Loading Search...

Explore the top RWA assets on different blockchains, from tokenized Treasuries to real estate and how RWAs are transforming global finance.

Author: Kritika Gupta

Blockchain has moved far beyond its original role as the backbone of cryptocurrencies. In 2026, one of its most important use cases is the tokenization of Real World Assets, commonly known as RWAs. This sector sits at the intersection of traditional finance and decentralized infrastructure. It brings Top RWA assets that people already understand, such as U.S. Treasuries, real estate, gold, private credit, and equities, onto blockchain rails. As a result, investors can now access familiar assets through faster, more transparent, and more programmable financial systems.

This shift matters because it changes what blockchain is for. For years, many critics argued that crypto lacked real economic grounding. However, RWAs directly challenge that criticism. Instead of revolving around purely native digital assets, tokenization connects blockchain networks to instruments with legal rights. In other words, the market is no longer asking whether blockchain can support real finance. It is now asking how quickly traditional finance will migrate on-chain.

Real World Assets have become the clearest example of blockchain solving a real financial problem at scale. For years, crypto promised to rebuild finance with faster transactions, open access, and reduced intermediaries. Yet most activity remained concentrated in speculative trading, memecoins, and crypto-native yield strategies. RWAs changed that narrative because they introduced assets that already play central roles in the global economy.

The core appeal is simple. Traditional finance controls massive pools of value, but access remains uneven and inefficient. Real estate is one of the largest asset classes in the world, yet it is illiquid, expensive to enter, and slow to transact. Government bonds offer yield and stability, but they still move through legacy settlement systems. Private credit, commodities, and equities all operate through siloed infrastructure with fragmented access, regional restrictions, and layers of costly intermediaries. Tokenization breaks those barriers by creating digital representations of these assets on blockchain networks.

As a result, tokenization improves market access in several ways at once. First, it enables fractional ownership. Second, it enables 24/7 transferability and liquidity. Markets no longer need to close at the end of a trading day if the asset representation exists on-chain. Third, it enables programmability. Issuers can automate compliance, distributions, collateral rules, and settlement logic directly into the token structure.

Not all blockchain ecosystems serve RWAs in the same way. Each network brings its own tradeoffs in speed, cost, liquidity, compliance tooling, developer maturity, and institutional credibility. Therefore, different ecosystems have started to dominate different parts of the RWA stack.

Some chains attract institutions that value regulatory compatibility and deep liquidity. Others attract retail users who want cheap, fast access to tokenized assets. Some specialize in fixed-income products, while others focus on synthetic equities, real estate, private credit, or commodity settlement. In effect, the RWA market has developed into a multi-chain environment where each ecosystem builds around its strengths.

Solana has emerged as one of the most active ecosystems for user growth in tokenized assets.Solana now leads in the number of wallets holding RWAs, with about 154,000 holders. That figure highlights Solana’s main advantage: it excels at distributing asset access to a large retail user base.

The reasons are straightforward. Solana offers very low transaction costs, rapid execution, and a user experience that supports frequent activity. These features make it ideal for tokenized equities, synthetic stocks, and RWA products that require active market participation. On Solana, users can trade quickly without worrying that fees will consume small transactions. This alone gives the network an edge for retail-oriented financial products.

In 2026, Solana’s RWA footprint sits around $2.16 billion in TVL, and that number reflects more than passive holding. It reflects active use across exchanges, vaults, liquidity strategies, and synthetic markets.

This structure matters because it brings a familiar market behavior onto blockchain rails. Users can rotate between tokenized stocks, stablecoins, and crypto collateral within the same environment. They no longer need to think in terms of separate worlds of finance. Solana makes that interaction feel native and continuous.

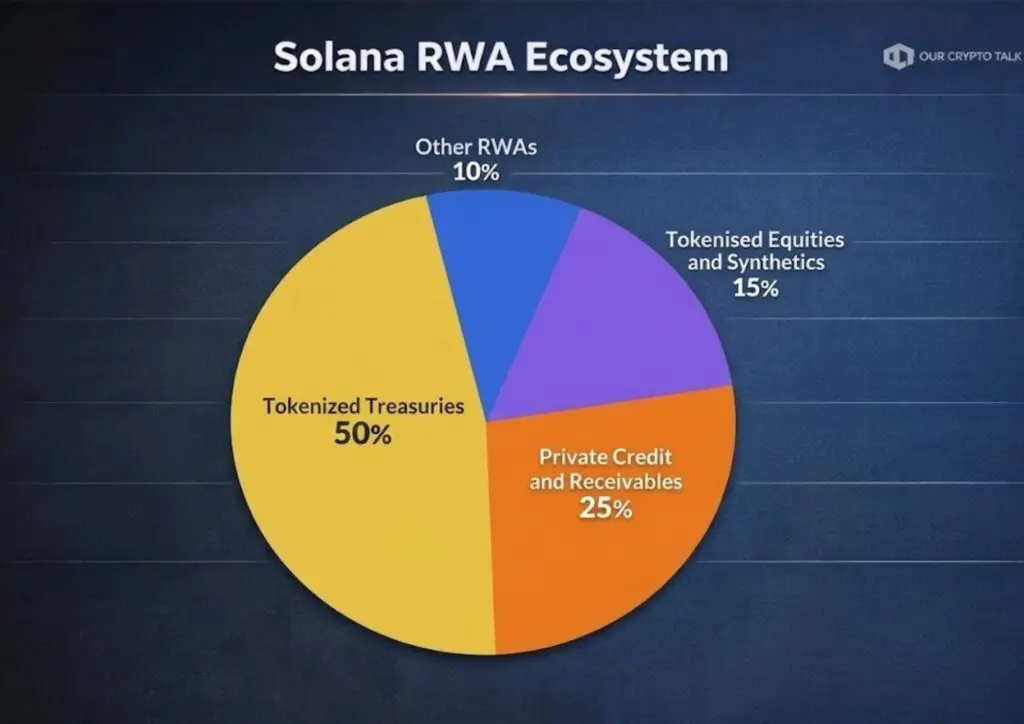

• Tokenized Treasuries (50%) – ~$1.08B in value, representing the largest share of Solana’s RWA ecosystem through tokenized U.S. Treasury exposure and yield-bearing government debt instruments.

