Loading Search...

The DeFi token curse is real. Data shows 51.75% of protocols with product-market fit collapse after launching tokens. Here's why to avoid it.

Author: Tanishq Bodh

There is a dirty secret in DeFi that nobody wants to say out loud. Launching a token might be the worst decision a successful protocol can make : The DeFi Token Curse.

That sounds heretical in crypto. The entire industry runs on the exit-to-token playbook. Build product. Gain traction. Launch governance token. Airdrop. List. Moon. Retire. Except the data is now breaking that narrative in a way that is hard to ignore.

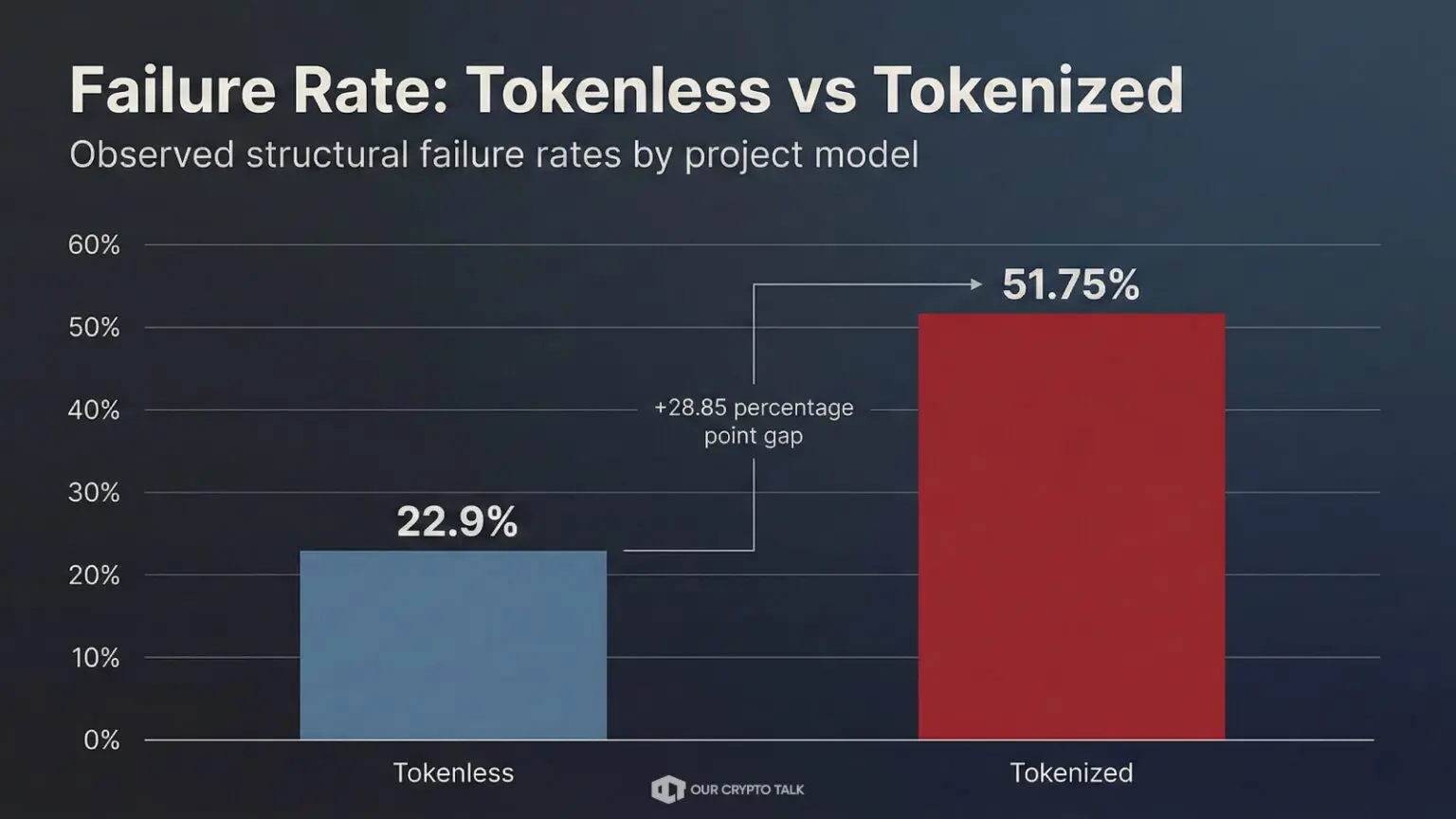

According to aggregated data from DeFiLlama, protocols that had already achieved genuine product-market fit, crossing $10 million in total value locked or generating $1 million in monthly fees, and then launched a token showed a 51.75 percent failure rate. More than half died.

Compare that to similar successful projects that never launched tokens. Their failure rate? Just 22.9 percent.

Let that sink in. If you already have product-market fit, tokenizing nearly doubles your odds of collapse. This is the DeFi token curse. And it’s structural, not coincidental. The token changes the physics of your protocol. Most teams underestimate how violently that physics can turn against them.

Tokens are rocket fuel. They ignite growth overnight. But they also attract the wrong kind of money.

When a protocol launches a token with emissions, yield incentives, and governance rewards, it sends a very specific signal to the market: there is yield to be farmed here. That signal works. Tokenized projects hit an average all-time-high TVL of $408.8 million, nearly double the $244 million peak of tokenless protocols. On paper, that looks like success. Bigger TVL, bigger numbers and of course bigger headlines.

Except that growth is synthetic. It is mercenary capital. Mercenary capital doesn’t care about your product. It doesn’t care about your roadmap, it doesn’t care about your community. It cares about APY. The moment emissions drop, the capital disappears, the moment price momentum stalls, liquidity leaves. The moment unlock schedules hit, farmers rotate to the next farm.

