Loading Search...

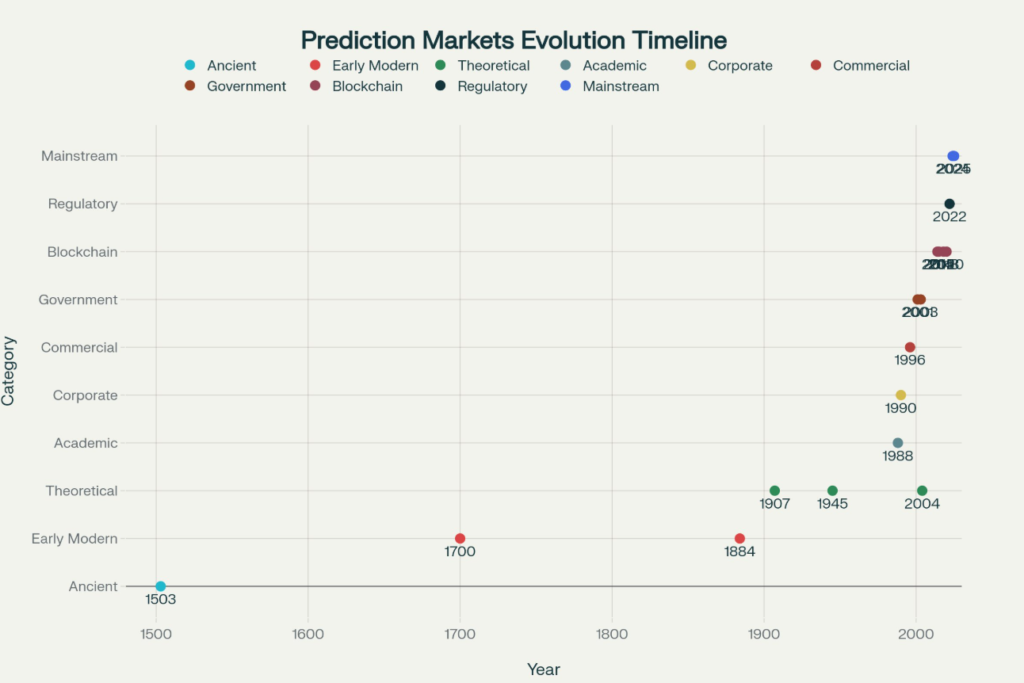

Prediction markets accuracy shows how crowds outperform experts, from historic betting to modern platforms like Polymarket.

In an era overloaded with forecasts and opinions, prediction markets accuracy has quietly emerged as one of the most reliable mirrors of collective expectations. Unlike polls or punditry, prediction markets convert sentiment into monetary stakes, and every forecast carries a price for being wrong a dynamic that further reinforces prediction markets accuracy in real time.

The outcome is a highly efficient system for aggregating information, often outperforming traditional models, institutions, and even AI-driven predictions. What began centuries ago with nobles in Renaissance Italy betting on papal succession has evolved into blockchain-powered platforms like Polymarket, now valued at over $9 billion, where data and belief intersect.

When Polymarket forecasted Donald Trump’s 2024 win with 94% accuracy while major polls called it a toss-up, it showed one thing clearly: truth sharpens when conviction carries financial weight.

Long before Silicon Valley turned collective intelligence into code, people were already using markets to transform private knowledge into public insight. The earliest prediction markets weren’t experiments in theory, they were instruments of power.

In 1503, nobles, merchants, and Vatican insiders in Italy traded odds on who would wear the next crown of Saint Peter. These were not idle bets but proto–information markets, early systems whose behavior already hinted at prediction markets accuracy by aggregating rumors, alliances, and political signals from across Europe.

Their influence became so strong that in 1591 Pope Gregory XIV threatened excommunication for anyone caught betting on the papal conclave, not out of moral outrage, but because markets had begun to rival divine secrecy itself.

