Loading Search...

Web3 neobanks bridge crypto and real-world finance, enabling stablecoin payments, fiat integration, DeFi yield, & global remittance at scale.

The best use case of cryptocurrencies/digital assets is payment and neobanks have made this vision a reality for global remittance.

TL;DR: Stablecoins are already the most killer crypto innovation, neobanks are that distribution layer, abstracting wallets and rails into familiar apps that turn onchain dollars into everyday payments, cards, salaries, and subscriptions. Neobanks essentially merge crypto with real-world use cases and quietly replace legacy banking systems with more advanced systems.

Don’t get fooled by the prefix “Neo”; they are basically banks, but digital-only banks and not like your regular traditional banks you visit often, begging for a transfer limit increase or stating what you want to use your money for when requesting withdrawals.

Don’t get me wrong here, we also have traditional Neobanking in Web2, often referred to as a fintech bank.

Neobanks in Web3 span every sector, concatenating blockchain integration, cryptocurrencies, DeFi and self-custody. They enable crypto-native services, enabling seamless integration between Fiat and digital assets. Neobanks are leveraging blockchain for secure, transparent transactions, and some platforms also use AI to automate processes such as automated trading and asset management, real-time fraud detection, AI-powered KYC/AML compliance, and Improved credit risk assessment.

Neobanks are often preferred over traditional banks because of their flexibility, which extends beyond the following:

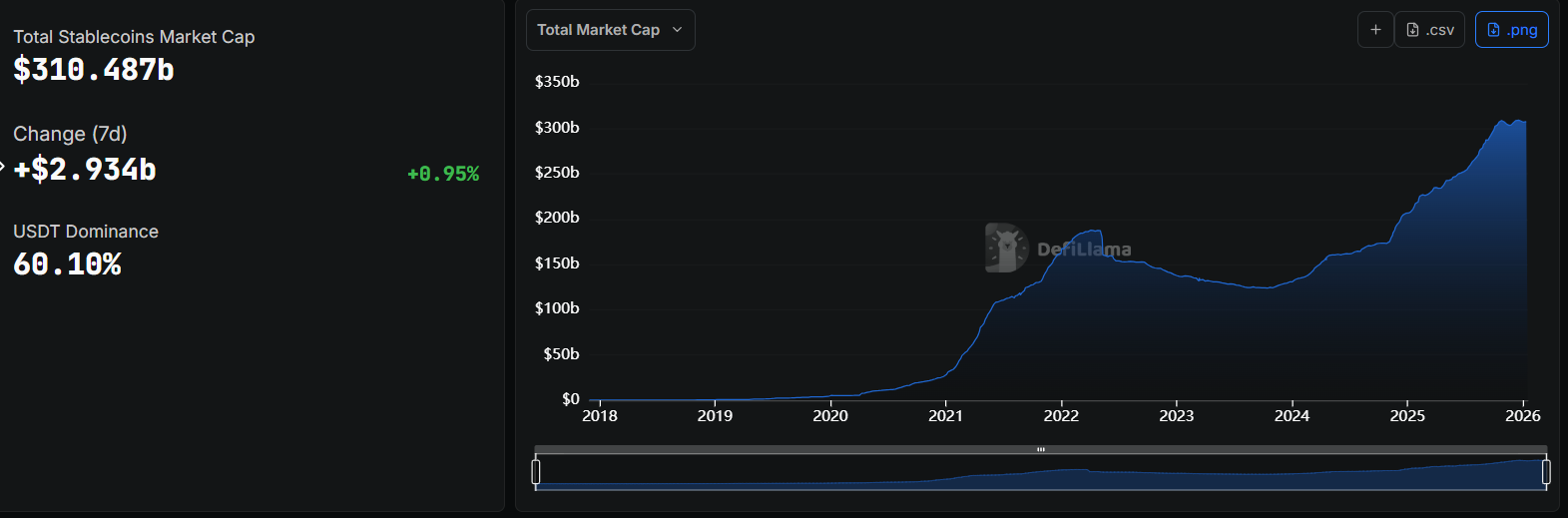

The Web3 Neobank is projected to reach a value of $30- $40B by 2030. We’ve seen their proliferation, which can be attributed to the rise of stablecoin adoption.