• Receivables (25%) – ~$540M in value, consisting of tokenized loans, invoice financing, and private debt markets brought on-chain.

• Tokenized Equities and Synthetics (15%) – ~$324M in value, covering synthetic or tokenized exposure to traditional equities.

• Other RWAs (10%) – ~$216M in value, including smaller tokenized asset classes such as commodities.

Ethereum remains the most important blockchain for RWAs by value. With roughly $17 billion in RWA TVL, it anchors the institutional side of the market. This dominance reflects Ethereum’s strongest asset: credibility.

Institutions prefer Ethereum because it offers the deepest liquidity, the most established smart contract environment. Although Ethereum’s base layer remains more expensive than some alternatives, its network effects still matter more for many high-value applications. Large issuers want the security, composability, and familiarity that Ethereum provides.

Ethereum also leads in compliant token design. Standards such as ERC-1400 and evolving tokenized security frameworks allow issuers to administrative controls into the asset itself. This capability is crucial for institutions that cannot simply issue unrestricted on-chain instruments.

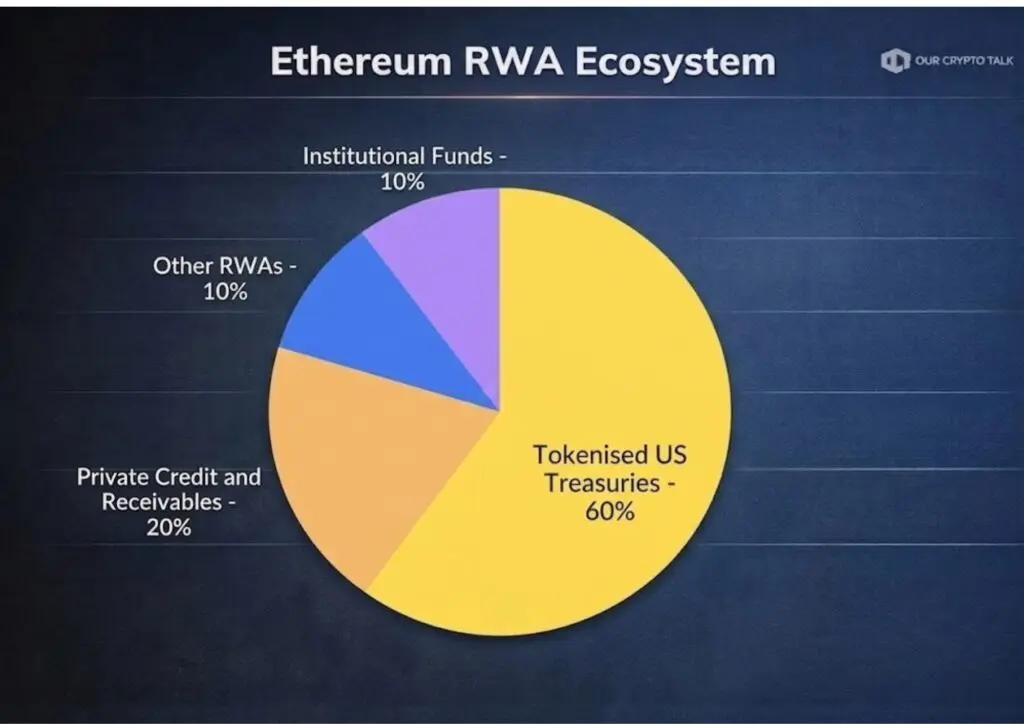

• Tokenized Treasuries (≈65%) – ~$11.05B in value, the dominant segment consisting of tokenized U.S. Treasury funds such as BlackRock’s BUIDL, Franklin Templeton’s BENJI, and Ondo’s OUSG.

• Private Credits (≈20%) – ~$3.4B, representing tokenized lending markets, invoice financing, and private credit.

• Tokenized Funds (≈10%) – ~$1.7B, including tokenized investment funds and equity-like exposure issued through regulated on-chain financial products.

• Other RWAs (≈5%) – ~$850M, covering smaller tokenized asset categories such as commodities.

Avalanche has carved out a distinct position in the RWA market by focusing on enterprise customization. Its subnet architecture allows organizations to launch tailored blockchain environments with specific rules, validators, and compliance parameters. That flexibility makes Avalanche particularly suitable for real estate, private credit, and enterprise-grade issuance.

The network’s RWA activity has grown to about $1.3 billion in TVL, with strong representation in real estate tokenization and credit markets. Similarly, credit protocols such as Maple Finance have used Avalanche-linked infrastructure to support more specialized institutional lending environments.