You are not building a protocol at that point. You are operating a subsidy program. And the data exposes how fragile that model really is.

Algo-stables with tokens: 100 percent failure rate. Twenty-two out of twenty-two dead. NFT lending with tokens: 100 percent failure rate. High-reflexivity protocols: near-instant death spirals. These weren’t fringe experiments. They were category leaders at various points. The problem is not that tokens exist. The problem is what they incentivize. When TVL is driven by emissions rather than utility, it is rented liquidity. And rented liquidity leaves the second rent is due.

TVL has always been DeFi’s favorite vanity metric. The higher the number, the stronger the narrative. But TVL doesn’t tell you whether users care. It tells you whether yield is attractive.

Tokenized protocols chase TVL because TVL justifies token price. Token price justifies emissions. Emissions justify TVL. It becomes a circular validation loop. At peak, everything looks unstoppable.

Consider the classic reflexive farming loop. Capital gets deposited. Rewards are farmed. Rewards are dumped. More rewards are emitted to compensate. Price weakens. Emissions increase to defend it. Liquidity providers leave. TVL collapses. That is not growth. That is a self-reinforcing feedback loop. And reflexive systems break violently.

The DeFi token curse doesn’t emerge from bad actors or bad luck. It emerges from a structural incentive design that looks good on the way up and catastrophic on the way down. Understanding this distinction is the first step to avoiding it.