According to DefiLlama, the current total stablecoin market cap is $ 305B.

Using the 2030 Neobank estimated value projection with the current stablecoin market cap, this represents about 9.8% – 13.1% of the total stablecoin market and we are bound to see more stablecoin adoption with this number growing and comparing to the percentage, we can see much upside here and a vast gap that Neobanks need to fill and this shows we are super super early.

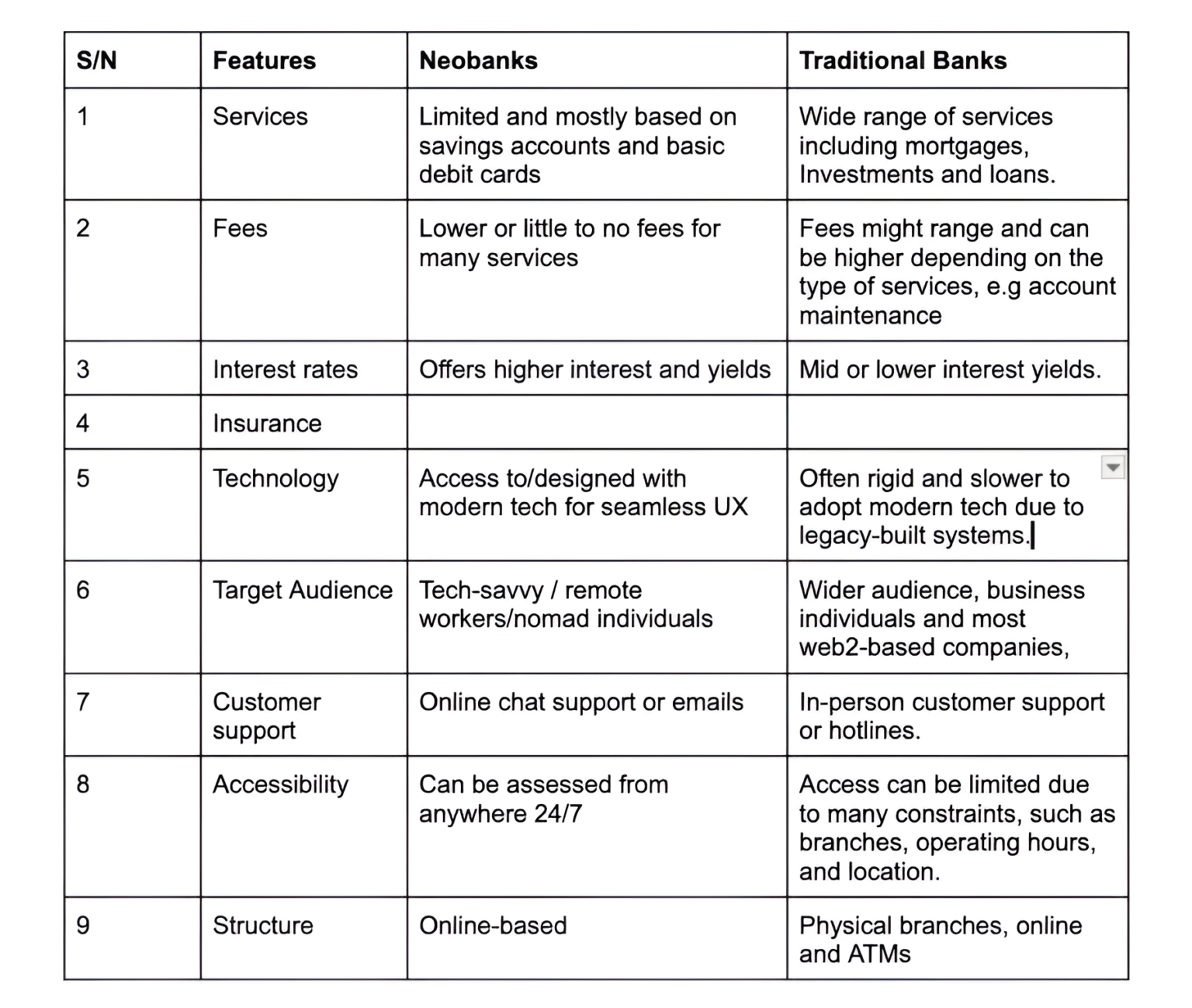

Traditional Banks, as we know, have been the most common form of banking before the rise of neobanks. Neobanks differ from conventional banks in many ways, primarily by operating entirely online, offering lower fees, and featuring technology-driven features. At the same time, the latter offers a full suite of services, including physical branches, and provides in-person customer support.