Avalanche’s architecture is especially attractive for sectors that require controlled environments. Real estate tokenization, for example, often involves region-specific legal structures, ownership records, and investor restrictions. A customizable blockchain environment helps issuers manage those requirements more directly. The same logic applies to private credit and enterprise debt products, where compliance cannot be treated as an afterthought.

Of course, flexibility can also create fragmentation. If capital and applications spread too thinly across multiple subnets, liquidity may become harder to consolidate. Even so, Avalanche’s approach remains compelling for institutions that want blockchain efficiency without abandoning tailored infrastructure requirements.

• Real Estate Tokenization (40%) – Roughly $520M of Avalanche’s RWA market is concentrated in tokenized property assets, where platforms enable fractional ownership of income-generating real estate.

• Institutional Lending (30%) – Around $390M is tied to tokenized credit markets, supporting institutional lending structures and on-chain debt issuance through specialized protocols.

• Tokenized Funds and Structured Products (20%) – Nearly $260M represents tokenized investment funds and structured financial instruments designed for institutional capital deployment.

• Other RWAs (10%) – The remaining ~$130M covers smaller tokenized asset categories, including experimental financial instruments and emerging enterprise-grade tokenization use cases.

Polygon continues to play a key role as an accessible, lower-cost environment for tokenized assets. With roughly $2.5 billion in RWA TVL, the network has positioned itself as a bridge between Ethereum’s institutional depth and broader market accessibility.

One of Polygon’s strongest advantages is cost efficiency. This makes it well suited for tokenized products that require frequent interaction but do not necessarily need the highest-value settlement environment. It also makes Polygon appealing in emerging market contexts, where even moderate fees can become a barrier to adoption.

In 2026, Polygon’s RWA presence spans carbon credits, tokenized real estate, Treasury-linked products, and hybrid DeFi-RWA structures. It has also attracted activity tied to real estate experimentation in markets like India, where lower-cost blockchain infrastructure can support more inclusive participation.Polygon’s evolving zkEVM stack adds another layer of relevance.

Privacy, scalability, and Ethereum compatibility remain valuable features for tokenized assets that need both efficiency and interoperability. Therefore, Polygon continues to matter not because it dominates one category, but because it supports a wide range of practical tokenization use cases at manageable cost.

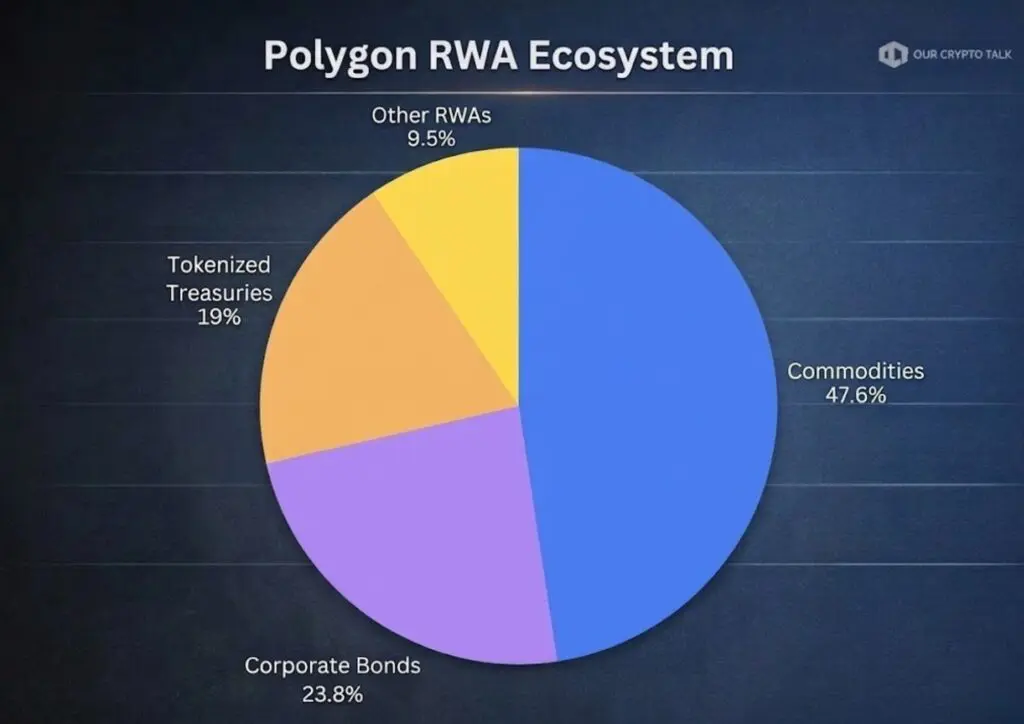

• Tokenized Treasuries and Yield Products (35%) – Approximately $875M of Polygon’s RWA ecosystem consists of Treasury-linked funds and yield-bearing instruments that bridge traditional finance with DeFi liquidity.

• Real Estate Tokenization (30%) – Around $750M is tied to tokenized property assets, enabling fractional ownership models and real estate experimentation in markets such as India.

• Carbon Credits and Environmental Assets (20%) – Nearly $500M represents tokenized carbon credits and sustainability-linked assets, an area where Polygon has become a prominent infrastructure layer.

• Hybrid DeFi Structures (15%) – The remaining ~$375M covers a mix of tokenized funds, experimental financial instruments, and hybrid DeFi-RWA products operating within Polygon’s low-cost ecosystem.

The XRP Ledger has leaned hard into one of its historic strengths: cross-border value transfer. In the RWA space, that has translated into growing traction for tokenized commodities, Treasuries, and institutionally issued assets designed for international settlement. Its tokenized asset footprint has climbed to around $3.2 billion in TVL in recent growth cycles.

