Loading Search...

Ethereum Foundation selling ETH is nothing new. Here is why EF sells, where the money goes, and how staking could end these sales for good.

Author: Tanishq Bodh

The Ethereum Foundation selling ETH is nothing new, but it never stops generating outrage. Every few weeks, the same headline hits Crypto X. Every time, the same cycle plays out. Accusations of dumping on retail, top-signal memes, and a fresh wave of doubt about whether the people building Ethereum even believe in it anymore.

On March 14, 2026, the Ethereum Foundation sold 5,000 ETH to BitMine, an institutional entity tied to Fundstrat strategist Tom Lee, through an over-the-counter deal at an average price of $2,042.96. That is roughly $10.22 million in proceeds. ETH barely moved.

But the reaction was predictable. One camp called it smart money exiting. Another questioned where the money even goes when lead EF developers reportedly earn $8,000 a month. A third just wanted to know why the Foundation could not at least sell at market price.

Most of this frustration comes from a gap in understanding. The average crypto holder sees the Ethereum Foundation selling ETH on-chain and fills in the blanks with whatever narrative fits their mood. The actual mechanics behind why the Foundation sells, how it operates, and what these sales fund rarely make it into the conversation.

This piece breaks that down.

The Ethereum Foundation is a non-profit organization based in Switzerland. It does not control Ethereum, it does not govern the protocol. It does not run the network.

What it does is fund the ecosystem. The Foundation supports protocol research, core client development, developer tooling, ecosystem grants, community programs, and events like Devcon and Devconnect. It also funds zero-knowledge cryptography research, Layer 2 development, and applied cryptographic work that keeps Ethereum competitive at the infrastructure level.