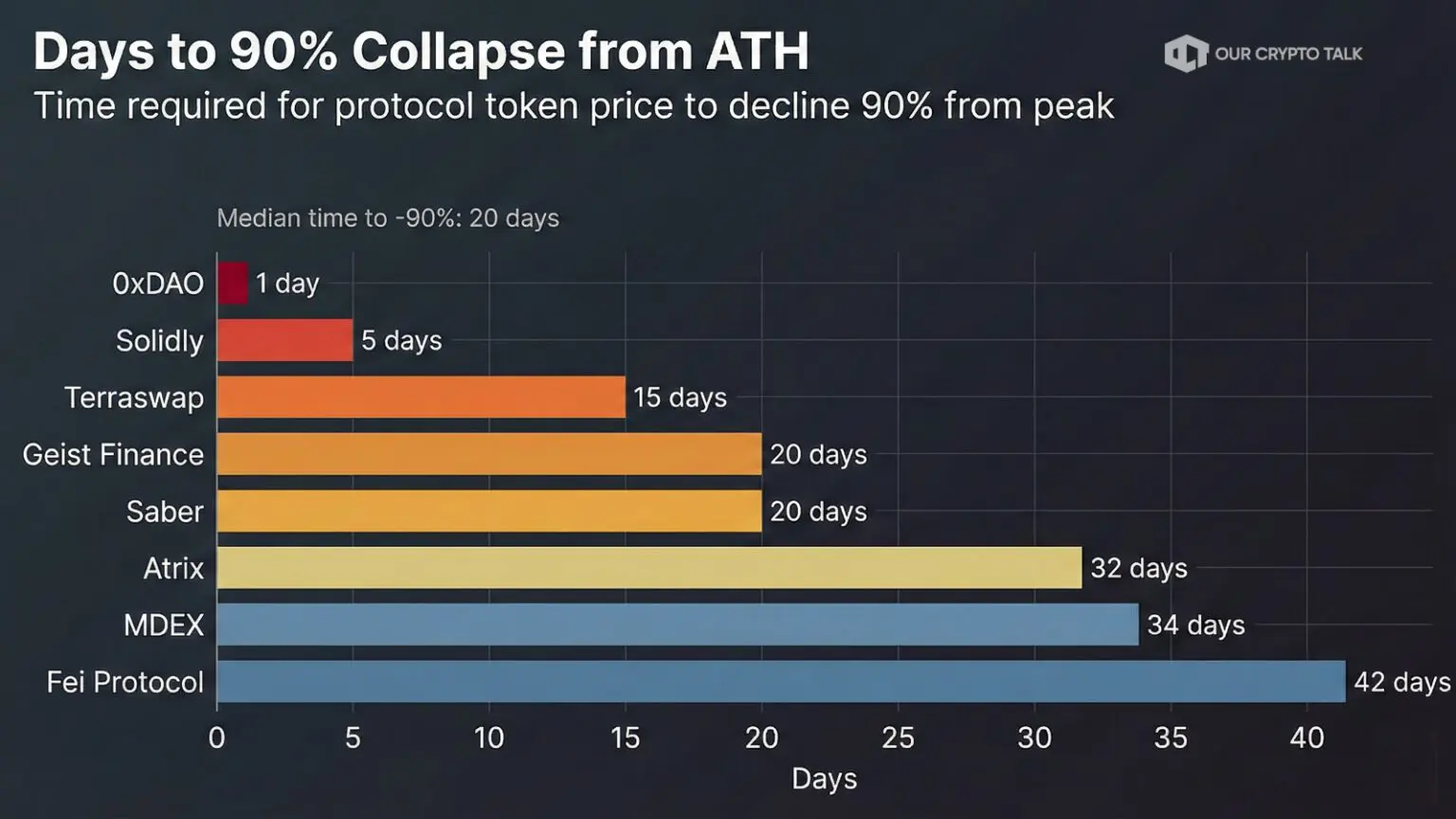

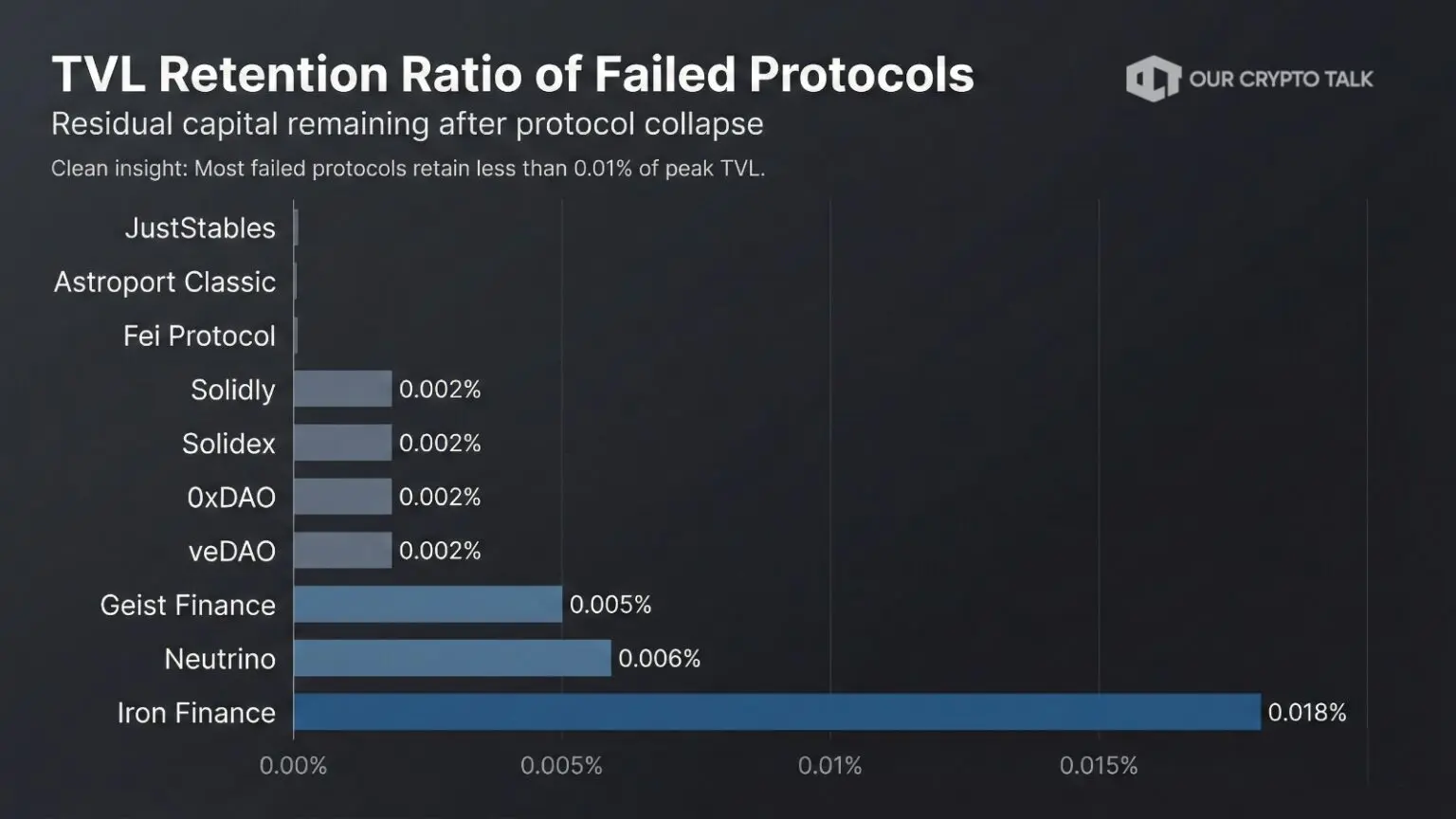

When tokenized protocols collapse, they don’t fade slowly. They explode. 0xDAO holds the record for one of the fastest multi-billion dollar evaporations in DeFi history. Peak TVL: $4.33 billion. Time to lose 90 percent: 48 hours after token launch. Two days. That is not market volatility. That is structural fragility.

The Saber-Sunny loop on Solana was even more extreme. Over $7.5 billion in combined TVL inflated through recursive farming loops. The same dollar recycled across multiple layers, sometimes magnified 600 percent. It looked like explosive adoption. It was leverage disguised as liquidity. When the loop broke, retention dropped to 0.13 percent. That is not a typo. The capital wasn’t sticky. It was synthetic.