The appeal is clear. XRP Ledger offers fast finality, relatively low costs, and an architecture that many financial firms already associate with payments infrastructure. When combined with tokenized assets, those features create a useful environment for moving value across jurisdictions more efficiently than legacy systems.

Projects such as Archax and institutional issuance partners have helped position the network as a home for regulated asset transfer rather than purely retail speculation. Tokenized gold and Treasury-linked instruments fit especially well in this model because they can serve both as investments and as settlement tools in international financial flows.

That said, XRP Ledger faces competition from newer ecosystems chasing the same cross-border and institutional use cases. Still, its identity remains coherent. It is building around governed issuance, payments efficiency, and financial connectivity, which makes it increasingly relevant for tokenized assets designed to move across borders.

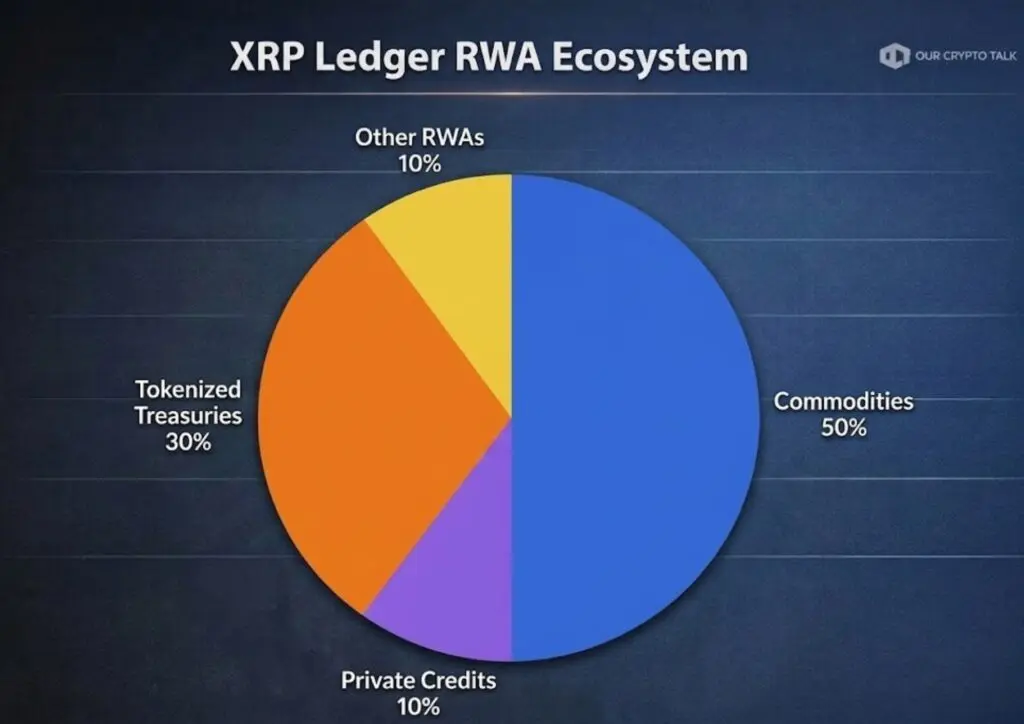

• Tokenized Treasuries and Funds (40%) – Roughly $1.28B of the XRP Ledger’s RWA ecosystem is tied to Treasury-backed and institutional fund products used for regulated asset settlement and yield generation.

• Tokenized Commodities (30%) – Around $960M is represented by tokenized commodities such as gold and precious metals, which function both as investment instruments and cross-border settlement assets.

• Institutional Financial Assets (20%) – Nearly $640M consists of regulated institutional issuances, including tokenized securities and financial products facilitated by platforms such as Archax.

• Other RWAs (10%) – The remaining ~$320M includes smaller tokenized asset categories such as experimental cross-border financial instruments and emerging institutional tokenization projects.

