Loading Search...

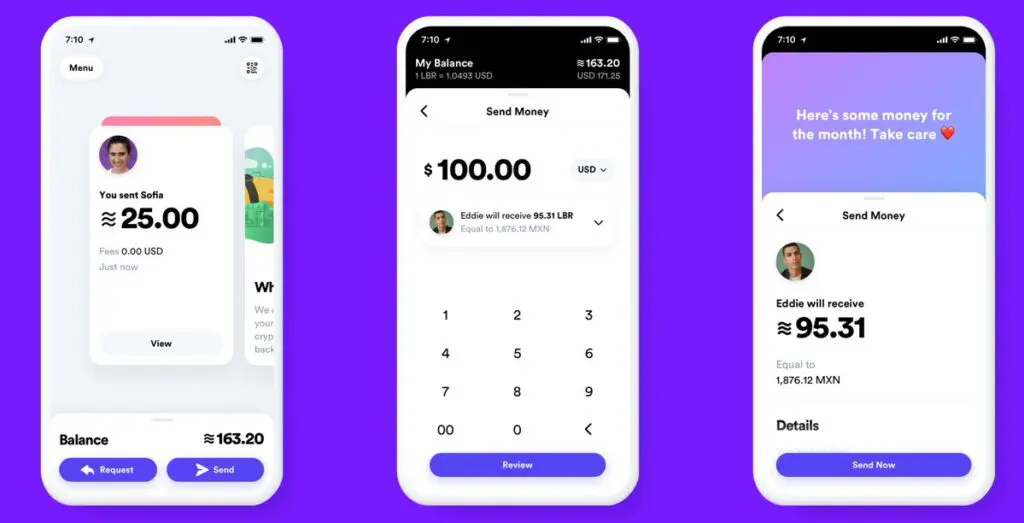

Meta aims to onboard 3.6 billion users onto Web3 with its stablecoin, crypto and wallet solutions, expanding accessibility.

Author: Arushi Garg

In 2019, Mark Zuckerberg revealed Facebook’s plan to launch a global digital currency. It was not just a payment tool or wallet but a fully-fledged currency. Backed by a basket of assets and governed by the Libra Association with 28 corporate partners, including Visa, Mastercard, PayPal, Uber, and Stripe, the project aimed to provide banking access to the unbanked and enable near-zero-cost cross-border money transfers. Today, Meta is exploring innovations in stablecoin, crypto, and wallet technologies to bring Web3 to billions of users.

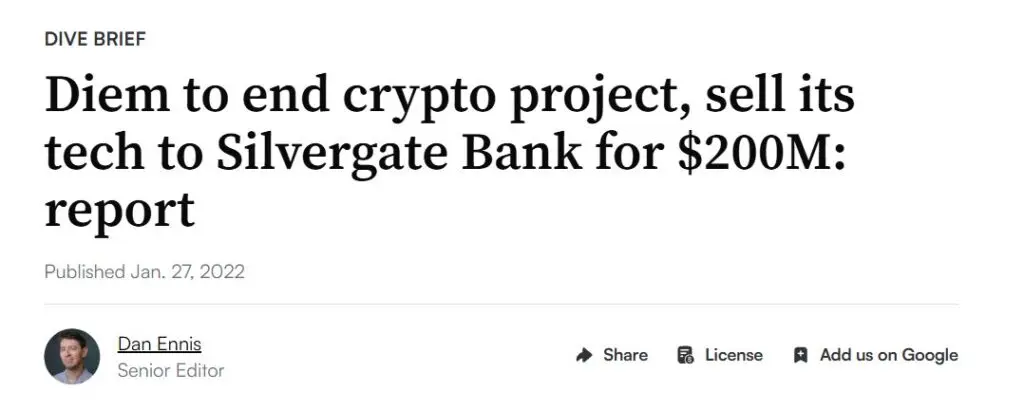

The announcement sparked immediate pushback. Within months, Visa, Mastercard, PayPal, Stripe, and eBay exited the Libra Association. U.S. Congress called Zuckerberg to testify, and the European Central Bank warned it threatened monetary sovereignty. Former President Trump demanded it be shut down, saying “it’s called the U.S. dollar.” The project’s team later renamed and scaled it back, eventually selling its assets to Silvergate Bank for about $200 million in January 2022. Silvergate later collapsed.

Meta’s next move is different. According to three sources, the company has issued a Request for Proposal to build stablecoin payment infrastructure across Facebook, Instagram, and WhatsApp. This is not a new coin or blockchain. It is integration of existing dollar-pegged stablecoins, managed by an external partner, quietly running on platforms used by 3.6 billion people.

