Loading Search...

Why TVL may be one of DeFi’s most misleading metrics and why investors should look beyond locked value to judge protocol growth.

Author: Arushi Garg

You have probably seen this play out many times in the DeFi market. A new DeFi protocol launches. Within weeks, the team is posting milestones like $500 million in Total Value Locked (TVL), then $1 billion shortly after. The crypto community celebrates, investors rush in, and the protocol’s token price starts pumping.

Everything looks like success.

But six months later, the protocol is quiet. Activity drops, users disappear, and the once-impressive TVL figure collapses overnight. The platform becomes a ghost town. If Total Value Locked was truly the best indicator of DeFi health, why didn’t anyone see the decline coming? The answer is simple. TVL is often misunderstood and frequently misused. Over time, it has become one of the most misleading metrics in decentralized finance.

Ask almost any DeFi investor or analyst what defines a successful protocol and the first answer you will hear is TVL. Total Value Locked sounds authoritative. It appears to represent adoption, liquidity, and trust. Because of that, it became the default metric used to measure the growth of DeFi platforms.

But TVL did not become the industry standard because it was the most accurate measurement. It became popular because it was the easiest number to track. In the early days of decentralized finance, protocols such as MakerDAO and Compound began publishing the amount of ETH deposited in their smart contracts. Crypto media and data dashboards started reporting these figures, and soon TVL became the shorthand for measuring DeFi growth.

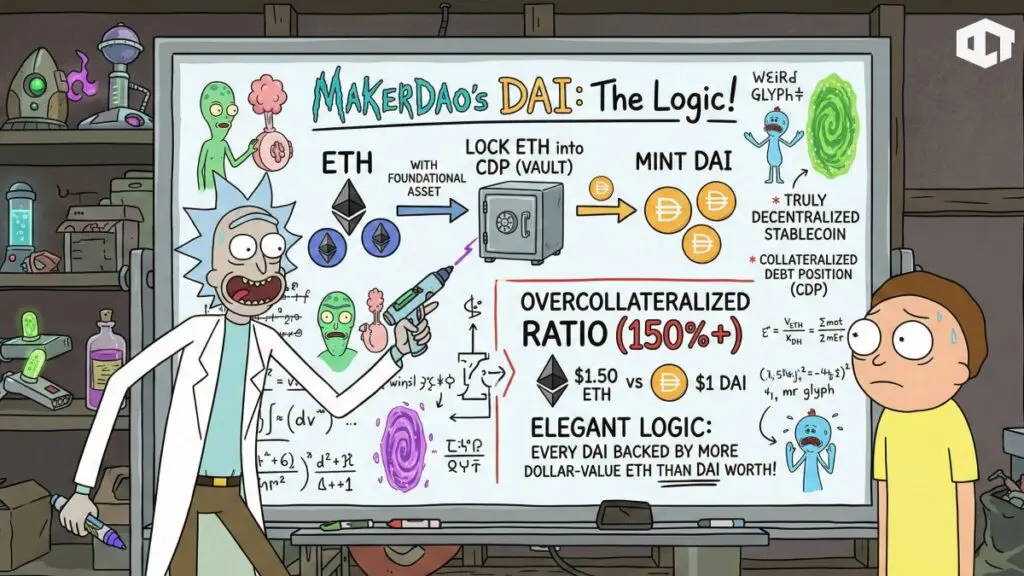

For example, DAI, the decentralized stablecoin created by MakerDAO, was backed primarily by Ethereum collateral rather than traditional fiat reserves. Users would lock ETH into Collateralized Debt Positions (CDPs), later called Vaults, and mint DAI against that collateral. The system required overcollateralization, typically 150 percent or more, meaning the value of locked ETH always exceeded the value of the DAI issued.

This design made DAI one of the first truly decentralized stablecoins and helped establish the early credibility of DeFi. But it also helped create the industry’s obsession with Total Value Locked, a metric that would eventually become far more influential than it should have been.

The issue is simple: Total Value Locked (TVL) only measures one thing, how much money is sitting in a smart contract. That’s it. It doesn’t show whether the money is actually being used, if the protocol is generating revenue, or if real users are engaged. A few whales could be gaming incentives, yet rankings, VC decks, and crypto media still lead with TVL. It’s like judging a restaurant by how full the parking lot is, without checking if there’s food inside.

