quantitative trading firm and liquidity provider. It emphasizes electronic trading, competitive pricing, and proprietary technology. It also notes that its U.S. services run through registered broker-dealer entities.

More broadly, a market maker provides liquidity. It does that by constantly quoting two prices: a price to buy and a price to sell. Those are the bid and the ask. The market maker can earn the spread between them. At the same time, it takes on inventory risk, because it may end up holding assets while prices move.

In calm markets, market makers can lower transaction costs. They can also help trades get filled faster and at tighter prices. However, during market stress, their behavior gets more attention. That is because liquidity can vanish quickly, and people start debating what “fair” trading looks like in a crisis.

For a sense of scale, the SEC’s 2020 staff report on algorithmic trading listed Jane Street Capital LLC in transparency-based breakdowns for OTC and ATS activity. That placement reflects how prominent large electronic liquidity providers are in modern markets.

ETFs have a specific piece of plumbing that many people miss. It involves “authorized participants,” often called APs. These are usually large broker-dealers. They can create and redeem ETF shares in large blocks called creation units.

Here is how it works in practice. An AP can deliver a basket of underlying assets, plus any required cash, and receive newly created ETF shares. It can also do the reverse. It can redeem ETF shares and receive the underlying basket back. This process is a form of arbitrage. Over time, it helps keep an ETF’s market price close to its net asset value.

This matters for online narratives because people sometimes mix up two different things. First, there is normal AP arbitrage and hedging. That can include shorting, using futures, or leaning on correlated products to manage intraday risk. Second, there is manipulation, which implies deceptive conduct or intent.

SEC materials discuss that APs may hedge while doing arbitrage. So yes, AP behavior can line up with short-term price pressure. Still, that does not automatically mean wrongdoing. To prove manipulation, you usually need more than the mechanical footprint of hedging.

Public reporting and primary documents point to a few categories of crypto involvement.

DeFi credit and Clearpool: In May 2022, CoinDesk reported that Jane Street borrowed $25 million in USDC through Clearpool, in a transaction involving BlockTower. The reporting framed this as an institutional DeFi moment, tied to Clearpool’s permissioned pool model. Bloomberg also reported Jane Street using DeFi to borrow crypto through Clearpool. In addition, ConsenSys commentary later referenced the same episode as an example of institutional activity.

Market-making pullbacks under U.S. regulatory uncertainty: Bloomberg reported in May 2023 that Jane Street and Jump pulled back from U.S. crypto trading amid regulatory uncertainty. It also described Jane Street as scaling back broader crypto ambitions around that time.

ETF-adjacent roles: Some SEC-filed prospectus documents for certain bitcoin products list an affiliate such as JSCT, LLC as a “Bitcoin Trading Counterparty.” They also state that an affiliate, Jane Street Capital, LLC, serves as an authorized participant for the fund.

Pyth Network: Pyth’s public materials have listed various market participants as data publishers or providers. Jane Street has appeared among those listed participants in Pyth documentation.

Put together, this suggests a mixed crypto footprint. It includes proprietary trading and liquidity provision. It also includes ETF-related infrastructure roles. Finally, it includes selective DeFi participation, mainly in borrowing or credit.

Sam Bankman-Fried worked at Jane Street Capital before he founded Alameda Research in 2017. He later founded FTX. Reuters’ 2022 profile says he traded currencies, futures, and ETFs at Jane Street. It also says he left after more than three years to move into crypto trading. Separately, an MIT Sloan teaching case says he took a job at Jane Street after graduating from MIT.

So the connection is mostly biographical. It is also about networks and talent pipelines. In other words, Jane Street sits in the broader “quant trading” ecosystem that produced several crypto trading founders and executives. However, that link alone does not show any operational connection between Jane Street and misconduct at FTX.

This section scores what the public can observe today. It does not score what might exist under seal or what could emerge in discovery.

Attribution (Jane Street ↔ Wallet A / 0x8d47…): Weak to Medium

Public chain analysis strongly supports the flow sequence. However, the key jump, “this wallet belongs to Jane Street,” is not established in Nansen’s public work. Other attributions mostly come from analyst hypotheses. To solidify attribution, you would need corroboration like exchange KYC, subpoenas, internal records, or admissions.

Scienter / MNPI misuse: Weak (publicly)

The complaint alleges inside channels and misuse of material non-public information. Still, the public copy is heavily redacted. Some referenced exhibits are missing. Because of that, the public cannot evaluate the actual communications or the intent behind them.

Causation (85m swap -> de-peg -> collapse damages): Medium

There is strong support that large Curve swaps and liquidity shifts coincided with destabilization. However, credible analyses also emphasize multi-actor and multi-factor dynamics. That includes liquidity depth, arbitrage behavior, and broader market stress. As a result, “but for this trade, the collapse would not have happened” becomes harder to prove cleanly. Proximate cause questions also get more complicated.

Because the complaint mixes securities, commodities, and state-law theories, several hinge points are likely to drive the case. These are not outcome predictions. They are simply the areas where the case often tightens or breaks.