This is an interesting comparison that highlights the differentiator between Neobanks and Traditional (Conventional) banks.

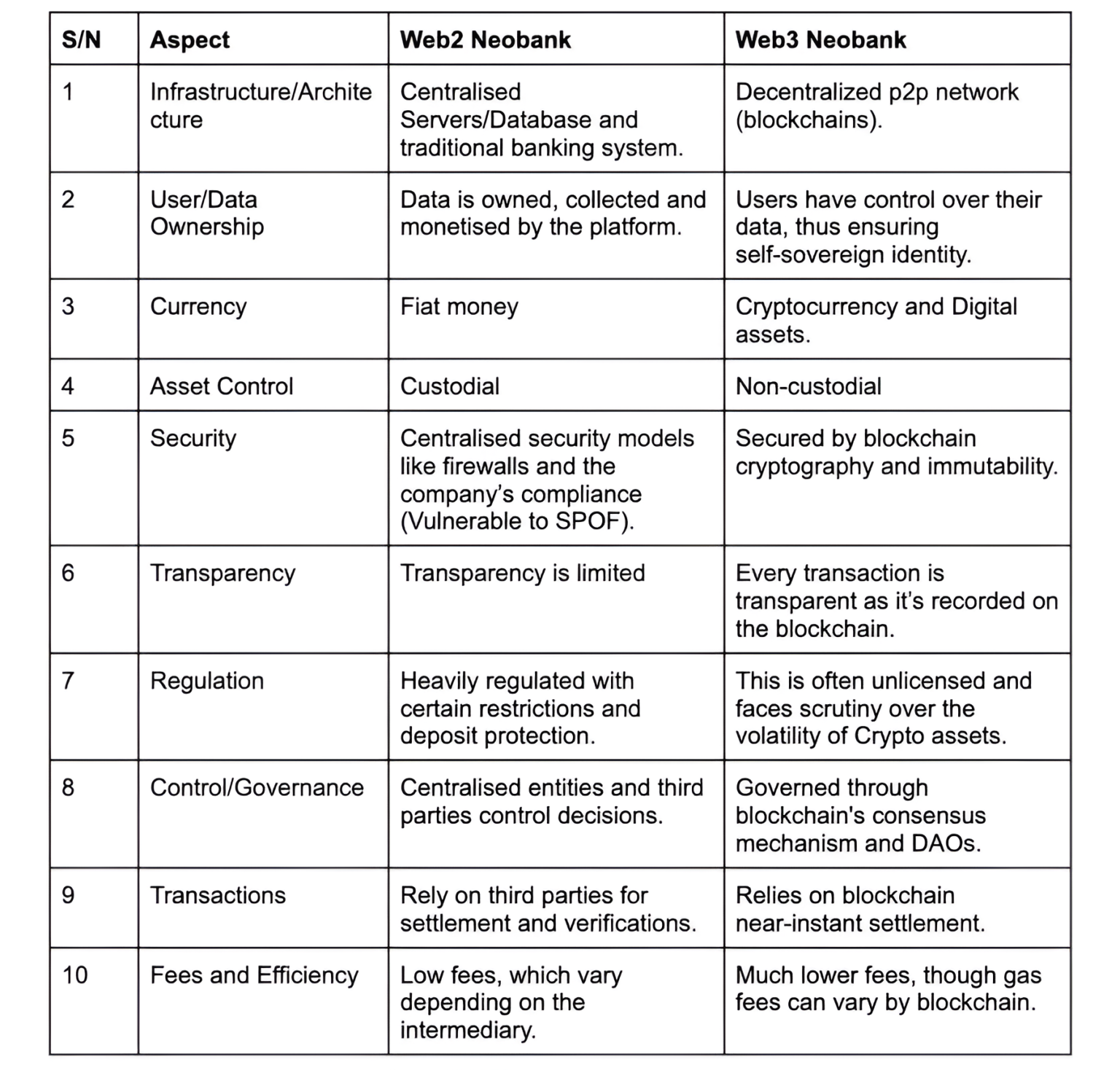

Neobanks in web2 and web3 are pretty similar, but the core ethos which distinguishes them is “Centralization and Decentralization”.