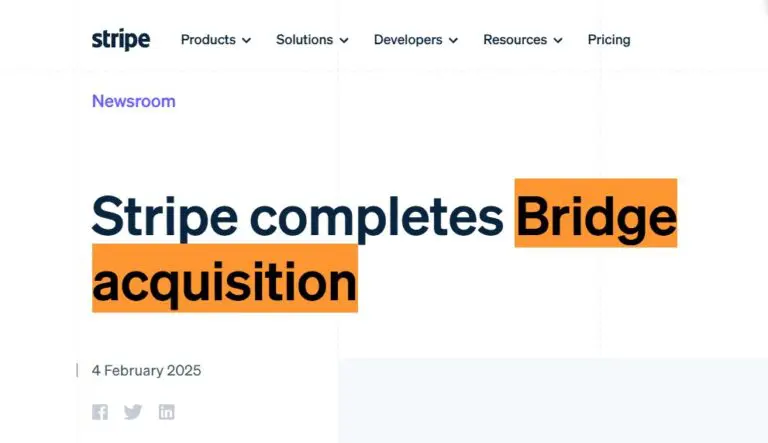

Stripe is the likely partner, with its stablecoin division Bridge expected to serve as the operational backbone. The pilot rollout is targeted for the second half of 2026, leveraging relationships that have been developing for over a year.

Stripe acquired Bridge, a stablecoin infrastructure specialist, in October 2024 for $1.1 billion, marking the largest acquisition in Stripe’s history. The deal closed in February 2025. Bridge already powers custom stablecoins for crypto products such as Phantom’s CASH and MetaMask’s mUSD through its Open Issuance platform.

On February 17, 2026, Bridge received conditional approval from the Office of the Comptroller of the Currency to operate as a national trust bank. This allows Bridge to issue stablecoins, custody digital assets, and manage reserves under federal oversight. It is one of the most significant regulatory milestones for a stablecoin infrastructure company in U.S. history.

Stripe CEO Patrick Collison joined the Meta board of directors in April 2025, a strategic move that aligns the companies for infrastructure collaboration. Stripe processed $1.9 trillion in total payment volume in 2025, roughly 1.6 percent of global GDP. Bridge’s stablecoin, crypto, and wallet transaction volume more than quadrupled in 2025 as adoption decoupled from crypto market cycles and began functioning like traditional payments infrastructure.

This is not a crypto startup pitching social media. It is globally credible payments infrastructure, federally approved, operating at scale, and positioned just one board seat away from Meta.

The regulatory environment has also changed. On July 18, 2025, President Trump signed the GENIUS Act into law, providing clear rules for stablecoin issuance, reserves, and oversight. The bipartisan legislation passed the Senate 68 to 30 and the House 308 to 122, creating a legal framework that did not exist during Libra in 2019.

The GENIUS Act establishes the first federal legal framework for payment stablecoins in U.S. history. Issuers must hold reserves at a one-to-one ratio. Eligible reserves include U.S. dollars, bank deposits, short-term Treasuries, and money market funds. Payment stablecoins are explicitly classified as neither securities nor commodities, removing them from SEC and CFTC oversight. The law creates a clear path for companies to issue and operate dollar-pegged tokens under federal supervision.

This legal foundation did not exist in 2019. Meta is not returning to the same battlefield. The battlefield has been rebuilt.

The 2026 plan is very different from the 2019 Libra project. Libra was Meta’s attempt to become a financial institution. It aimed to build the coin, govern it, back it with a basket of global currencies, control the infrastructure, and own the payment rails. Central banks worldwide saw it as a direct play for monetary power.

The 2026 plan is Meta’s attempt to add a payment feature to its apps. Meta will not build the coin, govern the network or hold the reserves. Instead, a third party will handle everything. That third party will be federally chartered and regulated. Meta will keep its hands off issuance and governance entirely. The goal is simple: let 3.6 billion users send money to each other, pay creators, and settle commerce inside apps they already use every day.

The leadership of this initiative reportedly sits with Ginger Baker, a Meta executive with prior experience at Ripple and connections to the Stellar Development Foundation. She brings deep knowledge of compliance and stablecoin operations.

According to sources, the architecture is simple: a licensed partner manages issuance, compliance, and settlement while Meta controls distribution. This clear division of responsibility is intentional and strategically smart.

The use cases Meta is targeting may seem modest at first. Cross-border remittances, peer-to-peer transfers, creator payouts, and social commerce are all in focus. The goal is to reduce friction in in-app payments, such as helping Instagram creators in Brazil receive payments from followers in Germany without losing 7 percent to wire fees. By leveraging the Meta stablecoin, crypto, and wallet solutions at scale across 3.6 billion monthly active users, the potential impact becomes much more significant.