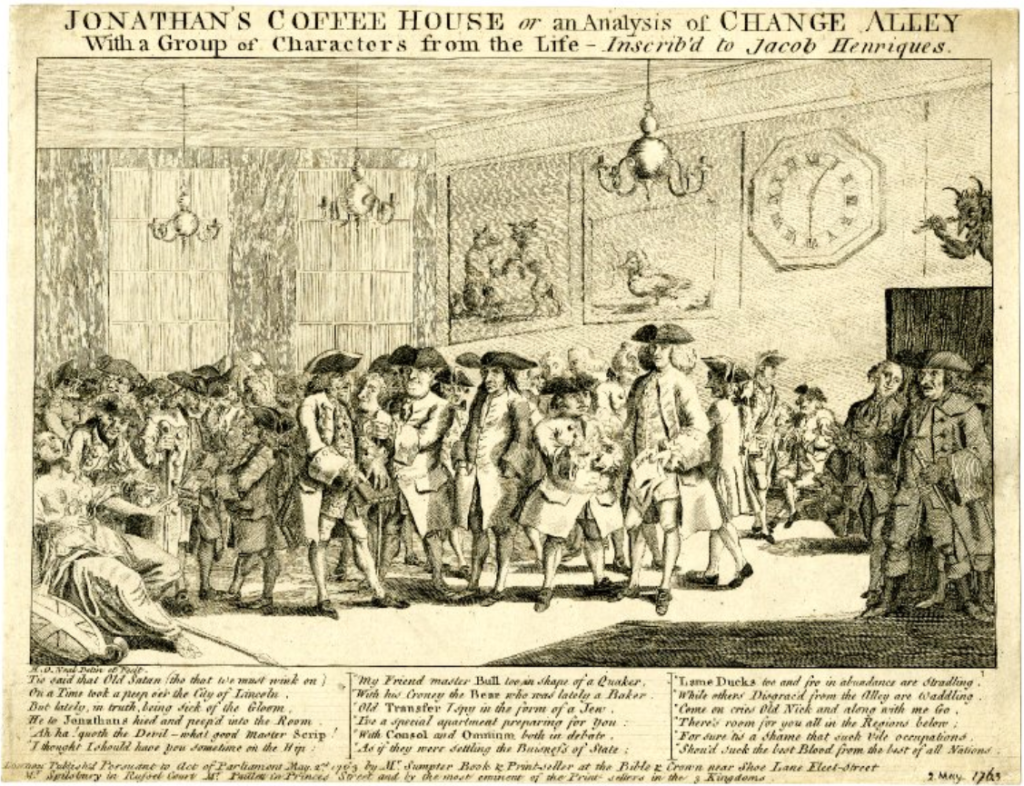

By the 18th century, London’s coffeehouses had become the nerve centers of political speculation. At Jonathan’s Coffeehouse, later the birthplace of the London Stock Exchange, traders and aristocrats exchanged contracts on everything from cabinet reshuffles to parliamentary scandals. Newspapers soon published the odds, creating early public polling that reflected a primitive form of prediction markets accuracy in how these wagers aggregated political sentiment.

Among the most notorious players was Charles James Fox, the firebrand Member of Parliament who bet on everything from the repeal of the Tea Act to the outcome of the American Revolution.

When his fortune collapsed, forcing a massive bailout from his father, Fox became the first cautionary tale of market conviction gone wrong, a reminder that while prediction markets capture collective wisdom, they also price in collective error.

Jonathan’s Coffeehouse in London, bustling with traders and aristocrats in the 18th century

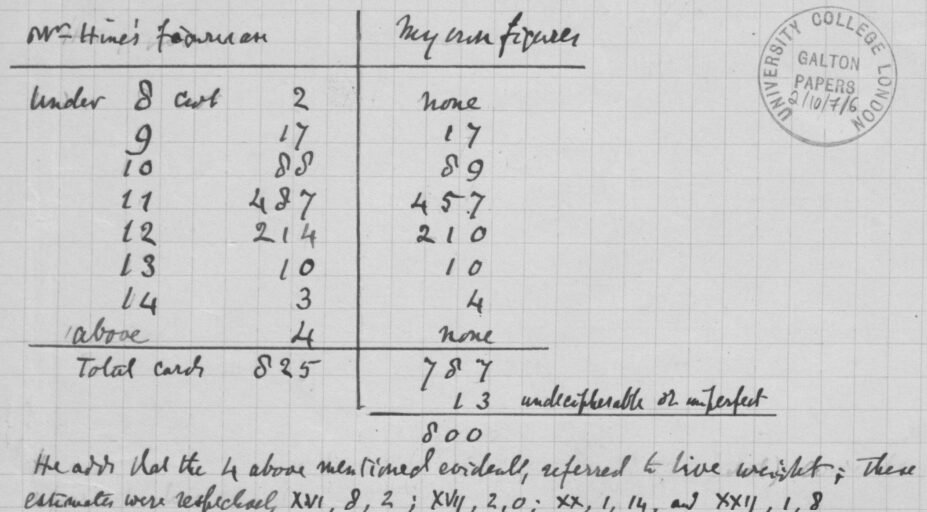

The intellectual roots of modern prediction markets trace back not to economists or financiers, but to a Victorian polymath at a county fair. In 1907, Francis Galton attended an agricultural show in Plymouth, where visitors were invited to guess the weight of a slaughtered ox.