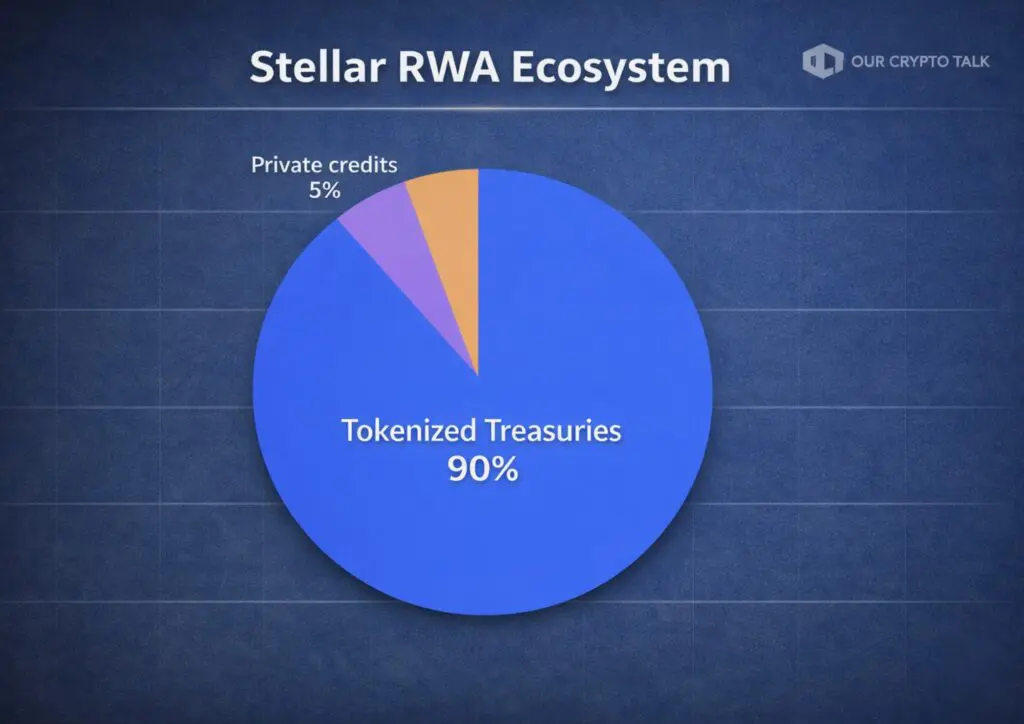

Stellar has consistently focused on low-cost financial access, and that orientation translates naturally into RWAs. In 2026, the network has built meaningful traction in tokenized fixed-income products and accessible yield instruments, with around $2.8 billion in tokenized asset activity.

The network works especially well for users and issuers who care about affordability and simplicity. Treasury products and other fixed-income instruments fit this model because they appeal to users looking for straightforward yield rather than high-frequency trading or complex leverage strategies. Stellar’s architecture supports that use case with low fees and a relatively clear payments-driven design.In emerging market contexts, this matters a great deal.

A user does not need to move large sums to benefit from tokenized yield if the blockchain itself remains cheap to use. That accessibility gives Stellar a practical role in the broader RWA map, particularly for financial inclusion and low-cost settlement.

• Tokenized Treasuries and Government Debt (45%) – About $1.26B of Stellar’s RWA activity is tied to Treasury-backed products that provide stable yield through tokenized government debt instruments.

• Fixed-Income and Yield Products (30%) – Roughly $840M consists of tokenized bonds and fixed-income instruments designed to offer predictable returns for users seeking simple yield exposure.

• Institutional Funds and Structured Products (15%) – Around $420M is represented by tokenized investment funds and structured financial instruments issued through regulated partners.

• Other RWAs (10%) – The remaining ~$280M includes smaller tokenized asset categories such as experimental financial products and regional financial inclusion initiatives.

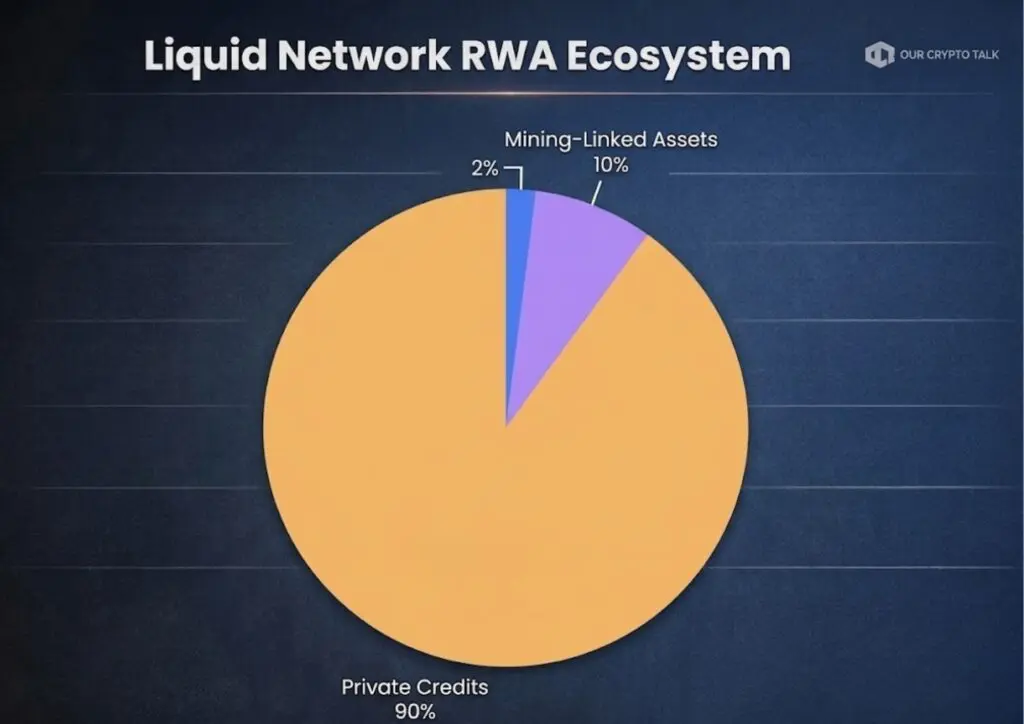

Liquid Network occupies a narrower but still important niche. As a Bitcoin-linked sidechain focused on confidential transactions, it appeals to institutions and users who prioritize privacy and Bitcoin-adjacent infrastructure. Its RWA market remains smaller than Ethereum, Solana, or XRP Ledger, at around $800 million in TVL, but it serves specialized functions that larger general-purpose chains do not always prioritize.

Private credit and discreet asset transfer represent two of Liquid’s more natural applications. Tokenized stocks, bonds, and Bitcoin-linked instruments can move within an environment that reduces public visibility. For institutions that value confidentiality, this matters. In markets where visibility can affect strategy, privacy remains a feature rather than a compromise.

Liquid is unlikely to dominate broad retail tokenization. However, it does not need to. Its importance lies in serving a segment of the RWA market that wants the efficiency of blockchain without the radical transparency of most public networks.