This has been a long-term battle fought over since the inception of Web3 as a new era of the internet, ushering in a new wave of internet pervasiveness, facilitating the essence of decentralization and ownership.

Neobanks in Web2 are heavily centralised and they rely on TradFi infrastructure, whereas Web3 neobanks leverage blockchain, offering users control and privacy.

Here’s a comparative table that provides a clear differentiator between these two:

We have seen that the proliferation of neobanks isn’t stopping soon and we already have 60+ neobank players in this landscape.

Amidst this noise, there hasn’t been a better way to filter it in this landscape than to group it into a Tier list by usage and in real time.

DeFI Warhol, a neobank enthusiast, created a great tier list ranking these neobanks by function and @ether_fi, @gnosispay, @UR_global and @Thorwallet stood out as key leaders.

Route2FI, one of the best CT writers and a DeFi enthusiast, also dug down the rabbit hole on neobanks and created a comparative table ranking etherfi as the key leader, whilst featuring gnosis, metamask, KAST and Crypto.com as well.

In the CT books of reckoning, Scroll is another ghost town L2, but I have always had this intuition of countertrading CT sentiments and 90% of the time it had always worked in my favour.

This is not me shilling Scroll or USX, but looking for an opportunity where others aren’t looking and I have never seen where one is wealthy doing what everyone else is doing.

What arouse my interest in USX and also made me feature them in this article is as a result of USX entirely reinventing the wheels on the Neobank landscape and doing what no one is doing.

They are building the first neobank dollar “USX” a spendable stablecoin which is private (ZK-powered) and gasless, which is estimate to earn 15% APY when you stake it.

This might be the project that will resuscitate the entire scroll ecosystem and being built by the Scroll team and exploring partnership with the @ether_fi for spendability and card.

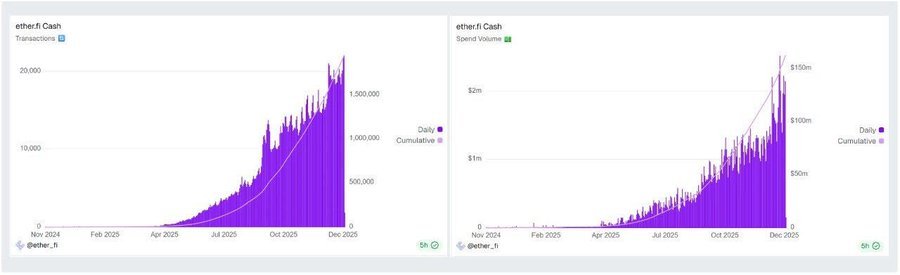

Etherfi cash is one of the leading neobank and has processed over $150M in total spend volume and has processed over 1.8M txns cumulatively.

I’m currently betting on the future of USX, driven by its initiative to shift the neobank sector to a new paradigm.

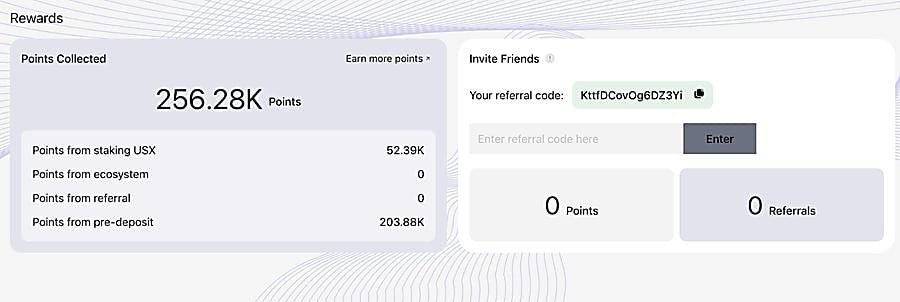

USX points program has been live for a while and its pre-deposit was the easiest chance to accumulate points.