Classification and jurisdiction questions

The complaint pleads UST and LUNA as securities. It also pleads, in the alternative, that they should be treated as commodities. So one early fight may be about legal classification and statutory reach. Another fight may be about whether the alleged conduct fits the relevant standards under the Exchange Act or the CEA.

Pleading sufficiency, especially with redactions

For Exchange Act claims, courts often scrutinize scienter and loss causation. That makes the redactions a practical problem for public evaluation. In other words, the real question is how much detail exists in the unredacted version. If the sealed material is thin, motions to dismiss become more dangerous. If it is detailed, the case may survive longer.

Causation and damages

Even if inside trading were proven, defendants can still argue the collapse came from structural fragility. They can point to design weaknesses, reflexive dynamics, and actions by multiple large market participants. That line of defense aims to narrow, or even break, damages causation.

Discovery focus if the case survives early motions

If the case clears the first procedural hurdles, discovery likely becomes the main battlefield. It would likely center on chat logs and emails, venue trade records, wallet-ownership evidence, and internal documentation about risk and intent.

This is neutral scenario analysis. It is not a conclusion of fact.

Reputational

Being tied to a high-salience crypto collapse and a high-profile regulator action can increase scrutiny. That said, large market-making firms often maintain strong franchises if performance stays strong and counterparties remain satisfied with their compliance posture.

Regulatory and compliance

The India proceeding, plus any related inquiries mentioned in reporting, could raise compliance costs. It could also create restrictions in certain jurisdictions, depending on outcomes and conditions imposed.

Operational posture toward crypto

Jane Street has been reported to pull back from parts of crypto trading during regulatory uncertainty. Litigation pressure can reinforce that stance. It can also push activity toward cleaner, more regulated lanes, like ETF-linked roles or other clearly defined market structure positions.

Litigation outcomes

Outcomes range from dismissal to settlement to trial. Settlement is common in complex financial litigation, even when liability is disputed. Still, the public record is too incomplete to responsibly assign probabilities today.

If you want to know what would actually change the public evidence picture, it is mostly this:

Wallet attribution proof

The single biggest upgrade would be KYC-based linkage between 0x8d47…7d0a and a real-world beneficial owner. That could come from subpoenas to centralized exchanges tied to the flow path, including deposit endpoints.

Unredacted communications

Full chat logs, email chains, and internal messages are central. If the case has real MNPI, it likely lives there. If it does not, that will show up there too.

Trade blotters across venues

Complete spot and derivatives histories across exchanges during the key May 7–13 window would help. So would correlated hedges and stablecoin activity. That is how you test “profit” or “loss avoided” claims.

Event-study style causation analysis

A serious reconstruction would combine Curve pool state with CEX order books and derivatives funding and liquidation data. That lets you test the complaint’s causal story against alternative explanations built around leverage and liquidity structure.

Redaction gap mapping over time

As filings become unsealed, a systematic comparison between the redacted and unredacted versions would matter. It would show what facts were removed and whether those facts meaningfully strengthen, or weaken, the MNPI and intent narrative.

The next few moves in this case will likely be procedural. However, those early steps can still reveal a lot.

First, watch the docket for sealing fights and any moves to unredact key sections. Right now, the public complaint leaves big gaps. If the court orders more disclosure, you may finally see what the plaintiff says supports wallet attribution and insider-channel claims. On the other hand, if sealing stays broad, the public narrative will remain mostly inference-heavy.

Next, focus on the first wave of motions to dismiss. Defendants will probably test standing, jurisdiction, and pleading sufficiency. They may also attack scienter and loss causation early, since those are common pressure points in market cases. In parallel, expect arguments over what legal regime even applies. The complaint pleads securities theories and, alternatively, commodities theories. So classification and statutory reach can become a hinge.

Then, track any signals about wallet attribution. This is the fulcrum for public confidence in the story. If subpoenas go out to centralized exchanges tied to the on-chain flow, the case can change shape fast. Even a small, well-supported attribution detail can outweigh pages of speculation. Conversely, if attribution stays circumstantial, the plaintiff may lean harder on communications and trading records.

Also watch for discovery disputes over communications. If the case survives early motions, fights over chat logs, emails, and internal messages will likely get intense. Timing matters here. A court order compelling production can create momentum. So can credible allegations of spoliation, or a clean showing that records were preserved.

Causation will be another battleground. Expect both sides to bring event-study style analyses. The plaintiff will try to tie the Curve swap, liquidity conditions, and market impact into a clear chain. Defendants will likely emphasize multi-actor dynamics and Terra’s design fragility. That debate will shape any settlement posture.

Finally, keep an eye on parallel pressure. Regulatory developments, especially outside the U.S., can shift incentives even if they are not legally decisive in this case. And if credible reporting surfaces new primary documents, the public narrative could swing quickly.

In short, the “next evidence” to watch is not a hot take. It is unredactions, motions, subpoenas, and records. Those will decide whether this stays a theory-heavy dispute or becomes a document-driven case.