• Private Credit and Institutional Lending (40%) – Roughly $320M of Liquid Network’s RWA activity is tied to private credit markets where institutions can issue and transfer debt instruments with greater transaction confidentiality.

• Tokenized Securities and Bonds (30%) – Around $240M consists of tokenized stocks and bond-like instruments that move within Liquid’s confidential settlement environment.

• Bitcoin-Linked Financial Instruments (20%) – Nearly $160M represents Bitcoin-backed or BTC-linked financial assets designed for institutional settlement and treasury strategies.

• Other Confidential RWAs (10%) – The remaining ~$80M includes niche tokenized assets and experimental financial products that benefit from Liquid’s privacy-focused architecture.

The RWA market often gets discussed as a single sector, but that can hide a crucial distinction. Not all real-world assets are equally tangible, and not all tokenized structures convey the same kind of claim. Some represent physical assets that exist in vaults or on land registries. Others represent legal rights, debt claims, or synthetic exposure. Therefore, investors need to examine not just what blockchain an asset lives on, but what the token actually represents.

This distinction shapes both opportunity and risk. Tangible assets often feel more intuitive because they map to physical property. Intangible assets may offer better liquidity or yield, but they depend more heavily on legal frameworks and counterparties.

Tokenized U.S. Treasuries sit at the center of the current RWA boom. They account for the majority of the sector by value and have become the preferred entry point for many institutions. Their rise makes sense. Treasuries already carry strong legitimacy in global finance. When tokenized properly, they bring that legitimacy on-chain.

These products usually represent claims on short-duration government debt held through regulated custodians or fund structures. That means users do not hold a Treasury bill directly in the way they might hold a crypto token natively. Instead, they hold a tokenized representation of beneficial exposure. Even so, the value proposition remains strong. Investors gain access to a relatively low-risk, yield-bearing instrument that can settle more efficiently and interact with decentralized applications.

• Tokenized U.S. Treasuries dominate the RWA boom with roughly $11B of ~$25–26B total sector TVL, making them the most trusted institutional entry point into on-chain finance.

• Ethereum leads with about $15.2B in RWA TVL, reflecting its maturity, compliance tooling, and concentration of flagship Treasury products like BlackRock BUIDL and Franklin BENJI.

• Liquid Network (~$1.8B) and Solana (~$1.7B) show strong traction, driven by demand for efficient settlement, privacy-focused structures, and yield-bearing Treasury access.

• Stellar (~$1.4B) remains heavily Treasury-centric, with tokenized government debt forming the vast majority of its RWA exposure through institutional offerings.

• Avalanche (~$0.59B), Polygon (~$0.46B), and XRP Ledger (~$0.45B) hold smaller but expanding shares, often tied to targeted partnerships, regional adoption, or niche financial use cases.

• While granular Treasury-only breakdowns per chain are not always disclosed, overall RWA TVL serves as a reliable proxy since Treasuries represent the largest and most credible asset category in the sector.

Tokenized stocks occupy a very different place in the market. They are popular because they make familiar equity exposure available in blockchain environments, often around the clock. However, they also sit closer to the edge of legal and structural complexity.

In many cases, tokenized stocks are not direct registered shares. They may be synthetic assets, wrapped exposures, or tokenized claims that rely on custodians, derivatives, or counterparties. This means the token’s price may track a real stock, but the legal rights attached to it can differ significantly from owning the underlying security through a traditional brokerage.

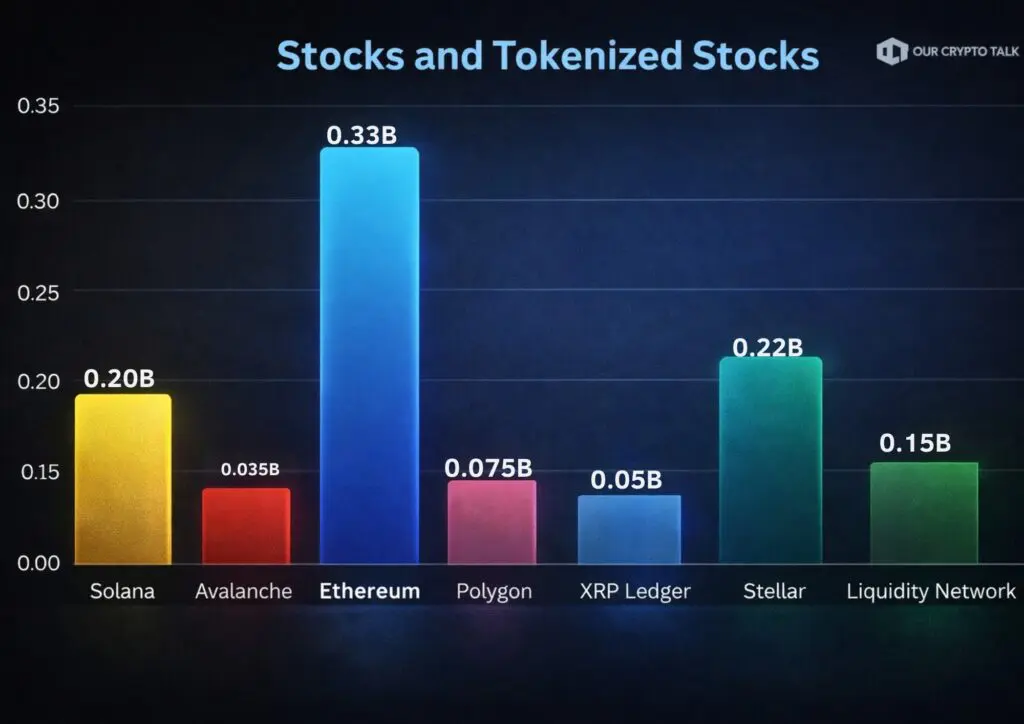

• Tokenized stocks form a smaller but rapidly expanding RWA segment (~$500M–$1B total TVL), offering synthetic exposure to major equities like Apple, Tesla, Nvidia, and index ETFs through blockchain tokens.