After analyzing 787 submissions, Galton found something remarkable: while individual guesses diverged widely, the median, 1,207 pounds, was only nine pounds away from the actual weight of 1,198. This less than one-percent margin of error — achieved not by experts but by ordinary fairgoers — became an early demonstration of the principles that drive prediction markets accuracy today.

From this experiment emerged a revolutionary idea: that under the right conditions, the collective judgment of a diverse crowd can outperform even the most informed individual. Independence of thought, diversity of perspective, and a mechanism for aggregation. Together, they formed what Galton called “the wisdom of crowds”.

What began as a simple curiosity became the conceptual foundation for prediction markets. Systems that now extend Galton’s insight from a village fair to the digital frontier of collective intelligence.

Francis Galton’s 1907 experiment

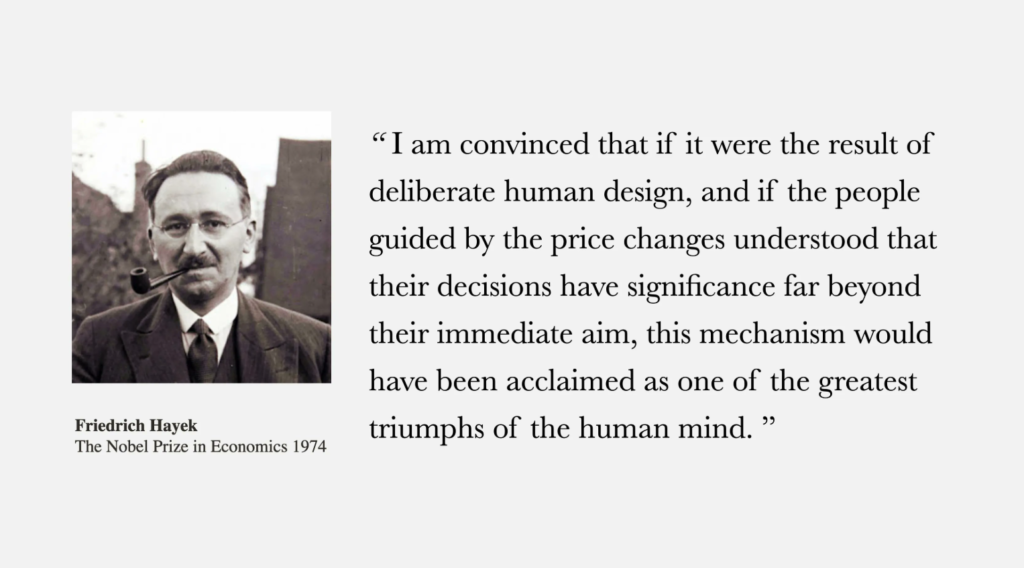

If Galton revealed that crowds could be wise, Friedrich Hayek explained why. In his landmark 1945 essay “The Use of Knowledge in Society”, the Austrian economist reframed the central question of economics: the challenge wasn’t how to distribute scarce resources, but how to coordinate scarce information.

Hayek’s insight was disarmingly simple. No single mind, institution, or government could ever hold all the knowledge needed for efficient decision-making. Information exists in fragments, dispersed among millions — a farmer seeing weather shifts, a shopkeeper tracking changing habits, a miner sensing shortages before others do — the very distributed knowledge that later became the foundation of prediction markets accuracy.

Markets, Hayek realized, are the mechanism that stitches those fragments together. Prices aren’t mere numbers; they are signals transmitting knowledge faster than any planner or committee ever could. As he wrote:

“Without an order being issued… tens of thousands of people are made to use the material more sparingly”.

That realization became the intellectual foundation for modern prediction markets. If traditional markets aggregate knowledge about what is, prediction markets extend that function to what might be. In Hayek’s framework, markets weren’t just for trading goods, they were networks for collective intelligence.