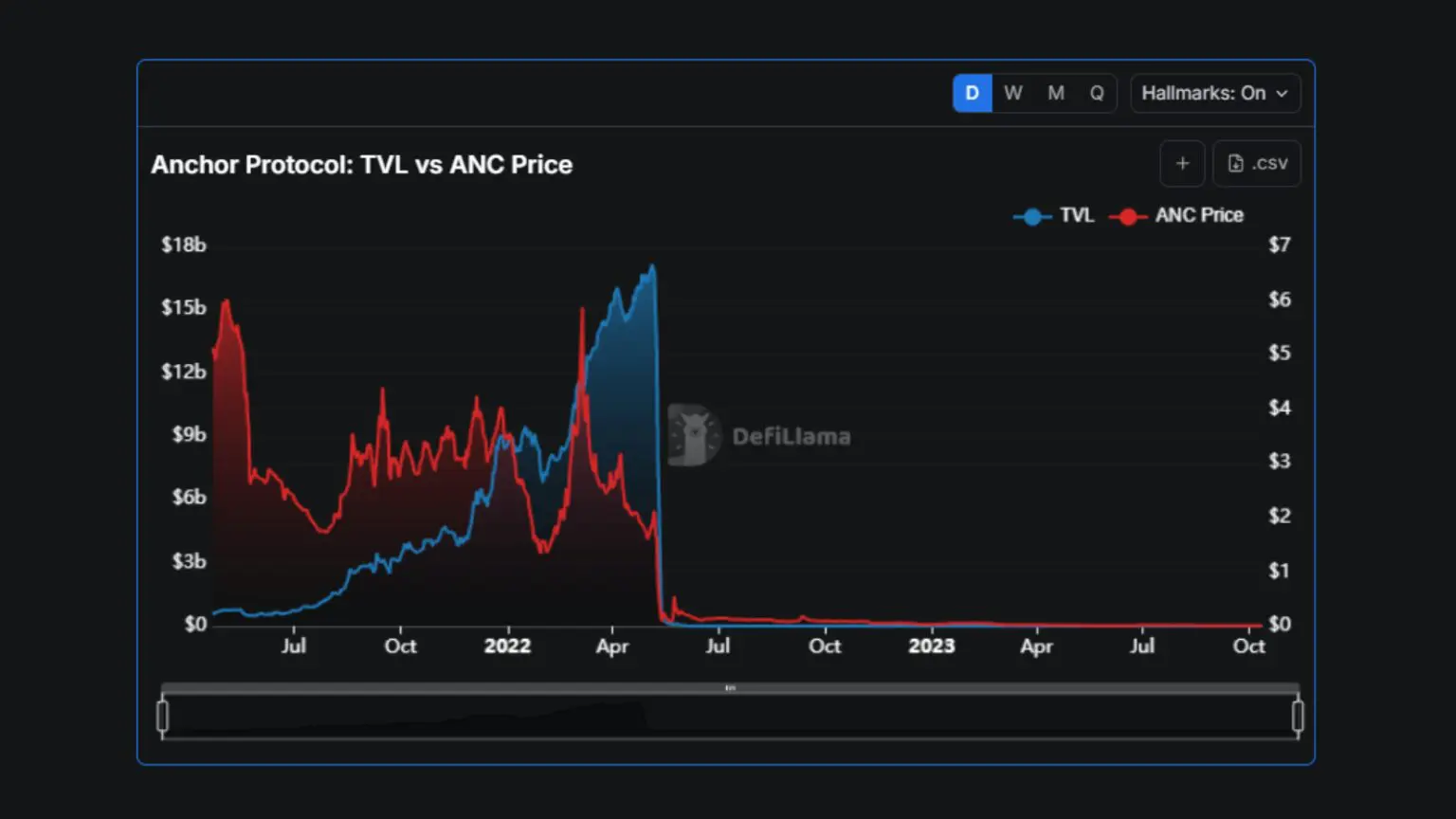

This pattern repeats across cycles. Mdex: 90 percent TVL loss in 24 hours. Saber: 90 percent gone within a day of peak. Geist Finance: $3.75 billion to effectively zero. These are not obscure failures. They were among the largest protocols on their respective chains.

For contrast, Terraswap operated without a token. It still died. But it took 134 days to hit a 90 percent drawdown. Without a token, the collapse was slower. There was no reflexive panic triggered by price freefall and simultaneous emissions collapse. Tokens accelerate both growth and destruction. When they break, they compress years of decline into days.

The DeFi token curse operates through three recurring mechanisms. The first and most violent is the reflexive death spiral.

Tokens create recursive loops. High emissions attract mercenary capital. Mercenary capital inflates TVL. Inflated TVL validates narrative. Narrative supports token price. Token price supports emissions. The loop feeds itself, until emissions are reduced, or token price falls, or unlocks hit.

Then the loop reverses. Capital doesn’t leave gradually. It stampedes. Liquidity dries up. Slippage spikes. Confidence evaporates. The protocol becomes collateral damage in its own token mechanics. Teams often respond by increasing emissions to stabilize price, which increases inflation, which drops price further, which triggers more exits. You cannot out-incentivize gravity forever.

Before a token launch, teams are forced to focus on product. They need users, retention and revenue. After a token launch, incentives shift in ways that are subtle but corrosive.

Founders and VCs often receive allocations. Unlock schedules begin ticking. The existence of a liquid token creates a parallel scoreboard. The pressure becomes price. Roadmaps get shaped around narrative catalysts rather than core utility. Governance proposals prioritize token holder appeasement rather than user experience. Instead of asking what makes the product better, the conversation becomes what supports token price.

Short-term token performance starts competing with long-term product integrity. And once liquidity exists, the temptation to extract becomes real. Early unlocks create selling pressure. Community trust erodes. Alignment fractures. The team that once moved fast on product features now moves fast on tokenomics. The product suffers accordingly.

Tokens don’t just change incentives. They change attention. Teams that were focused on shipping features now spend time managing tokenomics. They debate emissions schedules, argue about staking ratios. Also, navigate governance dram, they respond to price volatility, monitor unlock calendars. They become part-time market makers for their own narrative.

Meanwhile, competitors who never launched tokens keep building. Over time, the original product-market fit decays. The token becomes the product. And tokens are a far more volatile foundation than utility.

This is the quietest part of the DeFi token curse. It doesn’t announce itself. It arrives gradually, as priorities shift one Telegram message at a time, until one day the team realizes they haven’t shipped a meaningful feature in three months because they were too busy managing community sentiment about emissions.

There is a fourth, under-discussed dynamic that amplifies all three mechanisms: the structural conflict between token holders and actual users.

Users want low fees, high utility, and a stable experience. Token holders want buybacks, fee extraction, staking rewards, and reduced emissions. These goals are not always aligned. If you route more revenue to token holders, you increase fees for users, if you reduce emissions to preserve token value, you shrink the incentives that bootstrap adoption. If governance votes to maximize short-term yield, long-term sustainability suffers.