• These assets typically provide 24/7 trading, fractional ownership, and DeFi composability, allowing global retail users to access equity price movements without relying on traditional brokerage infrastructure.

• Ethereum (~$300–400M) remains the institutional backbone for tokenized equities, hosting compliant issuance frameworks and many of the largest tokenized stock providers.

• Solana (~$200–300M+) leads the retail-driven tokenized stock narrative, benefiting from ultra-low fees, high throughput, and strong adoption of products mirroring popular tech equities.

• Polygon (~$50–100M) and Avalanche (~$20–50M) maintain emerging footprints, often tied to specific integrations, scaling solutions, or niche issuer ecosystems.

• Stellar (~$20–50M) shows limited activity in tokenized stocks compared with its strong focus on Treasury products and institutional fixed-income tokenization.

• XRP Ledger and Liquid Network show minimal presence (~$5M each) in tokenized equities, reflecting their stronger orientation toward payments infrastructure or Treasury-centric institutional products.

Real estate remains one of the most compelling categories in the RWA story because it translates easily into the logic of tokenization. Property is expensive, illiquid, and geographically fragmented. Tokenization addresses all three problems at once by splitting ownership into smaller digital units.

A tokenized real estate product can represent direct ownership, beneficial interest, rental income rights, or participation in a special purpose vehicle. The exact structure varies, but the core appeal remains the same. Investors can access real estate exposure without having to buy whole properties or navigate every legal and operational layer personally.

• Tokenized real estate represents a nascent but promising RWA segment with TVL in the low hundreds of millions, focused on fractional ownership of high-value physical assets like commercial buildings, land, and rental portfolios.

• These products enable lower entry barriers, global investor access, and potential rental or dividend yield on-chain, often structured through SPVs, REIT-like tokens, or debt tranches backed by property income.

• Ethereum (~$100–150M+) leads institutional real estate tokenization, hosting compliant issuance platforms, private property funds, and programmable ownership frameworks.

• Stellar (~$70–100M) stands out due to dedicated platforms like RedSwan, which tokenize equity tranches in U.S. commercial properties and drive much of the chain’s real estate activity.

• Polygon (~$20–50M) and Solana (~$10–30M) show early momentum for retail-friendly fractional property exposure, leveraging lower fees and faster settlement for secondary trading experiments.

• Avalanche (~$5–20M) maintains a niche but growing footprint through targeted partnerships and pilot tokenized property initiatives.

• XRP Ledger (~$0–10M) and Liquid Network (~$0–5M) have minimal presence in real estate RWAs, with ecosystem focus currently tilted toward payments infrastructure or Treasury-centric products.

Gold brings a different kind of legitimacy to the RWA market. It is a physical asset with centuries of monetary history, and tokenized gold products lean heavily on that trust. Tokens such as PAXG and Tether Gold usually represent claims on vaulted physical gold held by custodians.

This structure gives investors a straightforward proposition. They gain blockchain transferability while retaining exposure to a well-known inflation hedge. Unlike tokenized stocks, the appeal here does not come from synthetic market access or financial engineering. It comes from digitizing a familiar tangible reserve asset.

• Tokenized gold represents a mid-hundreds-of-millions TVL RWA category, digitizing vaulted bullion into blockchain tokens that provide fractional access and seamless global transferability.

• These products typically use fully backed custody models with 1:1 reserve claims, allowing holders exposure to physical gold.

• Ethereum (~$400–500M+) dominates tokenized gold liquidity, hosting major bullion-backed tokens and deep DeFi integrations for lending, collateralization, and trading.

• Polygon (~$120–200M) strengthens retail accessibility by enabling low-cost transfers and scaling distribution of gold tokens bridged from Ethereum.

• Avalanche (~$50–100M) and Solana (~$30–70M) show growing experimentation with tokenized commodities, supporting faster settlement environments

• Stellar (~$20–50M) maintains a niche role focused on compliant issuance frameworks and cross-border settlement use cases tied to commodity tokenization.

• XRP Ledger (~$10–30M) and Liquid Network (~$5–15M) have limited but emerging deployments, often linked to remittance corridors.

• As a non-yielding defensive asset, tokenized gold primarily serves inflation-hedging and diversification needs, but remains dependent on custody transparency.