The modern prediction market era began not on Wall Street, but in a university lab. In 1988, a group of economists at the University of Iowa set out to test Hayek’s ideas in practice. Their creation, the Iowa Electronic Markets (IEM), became the first structured system built purely for forecasting rather than trading physical goods, offering an early proof of prediction markets accuracy in real-world academic research.

By the early 1990s, prediction markets had moved beyond academia into the corporate arena. Economist Robin Hanson, later one of the field’s defining figures, launched the first internal market at the software company Xanadu in 1990. His idea was straightforward: instead of asking executives or consultants to forecast outcomes, let employees bet on them.

Could the team deliver on time? Would the new feature hit its adoption target? How likely was a competitor to enter the same space? Each contract carried only a small monetary stake, but the aggregate signal it produced proved far more reliable than meetings or memos.

The concept quickly caught on in Silicon Valley. Google, Microsoft, Intel, and General Electric all tested internal markets to forecast launches, deadlines, and sales. These experiments often surfaced what employees privately believed but never voiced — that timelines would slip, budgets would shrink, or demand would underperform.

Soon, other sectors followed. Engineering firms used markets to predict project delays; sales teams converted intuition into more accurate forecasts than their CRM dashboards; financial institutions applied them to regulatory and volatility risks. The underlying insight spread fast: information isn’t hidden, it’s just misaligned with incentives.

Yet Hanson noticed a paradox. Despite consistent accuracy, many companies quietly shut down these markets. The problem wasn’t data, it was power. When truth challenges hierarchy, even the most rational organizations tend to look away.

While academics and corporations explored prediction markets for research and management, entrepreneur Max Keiser saw their potential in entertainment. In 1996, he launched the Hollywood Stock Exchange (HSX) — a digital platform where users traded virtual shares of movies, actors, and directors based on expected box office performance.

What began as a game soon became a forecasting engine. By 2007, HSX had correctly predicted 32 of 39 Oscar nominees and seven of eight winners in major categories. When a “moviestock” traded at H$40, it implied an expected box office of $40 million in the film’s first four weekends — a striking example of prediction markets accuracy, as the crowd was right more often than not.

Beneath the novelty was a serious insight: even in entertainment, markets could extract predictive power from collective sentiment. Streaming platforms began mining such data to guide content investments, studios optimized marketing spend by region and demographic, and talent agencies benchmarked stars’ commercial value through moviestock prices. Production companies even tracked Oscar markets to fine-tune awards-season campaigns.

The experiment was so effective that Cantor Fitzgerald sought to extend it into real-money box office futures. The U.S. Commodity Futures Trading Commission approved the idea in 2010, but fierce opposition from the Motion Picture Association of America, citing manipulation risks, shut it down before launch.

Still, HSX foreshadowed a deeper truth: markets could forecast not only politics and profits, but culture itself.

The most ambitious and ultimately disastrous experiment in prediction markets came not from Wall Street or Silicon Valley, but from the Pentagon. In 2001, the Defense Advanced Research Projects Agency (DARPA) launched the Policy Analysis Market (PAM), an initiative designed to forecast political and security developments across the Middle East.

The logic was deceptively simple: if markets could predict elections and box office outcomes, why not apply the same mechanism to terrorism, coups, and regime changes? PAM aimed to create a market in the future of the Middle East, where intelligence analysts, academics, and regional experts could trade futures tied to potential geopolitical events.

What DARPA viewed as an innovative forecasting tool, the public perceived as deeply unethical. Within weeks, PAM was condemned as a “terrorism futures market” and an “assassination exchange.” Critics accused the project of turning human tragedy into speculative profit. Senator Tom Daschle called it “an incentive to commit acts of terrorism”, while others went further, describing it as “a Pentagon-approved life insurance policy for would-be assassins”.

Despite strong defenses from Robin Hanson and other economists, who argued that the outrage stemmed from misunderstanding how such markets operate, the political backlash proved fatal. PAM was terminated in August 2003, never reaching live deployment.

The episode marked a turning point in the public perception of prediction markets. The failure lay not in the mechanism itself, but in society’s unease with applying market logic to morally charged questions — a boundary that still shapes the debate over where prediction markets belong.