TVL counts:

TVL does not track:

A protocol can boast $3 billion in TVL and generate almost no revenue. High TVL does not guarantee token price stability, as seen with Aptos, which hit new lows despite its all-time high TVL.

When a protocol offers 40% APY in its own token, deposits often surge. But most users are not joining because they believe in the product. They are chasing high yields.

This makes TVL spike quickly, giving the impression that the protocol is thriving. In reality, the token supply is being diluted through emissions. Once those rewards decrease, the same capital often leaves just as fast.

High TVL without real revenue can become unsustainable. What matters more are metrics that reflect genuine usage, such as protocol revenue, fee revenue relative to TVL, active wallet retention, and organic trading volume. These indicators are far harder to manipulate and provide a clearer picture of long term protocol health.

In DeFi, the same asset can inflate multiple TVL numbers across different protocols, creating a misleading sense of scale.

For example:

One ETH can show up four times. Even trusted trackers like DeFiLlama struggle with this and promised fixes back in 2022, yet the issue persists. This means TVL figures often overstate actual capital, making it a poor gauge of real activity.

Most aggregators still report raw TVL without properly adjusting for recursive collateral. When you hear DeFi has $100B in TVL, the actual value of unique assets could be much lower. This is not a reporting error. It is a feature that is often ignored because larger numbers attract attention.