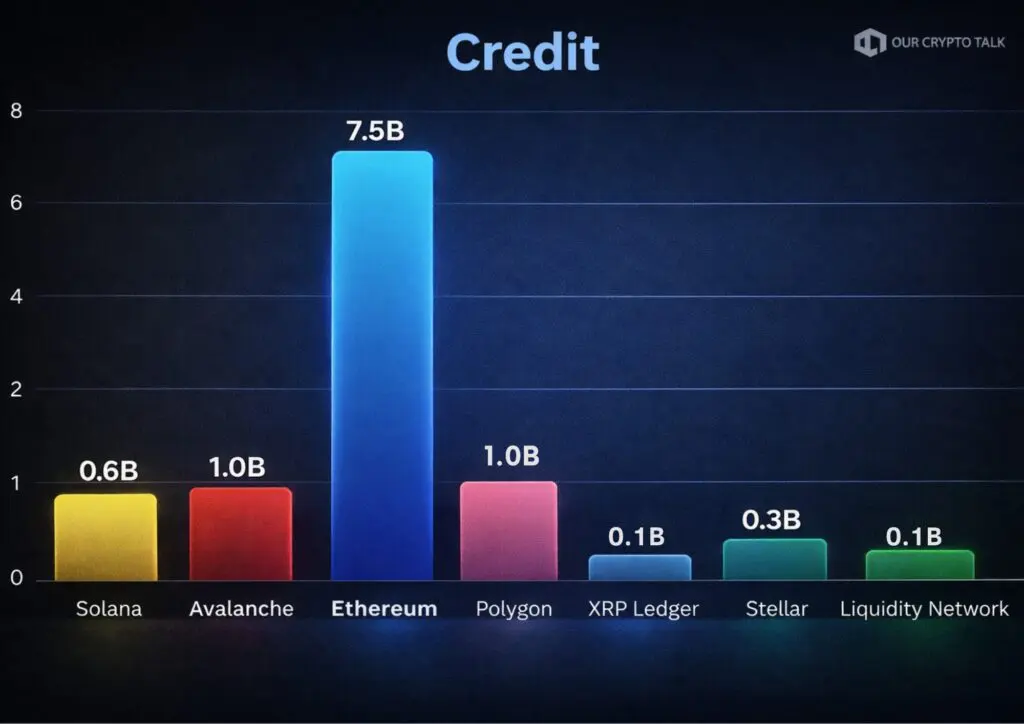

Private credit and on-chain lending represent one of the most interesting but structurally complex parts of the RWA market. Credit instruments are intangible by nature. They derive value from repayment obligations, underwriting standards, and collateral structures rather than from physical existence.

Protocols such as Centrifuge and Maple Finance have brought parts of this market on-chain by tokenizing receivables, loans, and institutional credit products. Smart contracts can automate repayment schedules, collateral triggers, and lender distributions. This creates a more transparent structure than many off-chain private credit arrangements.

• Tokenized credit has become a multi-billion-dollar RWA segment (~$10B–12B globally), bringing private loans, receivables, trade finance, and institutional debt instruments onto programmable blockchain rails.

• These assets represent claims on future cash flows rather than physical collateral, with smart contracts helping automate repayment schedules, collateral triggers, yield distribution, and lender reporting.

• Ethereum (~$7–8B) is the dominant hub for tokenized private credit, driven by institutional platforms, diversified lending pools, and mature DeFi infrastructure.

• Polygon (~$1.2–1.8B) and Avalanche (~$0.8–1.3B) have developed meaningful credit footprints through structured vaults, lending experiments, and scalable settlement environments.

• Solana (~$0.4–0.9B) is emerging as a faster, retail-accessible venue for on-chain credit products and fintech-linked lending markets.

• Stellar (~$0.2–0.5B) shows smaller but relevant activity, particularly in trade-finance and fintech-oriented credit issuance.

• XRP Ledger (~$0.1–0.3B) and Liquid Network (~$0.05–0.15B) remain niche participants, with limited but growing experimentation in tokenized lending and institutional credit structures.

Despite its momentum, the RWA market still faces serious challenges. Investors should not confuse rapid growth with perfect infrastructure. Several risks remain central to the sector.

First, tokenized assets depend on off-chain truth. A Treasury token needs a real custodian. A gold token needs audited reserves. A real estate token needs enforceable ownership rights. In every case, blockchain handles transfer and programmability.

Second, oracle risk remains significant. When smart contracts rely on price feeds or reserve data, the quality of those feeds becomes critical. A failure in data delivery can create market instability, liquidations, or inaccurate pricing.

Third, regulatory divergence still complicates expansion. What qualifies as a tokenized security in one jurisdiction may face different treatment in another. This is particularly relevant for equities, private credit, and cross-border asset issuance.

Fourth, liquidity fragmentation remains a structural issue. An asset may be tokenized, but if secondary markets remain thin, practical liquidity may still fall short of expectations.

The industry has responded with several mitigations. Multi-oracle models reduce data dependency on a single provider. Insurance layers and risk reserves help address technical failure. Compliance-aware token standards improve legal control. Cross-chain interoperability and better market infrastructure continue to improve liquidity.

These solutions do not eliminate risk, but they do show that the sector is maturing. Investors should still approach RWAs with due diligence, yet the market is no longer operating as a loose collection of experiments. It is becoming more structured, more audited, and more institutionally legible.

Real World Assets have become one of the most credible narratives in blockchain because they connect digital infrastructure to familiar economic value. They do not ask the market to believe in abstraction alone. Instead, they bring bonds, property, commodities, and credit into environments where capital can move faster, settle more efficiently, and reach more participants.

That does not mean every tokenized asset will succeed. Some products will remain too complex, too illiquid, or too dependent on weak off-chain structures. However, the broader direction is clear. Finance is becoming more programmable, more composable, and more globally accessible.

Therefore, the tokenization of the tangible and intangible is not just a niche trend within crypto. It is a larger restructuring of how value can be represented, moved, and used. In 2026, that restructuring is still in progress. Yet it has already advanced far enough to show that RWAs are not a side story. They are one of the clearest blueprints for blockchain’s future role in global finance.