When blockchain entered the scene in the 2010s, it promised to fix the core flaws of early prediction markets — regulation, censorship, and central control. The most ambitious attempt came in 2014, when Jack Peterson and Joey Krug founded Augur, the first fully decentralized prediction market built on Ethereum.

Augur replaced human intermediaries with smart contracts. Market creation, trading, and settlement were all handled automatically on-chain, with outcomes verified through the REP (Reputation) token — a mechanism meant to reward honest reporting and punish manipulation. In theory, it was censorship-proof, borderless, and transparent.

In practice, it exposed the social limits of decentralization. When Augur finally launched in 2018 after raising over $5 million, users immediately began creating unethical markets — including “death pools” on public figures. Within a month, daily activity collapsed from 265 users to just 37.

Even with upgrades in Augur v2, faster settlement, better UX, and oracles, adoption never recovered. The experiment proved a hard truth: decentralization solves technical problems, but not human ones.

While Augur chased the vision of a public marketplace, Gnosis, founded in 2015, took a quieter but ultimately more durable path. Instead of building a product for end users, it focused on the infrastructure layer — creating the Conditional Tokens Framework, a technical standard that made complex, composable prediction markets possible.

That choice paid off. By focusing on architecture rather than competition, Gnosis became the unseen backbone for the next generation of forecasting platforms — including the one that would redefine the entire space: @Polymarket

Read more about this in a great study by @danrobinson 👇🏼

Collateralization and lending brought another leap forward. Positions in prediction markets can now serve as collateral for loans, allowing traders to borrow against potential winnings before outcomes are resolved. The result: leverage, capital efficiency, and deeper market participation.

Cross-chain interoperability and smart-contract automation have since pushed prediction markets to a truly composable frontier. Traders can access them across chains, move assets via bridges, and deploy algorithmic strategies that hedge or rebalance positions autonomously.

Prediction markets are no longer isolated experiments. By absorbing the logic of DeFi, they have become dynamic systems of financial intelligence, fusing speculation, liquidity, and automation into a single, composable layer of on-chain coordination.

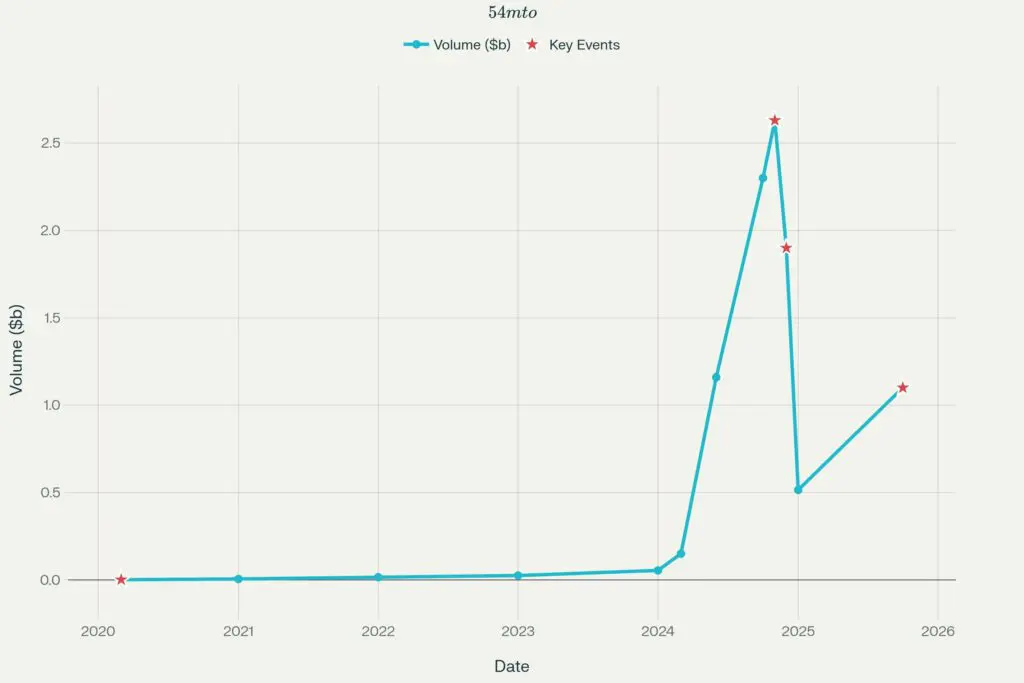

Among all blockchain experiments, Polymarket stands as the clearest proof that prediction markets can operate at scale. Founded by Shayne Coplan (@shayne_coplan), who began developing the project from a small apartment setup at age 22, the platform has since grown into a $9 billion ecosystem. It has processed over $9 billion in total trading volume, including $3.3 billion on the 2024 U.S. presidential election alone.