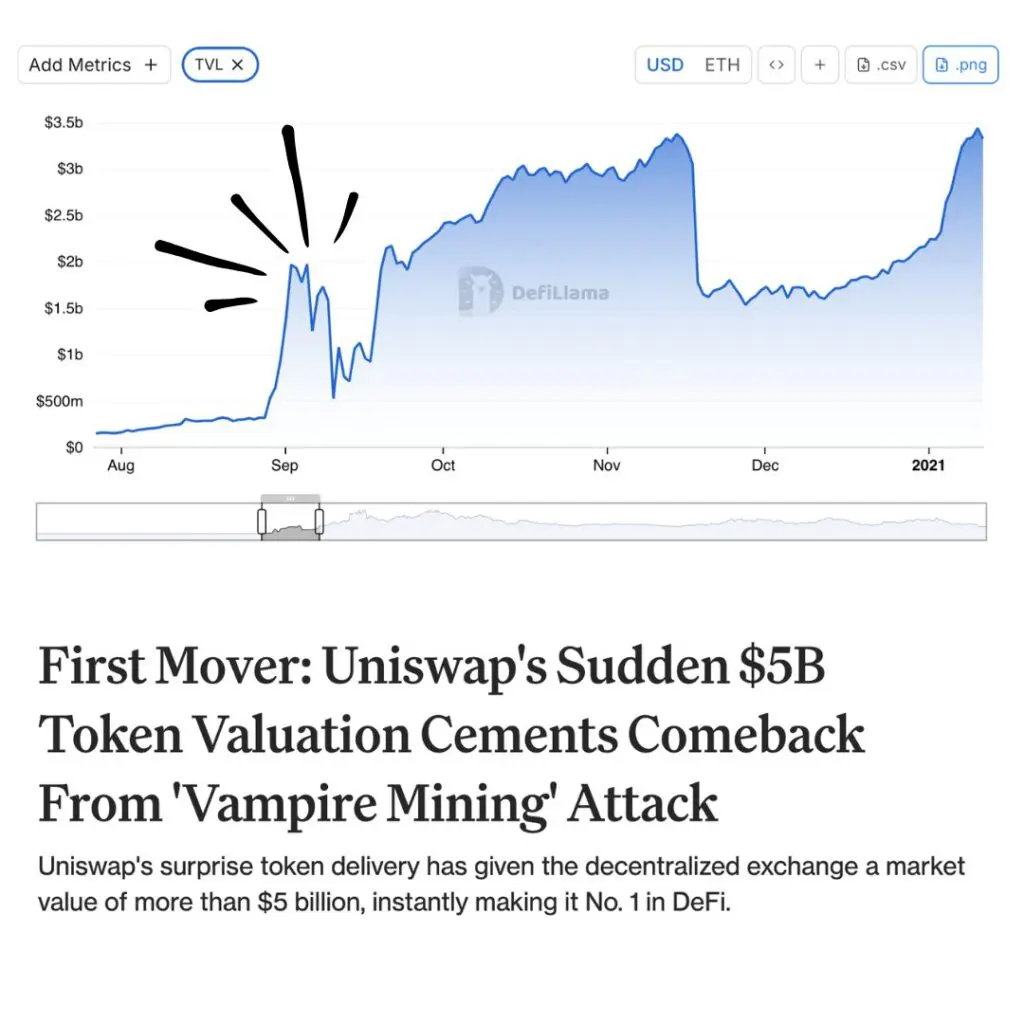

Mercenary capital moves to wherever yields are highest with no loyalty to any protocol. It inflates TVL quickly and leaves just as fast. A classic example is the SushiSwap attack on Uniswap in September 2020.

SushiSwap offered massive SUSHI token incentives and invited Uniswap liquidity providers to migrate. Over $800 million shifted in less than a week. Uniswap’s TVL collapsed while SushiSwap seemed to dominate. When incentives dropped, the capital left, showing that TVL growth was not organic adoption but short-term yield chasing. Uniswap continued building and eventually recovered, proving true resilience is measured differently.

This pattern repeats constantly across DeFi. Every major chain launch with big incentives, Avalanche Rush, BSC liquidity mining, L2 airdrop campaigns—follows the same path. TVL spikes rapidly. Founders celebrate. Once rewards slow, deposits drain quietly while the headlines stay positive.

Anchor Protocol provides one of the harshest lessons. In February 2022, the Terra/Luna ecosystem offered 20% APY on UST deposits. TVL soared as users chased yield, but the growth was not sustainable. When incentives or confidence faltered, the protocol’s apparent health vanished, showing that TVL alone never indicates true protocol resilience.

At its peak, Anchor Protocol held over $14 billion in TVL and was one of the most talked-about DeFi projects. Analysts praised it as the “savings account of DeFi” and the community celebrated the rising numbers.

Then disaster struck. In May 2022, UST depegged, and Luna’s price plummeted from $80 to almost nothing within 72 hours. Around $40 billion in value was wiped out, and Anchor’s TVL dropped to zero. Hundreds of thousands of users lost real money, proving that high TVL does not equal safety or sustainability.

Anchor’s collapse shows that TVL alone cannot predict risk. In the weeks before the UST depeg, its TVL looked stronger than ever, giving a false sense of security.

Contrast this with GMX, a decentralized perpetuals exchange on Arbitrum. Its TVL was smaller than giants like Curve or Aave, but it generated consistent real revenue from trading fees. Its high revenue-to-TVL ratio highlighted genuine growth and sustainability, proving that solid fundamentals matter far more than headline TVL numbers.

A protocol with $500M TVL and real revenue is far healthier than one with $5B TVL propped up by subsidized yields. TVL alone is misleading.

Smart DeFi investors focus on harder-to-fake metrics:

These numbers reveal sustainable growth and real usage, unlike TVL, which can be inflated by temporary incentives.

Uniswap is a prime example of efficiency in DeFi. At times it has generated more fee revenue than protocols with five to ten times its TVL. This shows that real products create actual value. Revenue does not lie.

TVL has been weaponized to attract capital and mislead retail investors. New protocols launch with massive token incentives, drawing in liquidity and announcing billion-dollar TVL figures. Media and investors amplify the FOMO. When token launches or fundraising rounds happen, insiders sell into liquidity, incentives slow, TVL drops, and retail investors are left holding losses. This playbook repeats across multiple protocols and is not technically fraud, just a selective use of a misleading metric.

DeFi must adopt better standards. Metrics should shift to real yield, tracking actual revenue, organic volume that persists without incentives, and user engagement showing genuine product-market fit. Platforms like Token Terminal already track revenue, P/S ratios, and earnings across protocols in ways similar to traditional finance.

Protocols should report transparently on revenue, utilization, and the composition of TVL, while media and investors must stop glorifying raw TVL numbers. The key question for any DeFi protocol is not TVL, but revenue, real users, and what happens if incentives are removed. DeFi’s future is exciting, but it will be built on real products serving real users. TVL had its moment. The industry must now focus on metrics that actually matter.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.