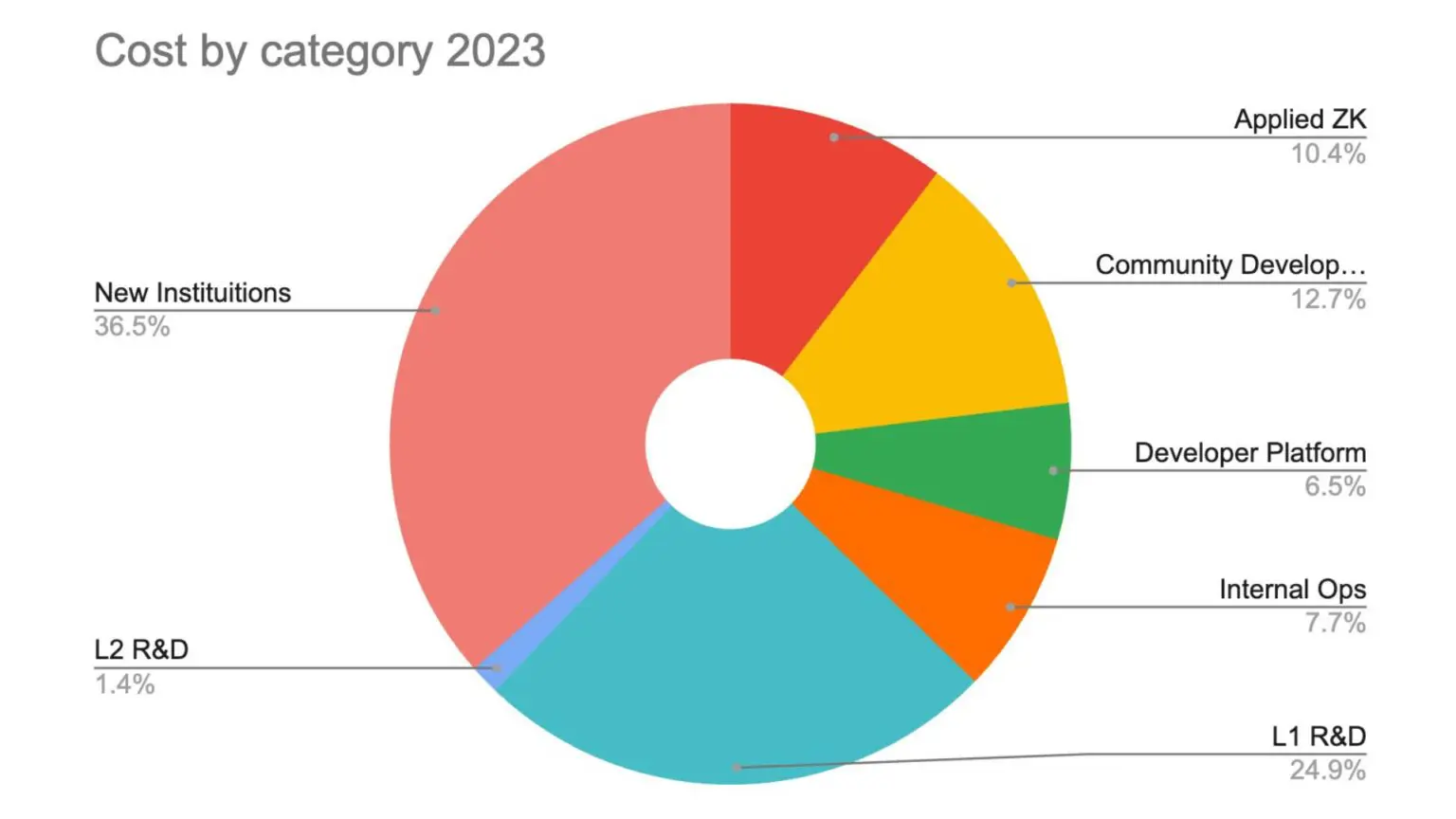

In 2023, the Foundation spent $134.9 million. In 2022, that number was $105.4 million. The annual budget hovers around $100 million, a figure confirmed by Ethereum researcher Justin Drake in a September 2024 Reddit AMA and later verified by Vitalik Buterin himself.

The 2023 spending breakdown looked roughly like this. New Institutions took the largest share at 36.5 percent of the budget, which includes external grants to organizations like L2Beat, 0xPARC Foundation, and Nomic Foundation. Layer 1 research and development was the second-largest at 24.9 percent, covering internal teams and external grants to projects like Geth, Solidity, and Ethereum’s Robust Incentives Group. Community development accounted for 12.7 percent. Applied zero-knowledge work captured 10.4 percent, followed by internal operations at 7.7 percent, the developer platform at 6.5 percent, and Layer 2 research at 1.4 percent.

That is where your ETH goes when the Foundation sells.