Polymarket distills complex forecasts into a binary format: a simple yes-or-no question priced between $0 and $1. This minimalism is its superpower. It lets users trade intuitively while aggregating information from thousands of independent opinions into strikingly accurate probabilities.

Polymarket’s Exponential Growth: Trading Volume and User Metrics (2020-2025)

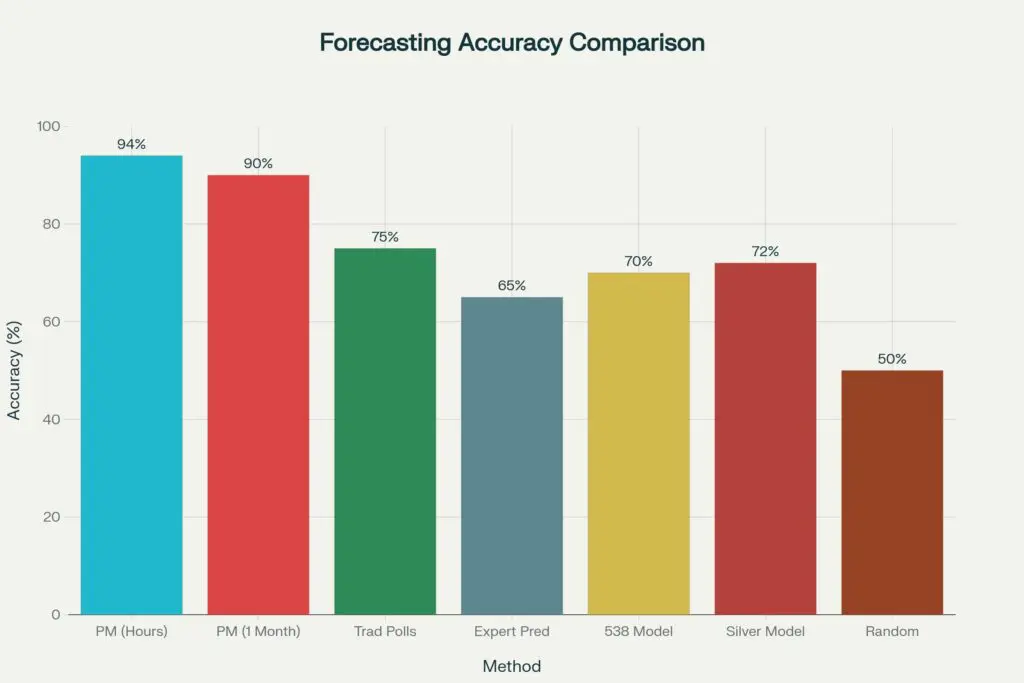

In head-to-head comparisons with polls and analysts, Polymarket consistently delivers stronger forecasts. Studies show its markets reach about 90% accuracy one month before an event, climbing to 94% just hours before outcomes are finalized.