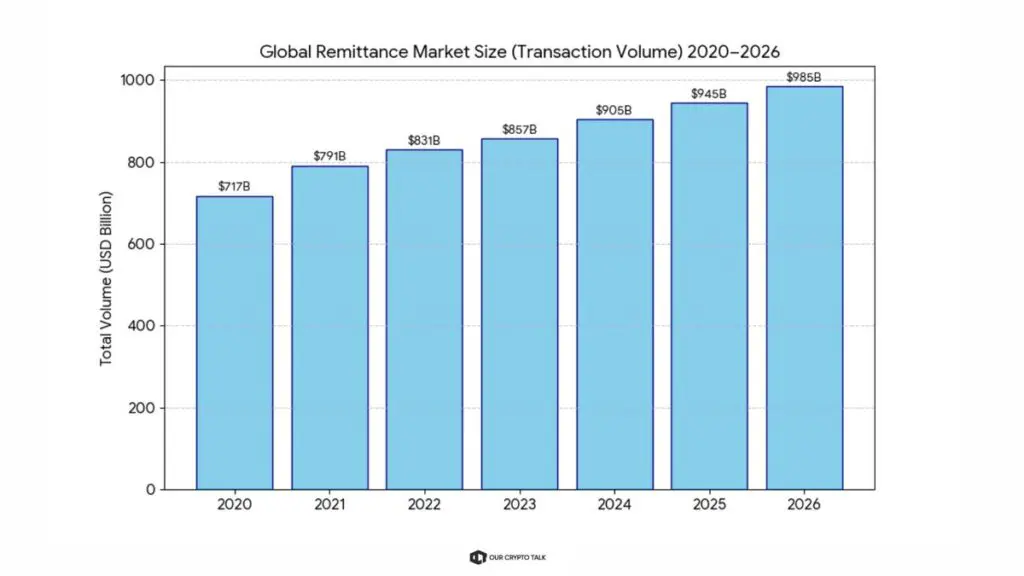

Remittances are a $950 billion annual market. Traditional international transfers charge 6 to 8 percent in fees. Stablecoin-based transfers can cost only a fraction of a cent. If Meta captures even a small share of that flow through WhatsApp, which dominates Latin America, Africa, and South Asia, it could disrupt traditional money transfer operators significantly.

Creator payouts follow a similar logic. Meta distributes billions each year to Instagram and Facebook creators. Using stablecoins, crypto, and wallet solutions instead of SWIFT or card networks reduces friction, speeds up payments, and removes intermediary fees. This saves real money and strengthens Meta’s creator economy compared to competitors.

Competition is also a factor. Telegram already runs TON Pay for 1.1 billion users. X Money is in closed beta with potential stablecoin support. Meta, with three apps and 3.6 billion users, has unmatched reach. Native stablecoin, crypto, and wallet payments across WhatsApp, Instagram, and Facebook could allow Meta to lead the “super app” race before X or Telegram fully enter the market.

The AI dimension is often overlooked. Meta is building AI agents that can browse products, manage shopping, and eventually execute purchases autonomously. For these agents to work, they need payment rails that operate programmatically, instantly, and at minimal cost. Credit cards require human action. Bank transfers need manual initiation. Stablecoins allow software agents to send payments in milliseconds at almost zero cost.

In the roadmap of Meta, stablecoin, crypto, and wallet solutions are not just a payments feature for users. They will serve as settlement infrastructure for autonomous AI commerce. The AI agent can compare products, choose the best option, and settle the transaction on-chain instantly, without any human entering credit card information. This is a far bigger vision than cheap remittances and explains why Meta is building financial infrastructure now, ahead of the full AI agent ecosystem.

The stablecoin market has grown dramatically since 2019. When Libra was announced, total stablecoins were $3 to $5 billion. Today the market is $308 billion, with Tether (USDT) at $187 billion and Circle’s USDC second largest. In 2025, the market expanded $46 billion in a single quarter, the largest quarterly growth ever. Bridge’s transaction volume quadrupled in 2025. Stablecoin adoption is now decoupled from crypto cycles, acting like core financial infrastructure rather than a speculative asset. The Meta stablecoin, crypto, and wallet initiatives are entering a real market, not just a crypto experiment.

This plan is not guaranteed. Regulatory implementation rules under the GENIUS Act are expected by January 2027, leaving some uncertainty. Meta’s past reputation issues, including Cambridge Analytica, may trigger scrutiny. The “at arm’s length” model means Meta’s payment feature depends on third-party performance; operational failures at Stripe or Bridge could hurt Meta’s reputation. Plans are still conditional, non-public, and dependent on integration success.

In 2017, a Facebook engineer named Morgan Beller began quietly researching blockchain, setting the foundation for what eventually became Libra and now the 2026 stablecoin initiative.

In 2019, Zuckerberg tried to launch Libra and faced universal regulatory pushback. By 2022, Meta sold the project and shut down the wallet. In 2023, the company discontinued its NFT feature due to limited user interest. By 2025, lawmakers replaced the regulatory framework that blocked Libra with a law welcoming stablecoins.

In 2026, Meta could return with a quiet integration of existing stablecoin infrastructure, managed by a federally chartered partner and distributed across 3.6 billion users. The plan targets the $950 billion remittance market and the emerging AI commerce economy.

The ambition remains the same but the approach is different. Before, Meta tried to become the bank. Now, it wants to be the app that the bank runs through. This version is more likely to succeed.

Disclaimer: Not financial advice. This summary is based on reports from CoinDesk and other sources citing anonymous insiders. Plans are unconfirmed. Stablecoins and crypto carry regulatory and market risks. DYOR.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.