If you’ve read up until this point, congrats, here’s my ref for you to use

https://www.usx.capital/pre-deposit?ref=KttfDCovOg6DZ3Yi

IMO, this is still undervalued considering the potential upside ahead if the scroll team executes this perfectly to make up for their poor airdrop distribution and it’s no coincidence they also started a points program for this.

As they say, fools rush in where angels fear to tread, but sometimes you have to play the role of a fool to fool the fool who thinks they’re fooling you.

Navigating the Regulatory Frontier: Compliance as a Catalyst

The proliferation of Web3 neobanks, fueled by advancements in DeFi and blockchain technology, has reached a critical inflection point where mass market and institutional adoption hinge entirely on regulatory clarity.

Compliance must be viewed not merely as a regulatory impediment inherited from traditional finance (TradFi), but as the essential infrastructure required for mainstream viability.

While Web3 neobanks frequently list Compliance and Identity tools as a core benefit, leveraging capabilities such as AI-powered Know Your Customer (KYC) and Anti-Money Laundering (AML) checks for enhanced operational efficiency

The sector simultaneously carries the risk profile of being often unlicensed and of facing scrutiny over asset volatility.

This gap between technical capability and legal standing presents a critical strategic challenge. Web3 projects must transition from possessing the technical capacity for compliance to achieving formalized institutional legitimacy through securing official charters and licenses.

This strategic pivot transforms the technology from a feature set into a foundational layer of trust that enables seamless operation between digital assets and fiat rails.

The failure to make this shift limits market access and prevents the sector from achieving the scale of integration necessary for explosive growth.

A fundamental clash exists between the core ethos of Web3 neobanking, characterized by decentralization, self-custody, and governance via Decentralized Autonomous Organizations (DAOs) and the global regulatory demand for transparent, centralized accountability.

Regulators require a single, identifiable entity responsible for mitigating financial crime risks.

The Financial Action Task Force (FATF), the global standard setter for anti-money laundering and counter-terrorist financing (AML/CFT), has issued binding standards that directly address this friction.

The FATF views virtual assets, especially those operating outside established oversight, as highly vulnerable to criminal exploitation.

Consequently, the global guidelines require Virtual Asset Service Providers (VASPs), a category that encompasses many Web3 neobank operations, to implement the same preventive measures as traditional financial institutions.

These obligations include comprehensive Customer Due Diligence (CDD), mandatory record keeping, and timely Suspicious Transaction Reporting (STR).

This VASP imposition structurally necessitates the identification of a centralized, liable entity capable of executing these duties, directly challenging the anonymous and disintermediated nature of true DAOs.

When projects resist this mandate, they are often perceived as risky and denied access to critical banking infrastructure and fiat services.

This creates a severe barrier to achieving the seamless Crypto <> Fiat integration that Web3 neobanks promise. Compounding the issue is the continuing regulatory ambiguity regarding what constitutes sufficient decentralization, which stalls the integration process and limits market opportunities for many protocols.

The fragmentation of global regulatory approaches, as seen between the European Union, the United States, and Asia, further incentivizes regulatory arbitrage. However, this approach severely limits neobanks’ ability to scale and attract highly regulated institutional capital.

The friction between decentralised governance and centralised compliance is not abstract; it creates tangible risk for decentralised market infrastructure projects, particularly those related to stablecoins, such as the proposed USX project on the Scroll L2 network.

In the United States, regulatory clarity for payment stablecoins has emerged through the enactment of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act).

This legislation aims to set regulatory boundaries for stablecoin issuance, promote consumer protection, and ensure the dollar’s global competitiveness.

The GENIUS Act strictly mandates that payment stablecoins be issued only by permitted payment stablecoin issuers, such as subsidiaries of insured depository institutions or licensed nonbank entities.

Crucially, these licensed issuers must adhere to orthodox financial requirements, including maintaining full, one-to-one backing in highly liquid, segregated reserves, such as short-term U.S. government-issued assets.