Polymarket vs Traditional Forecasting: Accuracy Comparison

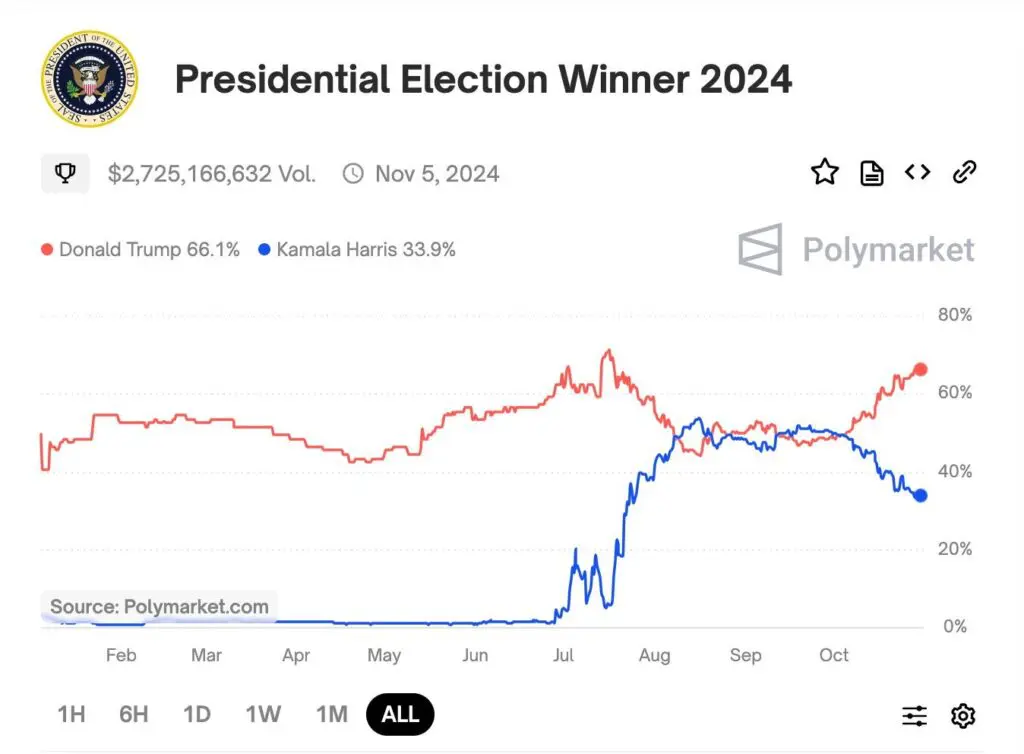

The 2024 U.S. presidential election was the ultimate test. While traditional polls suggested a dead heat between Trump and Harris, Polymarket’s odds had favored Trump for weeks, and by midnight on election night, the platform had already priced in his victory. Major media outlets didn’t confirm it until 6 a.m. the next morning.

Even at the state level, its predictive edge held firm. It outperformed pollsters in Arizona, Georgia, North Carolina, and Nevada — all key battlegrounds where survey data proved unreliable.

What this demonstrated wasn’t just technical precision, but behavioral insight: when people trade on beliefs rather than declare them, the noise fades and information converges toward truth.

Polymarket prediction market odds for the 2024 U.S. presidential election, showing Donald Trump leading over Kamala Harris through market trading volume of $2.7 billion

Prediction markets have quietly become a strategic data layer for industries far beyond crypto.

<> In journalism, major outlets now cite Polymarket odds alongside polling averages, using them to track narratives, anticipate storylines, and gauge real-time public sentiment. Editors monitor market movements for instant signals on breaking events.

<> In corporate risk management, firms use markets to quantify uncertainty — hedging exposure to policy shifts, regulatory outcomes, and supply chain disruptions. Markets serve as an early-warning system that traditional models often miss.

<> In finance, hedge funds and algorithmic traders incorporate Polymarket data into their models for event-driven strategies. It provides a probabilistic layer that complements macro indicators and helps identify mispriced political or economic risk.

<> And in academia, universities and think tanks use internal markets to forecast everything from research breakthroughs to enrollment numbers, while conferences experiment with markets to predict paper acceptances and award winners.

Across these fields, Polymarket has evolved from a crypto experiment into a new kind of information infrastructure, one that doesn’t just report the future, but lets anyone trade on it.

From papal elections in Renaissance Italy to blockchain markets, the story of prediction markets traces a single human obsession — to see the future more clearly. Over five centuries, that impulse has evolved from bets and rumors into code and data, yet the goal remains unchanged: better collective decisions.

Today, the evidence is undeniable. Well-designed prediction markets consistently outperform experts, polls, and pundits. But with that precision comes responsibility. As they scale into multi-billion-dollar ecosystems, these systems must confront a question of purpose: what kind of intelligence do they serve — democratic or technocratic, open or exclusive?

Their convergence with AI and DeFi introduces unprecedented potential: autonomous markets capable of hedging risk, forecasting global events, and guiding strategy across industries. Yet that potential depends on intent, on whether we use these systems to enhance human judgment or to replace it.

The future of prediction markets mirrors the future of democracy itself, a tension between participation and power, openness and control. The lesson Francis Galton revealed in 1907 still applies:

The crowd can be wise, but only if it remains truly collective.

That is both the promise and the peril of the prediction market revolution.

scrip-kid | educator | prediction maker | ugc creator | streamer | part of @zscdao

https://t.co/ceLwHmHr7X