In traditional companies, shareholders and customers are separated by structure. In crypto, they collide. And governance token holders are often not users. They are traders. They vote based on token price expectations, not product excellence. That tension quietly erodes protocol quality over time, and most teams never see it coming until the damage is done.

Here is the uncomfortable twist. Some protocols are quietly thriving without tokens. They don’t make headlines, they don’t trend on crypto Twitter. Neither do they launch airdrops. They just generate fees. And they demonstrate exactly what escaping the DeFi token curse looks like.

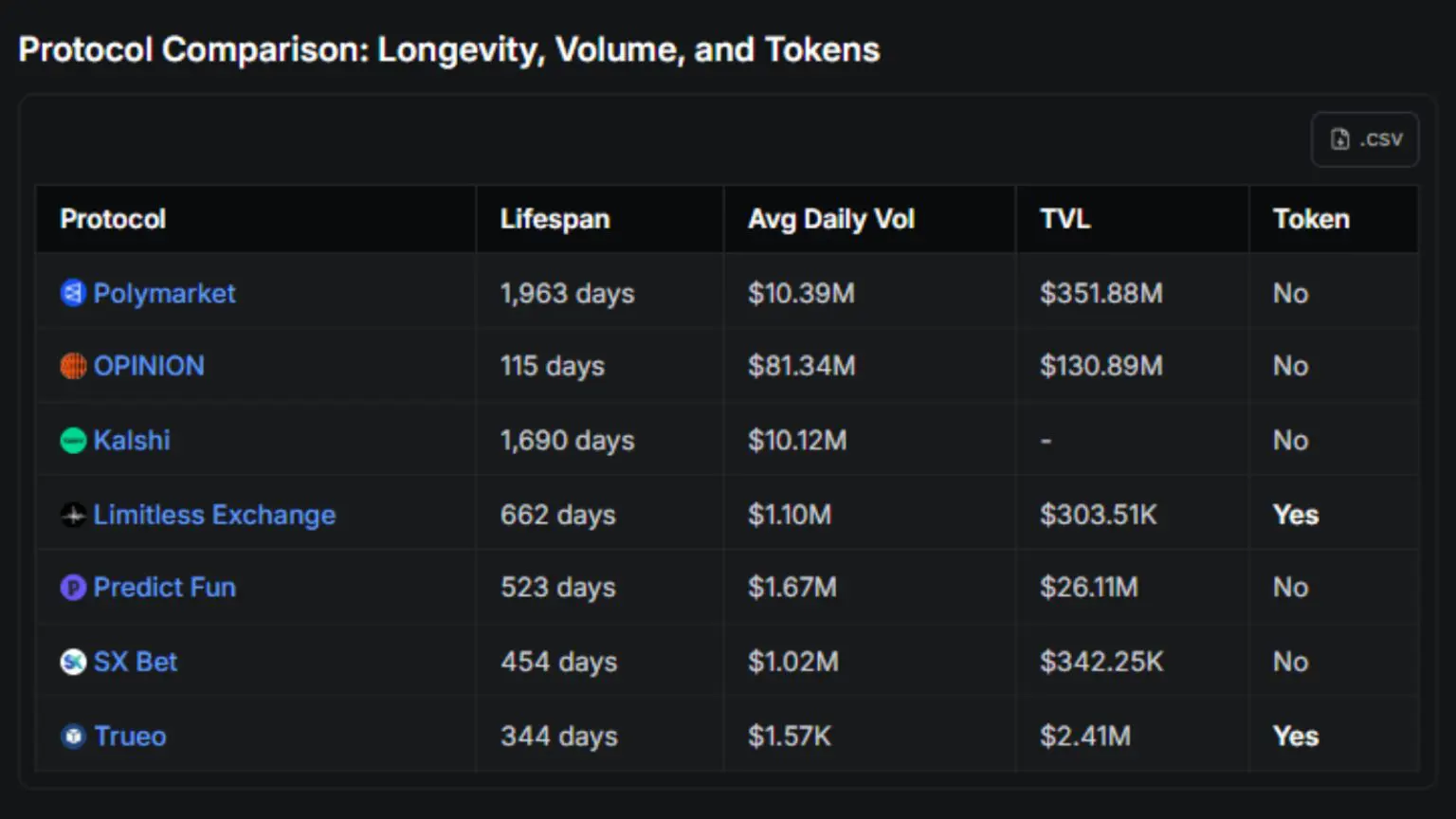

Take Polymarket. Nearly 2,000 days without a token. No emissions. No governance drama. Users come because it’s the best prediction market available. They are planning a token in 2026, but they built years of organic traction first. The token, if it launches, will follow proven demand rather than try to create it.

Or DeFi Saver. It sustained $249 million TVL for over 1,800 days without a token or emissions. Just a tool users genuinely need to manage leverage and risk. Or Gauntlet, curating $1.32 billion TVL across protocols by getting paid for risk management services, not by bribing liquidity. Or GMGN, generating over $5 million in monthly fees without ever launching a token, because it is a trading tool people use because it works.