Issuers are also subject to strict capital, liquidity, and operational risk management requirements.

For decentralized stablecoin projects like USX, this framework presents a significant hurdle. Unless the protocol can designate a licensed, capitalized entity legally obligated to maintain reserves and facilitate redemption, the stablecoin faces substantial regulatory risk.

This necessity forces decentralized infrastructure to integrate a centralized compliance wrapper. Projects that attempt to operate without this legal wrapper confirm the Risky Bet Play inherent in pioneering DeFi infrastructure that seeks mass adoption without addressing a pre-emptive compliance strategy.

Compliance serves as the primary de-risking function for Web3 neobanks, helping them transition from a volatile, high-risk sector into credible financial partners capable of attracting institutional liquidity and users.

Institutional investors, including hedge funds, family offices, and traditional financial entities, require vetted projects with clear governance and transparent compliance before committing substantial capital.

Effective crypto-related compliance is recognized as crucial for the overall stability and trustworthiness of the digital asset industry.

The ability of neobanks to integrate sophisticated blockchain analytics and real-time monitoring tools allows them to demonstrate compliance with global AML/CFT mandates, thereby securing the stability and safety that retail investors and institutions demand.

By embracing regulatory standards, Web3 neobanks gain the requisite trust to offer white-label crypto solutions to existing banks and businesses, accelerating adoption and expanding liquidity across the ecosystem.

Gnosis Pay exemplifies the successful Regulated Hybrid Model, demonstrating how Web3 principles can be reconciled with stringent TradFi requirements.

Gnosis Pay is architected as a decentralized payment network that upholds the Web3 ethos of non-custody, with user funds always secured within self-custodial Gnosis Safe wallets.

To bridge this non-custodial environment with the globally regulated financial system, Gnosis Pay pursues a strategic compliance approach focused on the integration point.

The Gnosis Card, for instance, is issued by third-party licensed Electronic Money Institutions (EMIs), initially targeting the regulated markets of the UK and Europe.

This regulated partnership is the crucial bridge, allowing the decentralized protocol access to the global Visa payment network.

Functional compliance is achieved through integrating specialized partners. Sumsub handles identity verification (KYC), and Elliptic provides real-time transaction monitoring (KYT/AML).

This KYC requirement is justified because the service connects to traditional banking systems, enabling SEPA transfers via Monerium for easy euro on- and off-ramps.

The operational strategy centralizes regulatory liability at the fiat entry/exit points through licensed partners, while the core digital asset custody remains decentralized and self-sovereign.

This approach demonstrates that adherence to global AML/CFT standards is achievable without sacrificing the non-custodial benefits that are fundamental to the Web3 value proposition.

The case of the crypto lending platform Nexo provides a stark cautionary example regarding the necessity of proactive, explicit licensing across all operational jurisdictions.

Nexo, a globally recognized platform, faced a large-scale investigation by Bulgarian authorities into alleged illegal activities, including money laundering, tax crimes, and the critical charge of providing banking services without the necessary license.

This regulatory uncertainty and legal challenge led to significant instability, including capital flight and market polarization within the local crypto community.

The incident underscored that simply having a presence or developing compliance tools is insufficient; comprehensive legal authorization, such as a proper banking charter or specialized license (like an e-money license), is non-negotiable for large-scale Web3 neobanks that operate with bank-like functions (lending, custody, interest yields).

The instability resulting from regulatory ambiguity demonstrates that proactive adherence is essential for maintaining operational continuity and the institutional trust required for long-term survival.

The synthesis of Web3’s structural demands and the non-negotiable requirements of the global financial system gives rise to the Hybrid Neobank Model. This model directly addresses the challenges posed by decentralized anonymity by integrating specific compliance layers mandated by international regulators, thereby enabling institutional engagement.

Web3 promised us the future of decentralization and with blockchain technology, the vision is becoming clearer and we will get to that point in the future where blockchain use cases will be beyond finance. I expect to see that in other sectors like Aviation, the automotive industry, the medical industry, and the agro-allied sector etc.

see something, say something. building @moduverseco

https://t.co/p896uWGWub

Genome Protocol Rug Pull: Explained

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Genome Protocol Rug Pull: Explained

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio