Crypto Buybacks have recently turned into a major catalyst across markets, especially for token price action, and we’re seeing it everywhere. For example, HyperliquidX routes 97% of platform fees into $HYPE buybacks and has already crossed over $1B in cumulative purchases, which keeps a steady bid in the book.

In contrast, Pumpdotfun spent around $44M repurchasing $PUMP, including a $12M single-day buyback last week, yet the price gains faded quickly after the initial pop. Meanwhile, 0xfluid’s community is actively debating a dynamic model that can allocate up to 100% of revenue to buybacks when FDV is low, and the Arbitrum DAO is considering an institutional ARB buyback funded through bond issuance.

We keep using the same word “buyback” but the outcomes vary widely. This alone tells us something important: crypto buybacks can act as support, resistance, or even a source of drawdown, depending entirely on how they’re designed and executed.

So the real question is:

Why do some crypto buybacks pump a token, while others barely hold the price up?

The Mechanics Behind Crypto Buybacks

Buybacks are not magic they are flows, and flows interact with supply, liquidity, and trader behavior. Four core mechanics shape the outcome of a buyback program:

1. Supply Balance: A buyback only reduces circulating supply if the amount purchased exceeds emissions, unlocks, or vested allocations. If outflow < inflow, the net effect is dilution.

2. Order Flow: Buybacks provide consistent buy-side order flow on the book. But if existing holders are selling faster than the buyback accumulates, price support disappears. It’s simply the balance of flows.

3. Liquidity Depth: Deep liquidity absorbs buyback size in a way that creates sustainable levels. But in thin liquidity, the same amount of spend creates temporary spikes that retrace once sellers return. Liquidity determines whether the buyback creates a floor or just a wick.

4. Execution and Funding: Execution matters. Predictable, onchain buyback schedules get front-run. Randomized or private execution gives the buyback more staying power.

5. Funding matters too: Programs tied to recurring revenue can run indefinitely; programs funded from a finite treasury last only as long as reserves remain.

How and Why Buybacks Can Fail

Many projects announce buybacks and still see price bleed. Understanding the failure modes is just as important as understanding the wins.

Mechanically, crypto buybacks fail when the program:

Cannot offset net supply

Signals execution and invites traders to fade it

Operates in liquidity too thin to retain price impact

Revenue peaks during hype cycles and collapses in downturns

Treasuries get drained too quickly

Buys occur at or above fair value, creating resistance instead of support

Often, buybacks become bullish headlines without real impact cosmetic, not structural.

The Buyback Model Map

Not all buybacks follow the same logic. Projects adopt different models to decide when and how to buy, and these models directly determine the outcome. Here are the most common ones used in crypto today:

1. Constant Revenue Share:

A fixed percentage of revenue gets allocated to buybacks every epoch.

Hyperliquid routes 97% of fees directly into $HYPE buys.

This is simple and predictable, but it doesn’t adapt to stress if emissions spike or liquidity thins, the program keeps buying at the same pace, regardless of effectiveness.

2. TWAP Triggers

Programs activate buybacks when price trades below a 30-day TWAP, and pause when above.

This reduces frontrunning and smooths execution, but can lag in fast-moving markets and sometimes just pays for natural reversion.

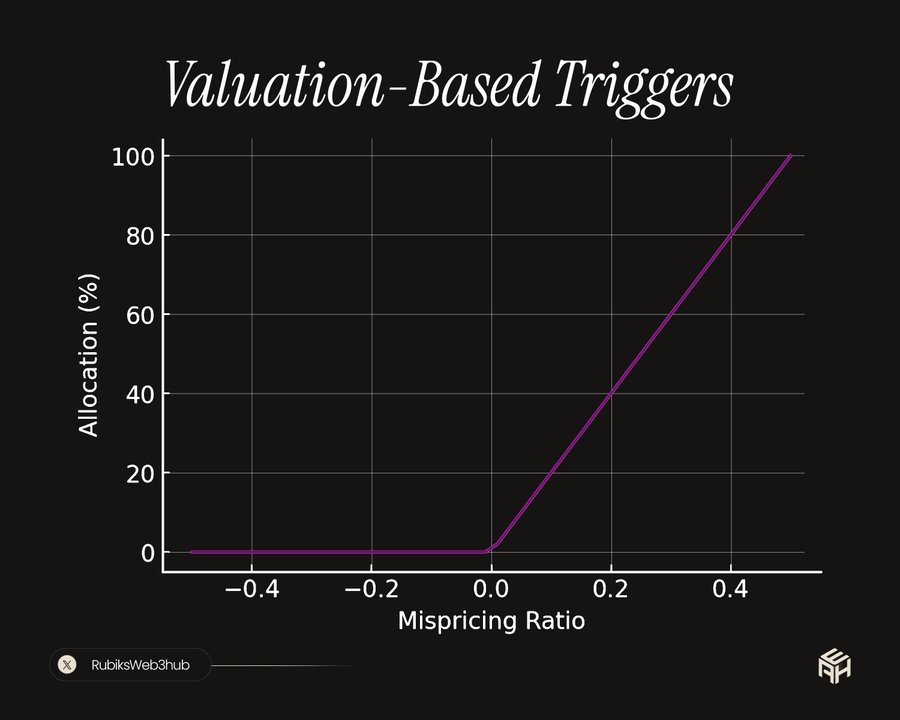

If actual FDV < fair value, the buyback allocation increases sometimes scaling up to 100% of revenue.

Done right, this is countercyclical. Done wrong, it gets gamed by restricted float or unrealistic multipliers.

0xfluid‘s community has been debating exactly this. A dynamic model that can push buybacks up to 100% of revenue when FDV is low. If it is done right, this design is countercyclical. If done wrong, it can be gamed by a restricted float or unrealistic multipliers.

Tweet not available.

Below is an opinionated post on Fluid proposed methods by 0xnoveleader:

Tweet not available.

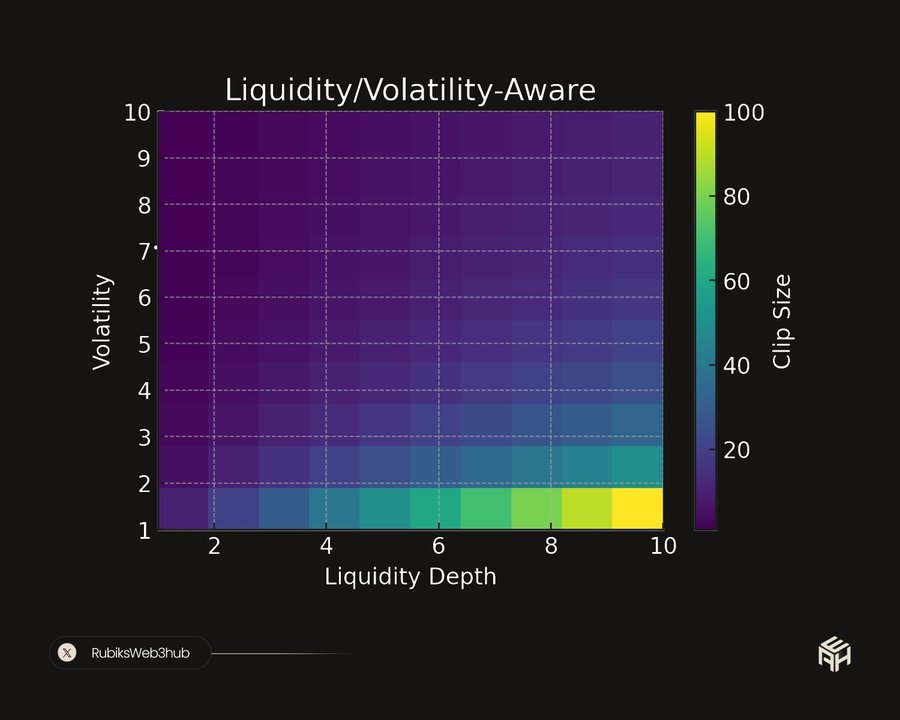

4. Liquidity or Volatility-Aware Models

Here the program adjusts clip size and frequency based on real-time depth or volatility.

Buy more when liquidity is deep, buy less when shallow.

Efficient but data-heavy.

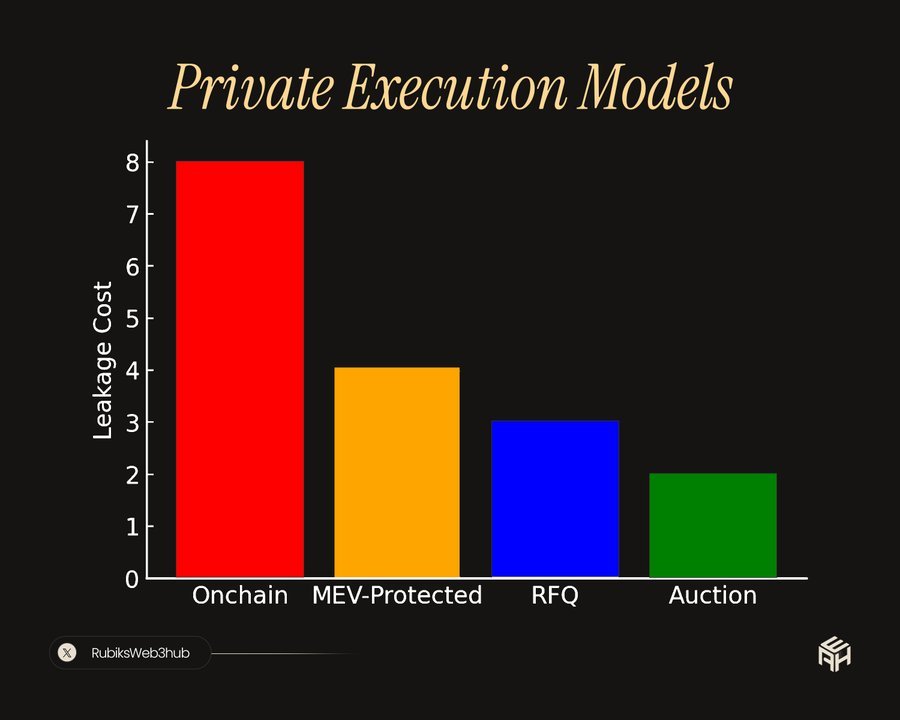

5. Private Execution Models

Execution style changes outcomes even with identical budgets.

Public onchain orders invite frontrunning; private RFQs, sealed auctions, or MEV-protected relays stretch the buyback further.

Arbitrum DAO explored using institutional-grade execution to minimize slippage and waste.

Artificial Demand vs Real Demand

Not every buyback delivers the same kind of demand. Some create temporary support; others build lasting floors.

Artificial demand exists only while the program is active:

Price rises during the buyback and fades immediately after

Charts show abrupt wicks

Wash traders and opportunists cycle through

Real demand is fundamentally different:

Holders keep holding due to genuine perceived value

Buybacks reinforce long-term conviction

Demand persists even if buyback activity slows

Tests to distinguish the two:

If price and volume collapse when the program stops -> artificial

If wallets bought during the program churn within 30–90 days -> artificial

If protocol usage and revenue grow with price -> real

If revenue follows the pump instead of leading it -> hype, not fundamentals

This distinction matters because cosmetic buybacks create noise; real buybacks create floors that last across cycles.

The Conditions for a Successful Buyback

Some buybacks create durable floors; others are purely cosmetic. The difference usually comes down to design and discipline. Strong buyback frameworks share these traits:

Countercyclical Triggers: Spend more when valuations drop capital-efficient and credible.

Liquidity-Aware Execution: Order sizes remain small relative to depth and are spread across time, avoiding signal leakage.

Blackout Discipline: Pausing buybacks around unlocks or major announcements prevents optics of manipulation.

Transparent Inputs: Publishing formulas and input data increases trust and reduces skepticism.

Budget Caps and Taper: Hard caps per week/quarter prevent treasury drain, ensuring sustainability.

Product Linkage: Repurchased tokens used for utility perks, fee rebates, or liquidity incentives extend demand beyond the buyback itself.

Buybacks succeed when they feel engineered, not promotional.

How to Measure Buyback Impact

When a project launches a buyback, track these indicators to understand whether the program genuinely matters:

30/60/90-day price windows: sustained support vs quick fade

Pump strength + duration: wick vs multi-week floor

Impact per dollar: spend efficiency relative to market depth

Volatility changes: downside compression is a strong signal

Wallet retention: high retention = real demand

Market cap gained per dollar spent: efficiency score

Context overlay: check against unlocks, vesting cliffs, and supply flows

This is how you distinguish a real structural catalyst from a market stunt.

Wrapping Up

Buybacks are plumbing, not fireworks. If a buyback only works when everyone is watching, it’s theatre. If it holds when no one is looking, it’s support.

Treat every buyback as a contract between the project and the market:

Spend must be justified

Execution should be invisible

Proof must be on-chain and auditable

Rules should remain consistent both in risk-on and risk-off weeks

Teams that approach buybacks like operators not promoters are the ones that earn credibility.