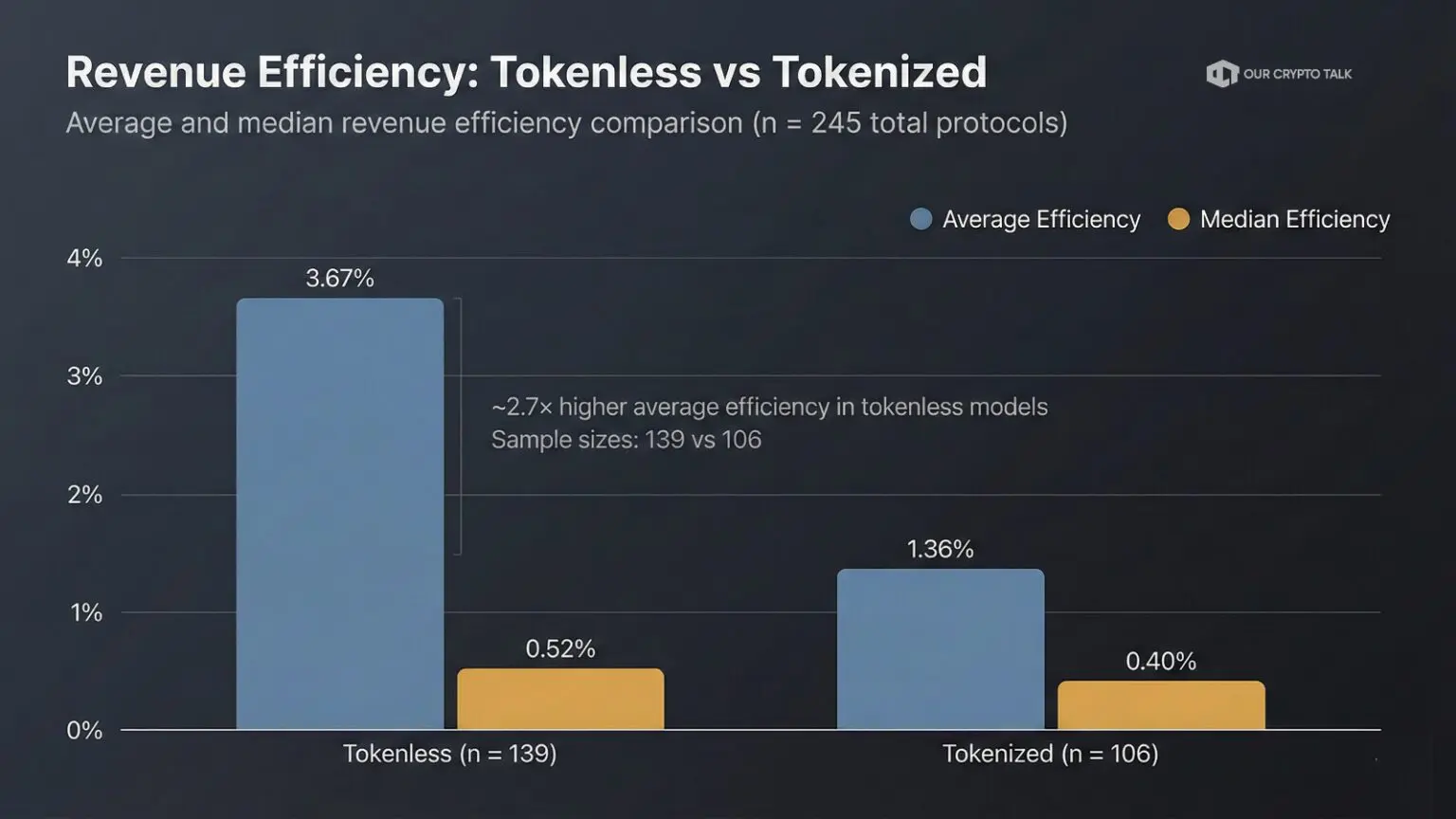

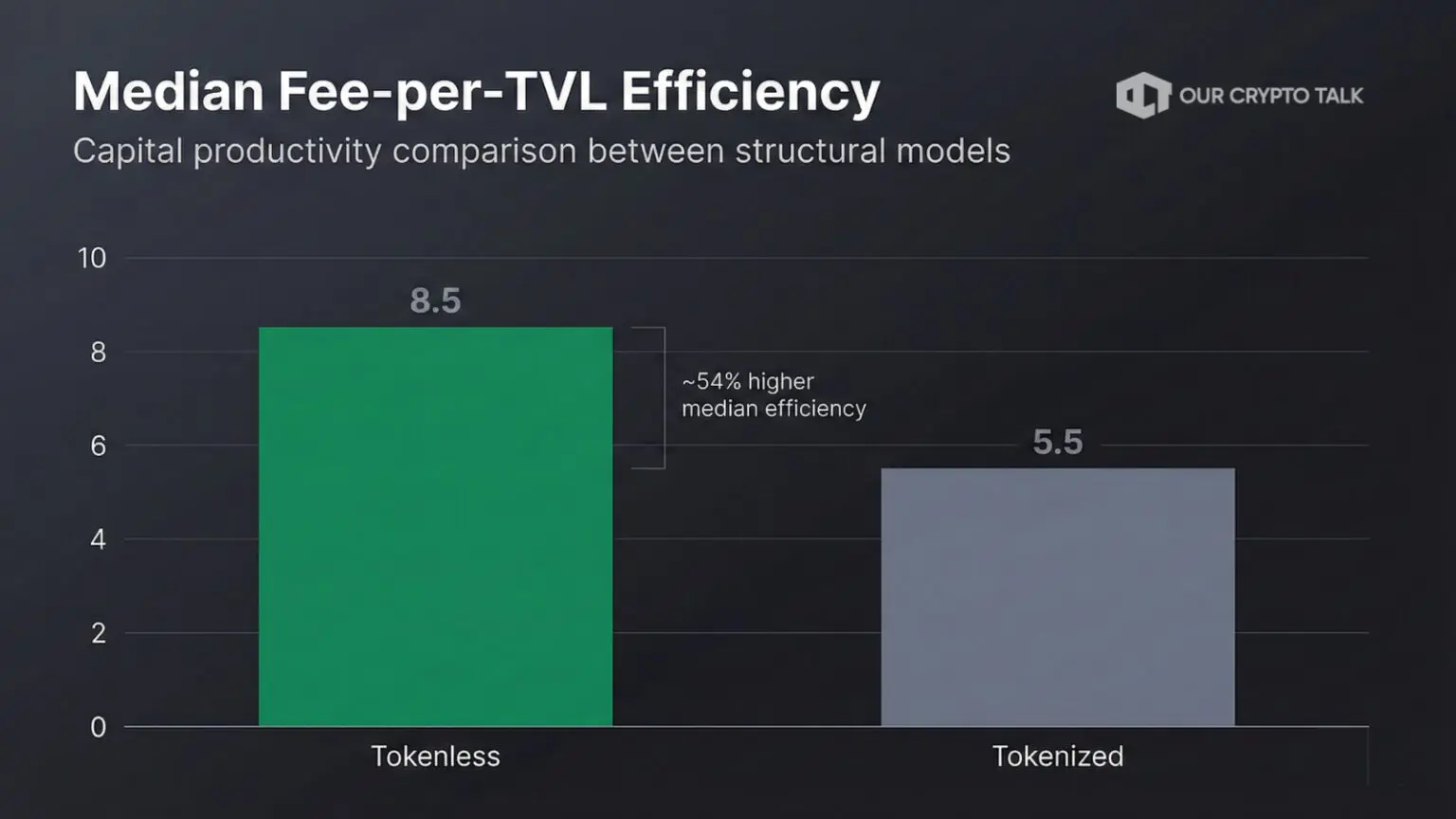

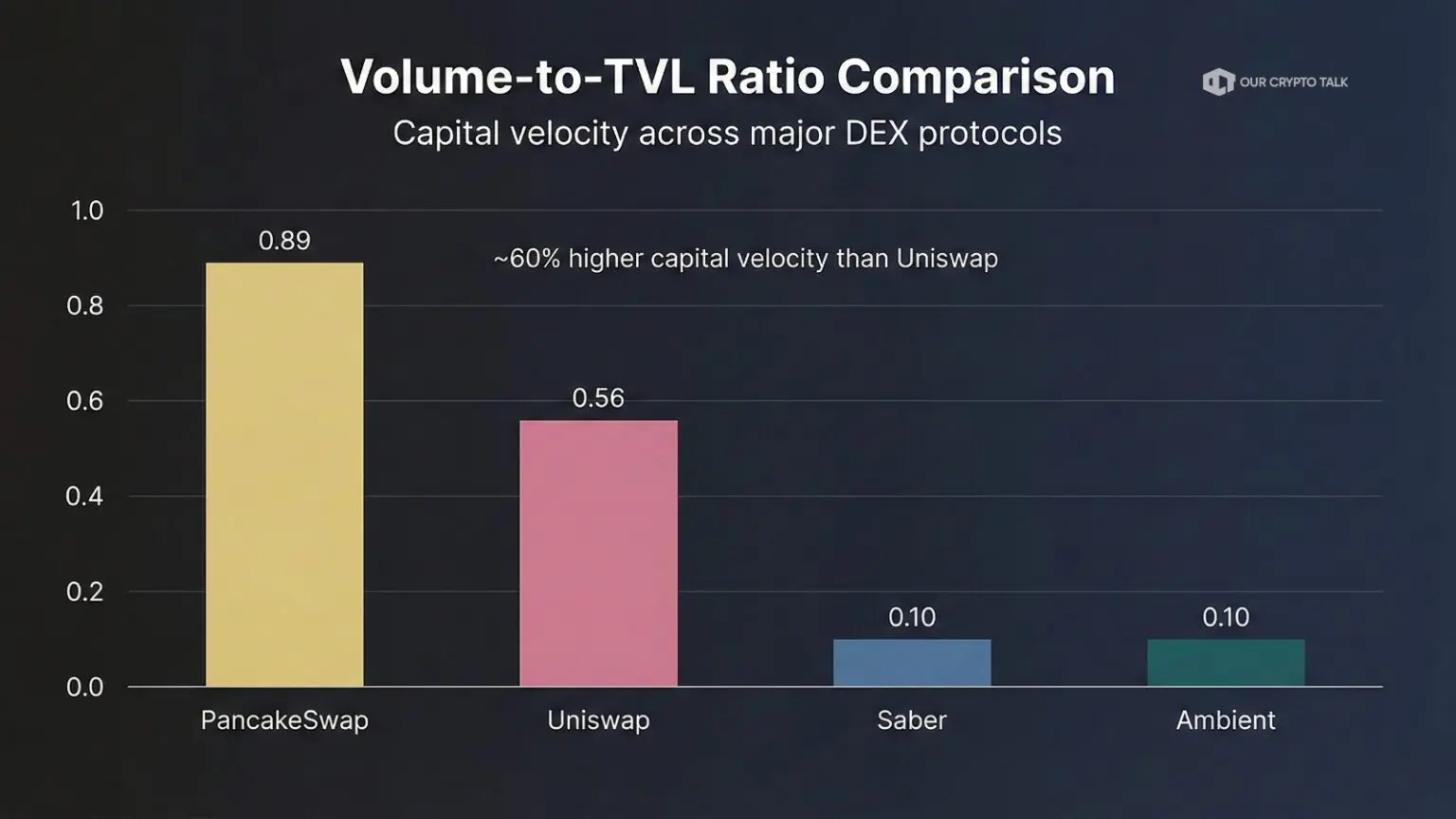

These protocols share critical traits that explain their longevity. First, they optimize for fee density over TVL vanity metrics. Tokenless protocols are 54 percent more capital-efficient, with a higher median fee-to-TVL ratio. Their capital is productive, not parked. Second, they maintain high Volume-to-TVL ratios, meaning capital is actually used, not just farmed. Third, they last five to ten times longer than tokenized protocols. They are built for decades, not quarters.