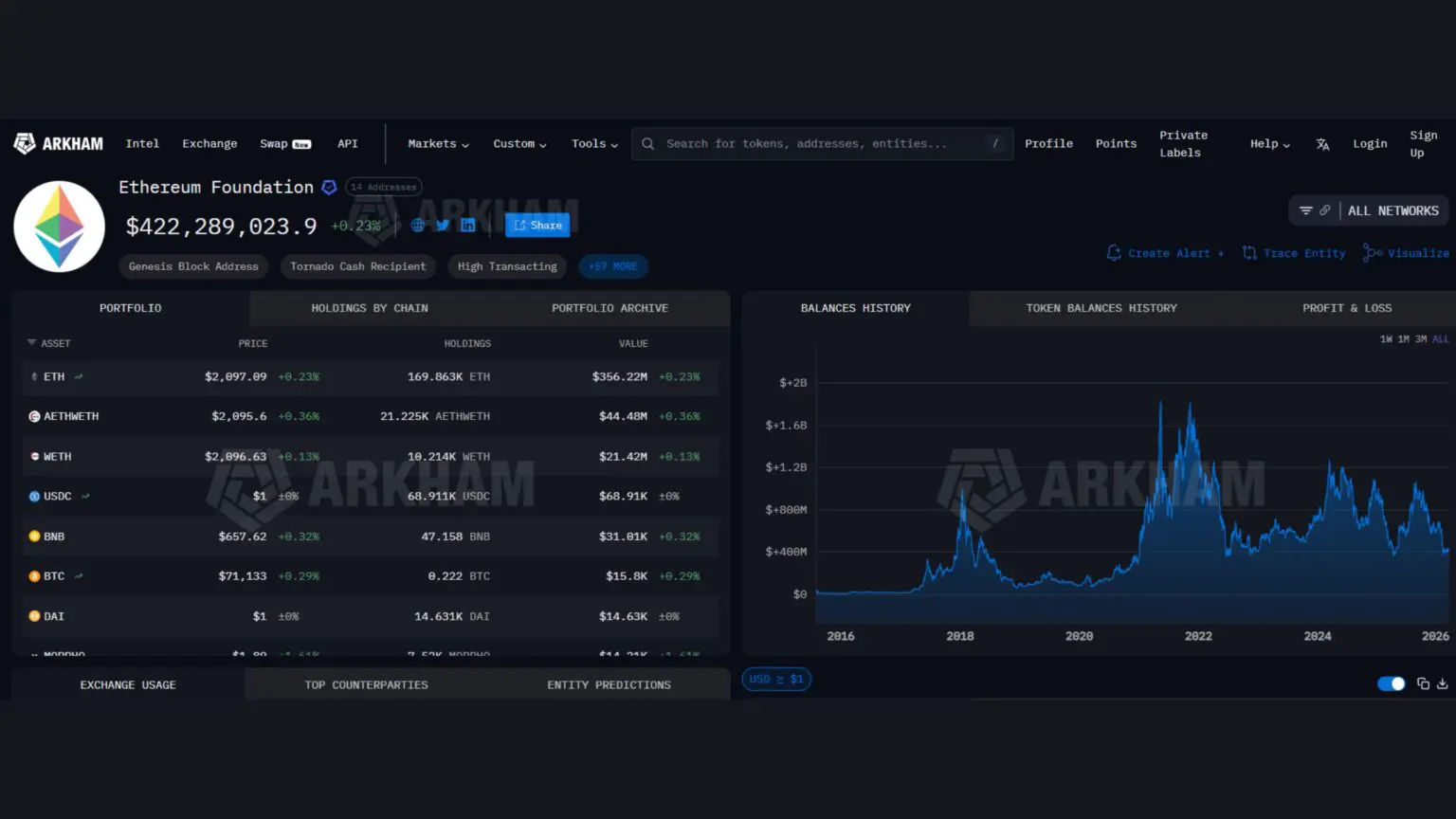

As of late 2024, the Ethereum Foundation’s total reserves stood at roughly $970 million. That was already down 39 percent from $1.6 billion reported in March 2022. Of that $970 million, about $788 million was in crypto, with 99.45 percent of that held in ETH. The remaining $181 million was in non-crypto holdings including fiat and traditional investments.

The Foundation operates on a budget strategy of spending approximately 15 percent of its remaining funds each year. By design, this means the Foundation gets smaller over time. That is intentional. The goal is not to be a permanent institution but to support Ethereum until the ecosystem can sustain itself through other funding mechanisms.

But here is the problem. You cannot pay salaries, rent office space, fund conference logistics, or distribute grants to developers in ETH alone. Many recipients, especially those in traditional jurisdictions, can only accept fiat currency. The Foundation needs dollars, euros, and Swiss francs to operate. The only way to get those is to sell ETH.

That is the fundamental reason behind the Ethereum Foundation selling ETH. It is not a lack of conviction. It is an operational necessity.

Not all EF sales happen the same way. The smaller, routine sales, usually 100 ETH batches, have historically gone through exchanges like Kraken. But the larger transactions, like the recent 5,000 ETH sale to BitMine or the 10,000 ETH sale to SharpLink Gaming in July 2025, are executed over-the-counter.

OTC deals happen off the public order book. A buyer and seller agree on a price privately, and the transaction settles without touching the open market. The advantage is simple: no slippage, no visible sell pressure, and no panic-inducing Lookonchain alert showing thousands of ETH moving to an exchange wallet.

When the Foundation sells 5,000 ETH on-market, that is a $10 million sell order hitting the book. Even on a liquid pair like ETH/USDT, that creates visible downward pressure and triggers algorithmic trading responses. OTC avoids all of that.

The buyers in these deals are also telling. BitMine is an institutional player accumulating ETH as a strategic treasury asset. SharpLink Gaming, the counterparty for the July 2025 sale, is a publicly listed company that bought 10,000 ETH at roughly $2,572 per coin. These are not speculators flipping a position. They are long-term holders absorbing supply that would otherwise hit the open market.

The narrative that the Ethereum Foundation selling ETH “always marks the top” has become crypto folklore. And like most folklore, it contains some truth and a lot of exaggeration.

Here is the actual record.

So does the Foundation sell the top? Sometimes. The May and November 2021 sales were remarkably well-timed, whether by skill, luck, or prudent risk management. But the December 2020 sale, where the Foundation moved 100,000 ETH before a 6x rally, completely undermines the idea that EF sales are a reliable bearish indicator.