Most importantly, they never trained users to expect subsidies. They priced their service honestly from day one. Protocols that never emit tokens never face the addiction problem. And that gives them a compounding advantage: as tokenized competitors collapse, these protocols absorb their users. Organic survivors don’t just survive the DeFi token curse. They benefit from it.

If the data is this clear, why do founders still launch tokens? Why does every cycle repeat the same pattern? Because tokens solve founder problems far better than they solve product problems. And that distinction changes everything.

For most crypto founders, a token is not just infrastructure. It is a liquidity event. In traditional startups, liquidity comes years later through IPOs or acquisitions. In crypto, liquidity can arrive months after product launch. Raise seed. Ship MVP. Bootstrap traction. Launch token. List on exchanges. Unlock vesting. Suddenly there is a price. That price becomes validation, media coverage, and personal net worth, even if the protocol hasn’t proven long-term sustainability.

Tokens compress the startup lifecycle. Instead of building for ten years to earn liquidity, you can generate a liquid market within twelve months. The psychological shift is enormous. Before token launch: survival mode. After token launch: price-watching mode. And once there is a price, everything gets distorted.

The narrative dynamic makes it worse. Crypto is attention-driven. When your protocol launches a token, you enter the narrative arena. Token price becomes your public KPI. And token price rarely tracks fundamentals in the short term. It tracks attention. That creates a dangerous incentive loop where narrative always wins faster than product iteration. So teams allocate attention accordingly. Slowly, the product becomes secondary. And the DeFi token curse tightens its grip.

Once you start emitting tokens to attract liquidity, stopping becomes extremely difficult. High APYs attract capital. Capital inflates TVL. TVL validates token value. Token value justifies emissions. The loop feeds itself. But emissions are inflation. At some point, the market realizes that rewards exceed organic demand. Price drops. To compensate, protocols increase emissions, which increases inflation, which drops price further.

Users trained to expect subsidies treat emission cuts as betrayal. Community members who joined for yield become hostile the moment that yield shrinks. The team faces an impossible choice: reduce emissions and watch capital flee, or maintain emissions and accelerate the death spiral. There is no clean exit from this trap. The only winning move is not to enter it.

This is not an argument that tokens are universally bad. It is an argument that premature tokens are lethal. The DeFi token curse strikes hardest when tokens are launched to satisfy narrative expectations rather than solve genuine coordination problems.

Tokens make sense when the protocol is already revenue-generating and stable. When the token has a clear, unavoidable role in system security or coordination, such as aligning validators, incentivizing security, or distributing ownership across contributors and when emissions are minimal or non-existent. Also, when governance is genuinely necessary and meaningful. When team incentives are aligned long-term, not front-loaded.

In other words, tokens should be infrastructure. Not marketing. They should emerge after product-market fit is deeply established, not as a shortcut to it. The protocols that will safely launch tokens in the next cycle are exactly the ones that don’t need them right now. Because they have something more valuable than a token. They have a working product with paying users.

Before launching a token, every founder should sit with three questions. First: are we solving a coordination problem, or creating a liquidity event? Second: are users paying us because the product works, or because emissions are attractive? Third: would our protocol survive if the token went to zero tomorrow?

If the answer to that last question is no, you do not have product-market fit. You have token-market fit. And token-market fit is fragile. It evaporates the moment a better farm appears, or the moment macro conditions tighten, or the moment unlock pressure hits. It provides the illusion of traction without the foundation of genuine utility.

The DeFi token curse is not inevitable. But it requires intentionality to avoid. It requires founders who are honest enough to distinguish between what serves their protocol and what serves their personal liquidity. That distinction is rarer in crypto than it should be.

Every cycle in DeFi delivers the same lesson in a new costume. Build product. Get traction. Launch token. Watch metrics inflate, watch capital flee and watch team fracture. Read the post-mortem.

The DeFi token curse persists not because founders are reckless, but because the structural incentives of tokenization genuinely reward short-term extraction over long-term building. The playbook looks rational at every individual step. The outcome is irrational in aggregate.

The market is slowly learning. Capital is becoming more selective. Investors are starting to look at fee sustainability, emission schedules, unlock timelines, and real usage metrics before deploying. The era of blind token launches as default growth strategy is fading. Projects that demonstrate revenue without inflation will command higher trust. And ironically, those might be the only projects that can safely launch tokens later, because they will not need them.

Crypto loves to believe that tokens are empowerment. Sometimes they are. But more often, they are accelerants. Accelerants make things grow fast. They also make things burn fast. If you already built something people love, protect it. Because the data is clear. In DeFi, the token is not the finish line. It is often the fuse.

What Happens When All 21 Million Bitcoins Are Mined? A Beginner’s Guide

Why Does The Ethereum Foundation Keep Selling ETH?

The CLARITY Act Explained: What It Means for Your Crypto

Meta To Onboard 3.6 Billion Users Onto Web3

What Happens When All 21 Million Bitcoins Are Mined? A Beginner’s Guide

Why Does The Ethereum Foundation Keep Selling ETH?

The CLARITY Act Explained: What It Means for Your Crypto

Meta To Onboard 3.6 Billion Users Onto Web3