CoinGecko research found that less than half, around 47.6 percent, of EF sell-offs resulted in a price decline within seven days. In more cases than not, the price actually rose after a Foundation sale. The correlation between EF sales and price drops has been inconsistent, and broader macro forces like Federal Reserve policy, Bitcoin dominance cycles, and overall risk appetite play a far larger role in determining ETH’s direction.

The real takeaway is this: EF sales create short-term sentiment shocks, especially when they hit as large exchange transfers. But they do not drive the trend. They are noise, not signal.

Everything described above is changing.

In June 2025, the Ethereum Foundation announced a new treasury policy focused on actively deploying ETH rather than sitting on idle reserves. The centerpiece of this policy is staking.

On February 24, 2026, the Foundation began staking with an initial deposit of 2,016 ETH. The broader plan targets approximately 70,000 ETH to be staked over the coming months, representing roughly 38 percent of its liquid ETH holdings. At current prices around $2,000, that is approximately $140 million locked into validators.

At a staking yield of roughly 2.8 percent, 70,000 staked ETH would generate an estimated 1,900 to 2,200 ETH per year, or approximately $3.6 million annually at current prices. That does not cover the full $100 million annual budget, but it is a meaningful step toward reducing the frequency and size of treasury sales.

The infrastructure runs on open-source tools developed by Attestant, now operating under Bitwise Onchain Solutions. The setup uses Dirk for distributed key signing across multiple jurisdictions and Vouch for validator management across several client implementations. The Foundation is using minority clients and a mix of hosted and self-managed hardware spread across several countries.

Beyond staking, the updated treasury policy also allows selective participation in vetted DeFi protocols and exploration of tokenized real-world assets, including U.S. Treasuries, as a way to stabilize fiat reserves and diversify risk.

The strategic logic is straightforward. The Ethereum Foundation selling ETH depletes the treasury permanently. Staking creates ongoing yield while the principal remains intact. If yield can cover even a portion of operational costs, the Foundation’s runway extends significantly and the sell pressure everyone complains about gets reduced structurally rather than cosmetically.

The Ethereum Foundation selling ETH is defensible on its own merits. What is less defensible is how poorly it has communicated about it.

For over two years, the Ethereum Foundation published no financial report. Community members learned about major ETH movements from third-party on-chain trackers like Lookonchain and SpotOnChain, not from the Foundation itself. When 35,000 ETH moved to Kraken in August 2024, the community found out from a Twitter bot.

That is a governance and communications failure. As one community member put it, “How hard is it to release a quarterly report with financials and basic updates? Expenses, expected upcoming sales, how and where the money is being spent, team size and distribution.”

The November 2024 report helped, but it came after sustained public pressure. The Foundation also introduced a conflict-of-interest policy after two prominent researchers, Justin Drake and Dankrad Feist, came under scrutiny for ties to the Eigenlayer protocol, which had accumulated over $14 billion in user deposits.

The combination of opaque finances, perceived top-selling, and internal governance questions erodes trust, even when the underlying treasury management is rational. Other major foundations like Polkadot’s Web3 Foundation face similar scrutiny but at least publish regular transparent spending reports. The Ethereum Foundation, stewarding the second-largest crypto ecosystem in the world, should be held to at least the same standard.

The Ethereum Foundation is in a transitional period. The old model, hold ETH, sell when you need cash, repeat, is being replaced by something more sustainable. But the transition is not complete.

The staking program generates meaningful yield but not enough to eliminate sales entirely. At $3.6 million in annual staking income against a $100 million annual budget, the Foundation still needs to liquidate ETH periodically. The March 2026 OTC sale to BitMine is a bridge, covering immediate cash needs while the staking model ramps up.

Several things worth watching in the months ahead. The Glamsterdam upgrade is expected in the first half of 2026, followed by the Hegota upgrade later in the year. Both target scalability improvements that could increase network activity and, by extension, staking rewards. The Foundation’s quarterly transparency reports will show progress toward the 70,000 ETH staking target. If staking yields fall below expectations or operational costs rise, additional treasury sales are inevitable.

But the direction is clear. The Ethereum Foundation is moving from a model that creates recurring sell pressure and erodes community trust toward one that generates protocol-native income and keeps the treasury intact. It is not there yet. But the structural pieces are in place.

The next time you see “Ethereum Foundation selling ETH” on your timeline, you will know what is actually happening. And you will know that the real question is not why they sell, but whether the new model can make these sales a thing of the past.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.