Loading Search...

A deep dive into the Top 7 Crypto Payment Projects powering real-world blockchain payments, stablecoin transfers, and global finance.

Author: Akshat Thakur

In the rapidly evolving landscape of digital finance, crypto payment protocols have emerged as powerful tools that bridge traditional financial systems with decentralized blockchain infrastructure. These protocols are not simply digital currencies. They represent structured frameworks that enable secure, borderless, and efficient value transfers without relying on centralized intermediaries such as banks or payment processors. The top 7 crypto payment projects highlighted in this guide demonstrate how decentralized networks can enable fast, secure, and borderless financial transactions without relying on traditional intermediaries such as banks or payment processors.

As global financial systems increasingly explore decentralized alternatives, understanding the mechanics and advantages of crypto payment solutions has become essential for businesses, developers, and everyday users. The concept of digital payments built on blockchain technology began with Bitcoin in 2009, which introduced peer-to-peer electronic cash. Since then, the ecosystem has expanded significantly, with numerous networks and protocols designed to improve transaction efficiency, scalability, and accessibility. Modern crypto payment protocols address critical limitations of early blockchain systems, including slow confirmation times, high fees, and limited throughput.

Through innovations such as smart contracts, layer-2 scaling technologies, and cross-chain interoperability, these systems aim to deliver payment experiences comparable to traditional financial services. Adoption has accelerated rapidly. Recent estimates suggest that more than 420 million people worldwide now use cryptocurrencies. As this user base expands, the demand for reliable payment infrastructure continues to grow. Crypto payment protocols can reduce transaction costs to fractions of a cent, compared with traditional payment networks that often charge merchants between two and three percent per transaction. As blockchain adoption continues to expand, the Top 7 Crypto Payment Projects discussed in this guide highlight how decentralized infrastructure is evolving to support faster, more efficient, and globally accessible digital payment systems.

This article explores the foundations of crypto payment protocols and the core features that define the most effective solutions. By understanding how these systems operate and what distinguishes leading protocols, readers can better evaluate their potential role in the future of digital commerce. This article explores the top crypto payment projects shaping the future of digital transactions and examines the technologies that enable them to operate efficiently at global scale.

Crypto payment protocols define the rules and mechanisms that enable transactions on blockchain networks. They determine how payments are initiated, verified, recorded, and finalized across decentralized systems. Unlike traditional financial infrastructure, where banks and payment processors act as intermediaries, crypto protocols rely on distributed networks of nodes that collectively validate transactions.

At a technical level, these systems operate on blockchain ledgers. Each block contains a set of verified transactions that are cryptographically linked to the previous block, creating an immutable transaction history. When a payment is initiated, it is broadcast to the network where nodes verify that the sender has sufficient balance and that the transaction complies with protocol rules. Once validated, the transaction becomes part of the next block added to the chain.

Early crypto payment protocols relied primarily on proof-of-work consensus systems. In these networks, miners compete to solve complex cryptographic puzzles to validate transactions and secure the blockchain. While highly secure, this model introduced scalability limitations and high energy consumption. Bitcoin, for example, processes only a limited number of transactions per second.

Later innovations introduced proof-of-stake consensus mechanisms, where validators secure the network by staking cryptocurrency instead of performing energy-intensive computations. This significantly reduces power consumption and improves network efficiency. Many modern payment protocols now adopt proof-of-stake or hybrid consensus models to balance security, scalability, and decentralization.

To improve transaction capacity, many networks also incorporate layered architectures. Layer-1 refers to the base blockchain itself, while layer-2 solutions operate on top of the main chain to process transactions more efficiently. Techniques such as rollups and sidechains bundle multiple transactions together before submitting them to the base layer, reducing congestion and lowering fees.

Security remains a core component of crypto payment protocols. Transactions are authorized using public-key cryptography, where private keys generate digital signatures that prove ownership of funds. Additional mechanisms such as multi-signature wallets and zero-knowledge proofs enhance security and privacy while maintaining transparency on the blockchain.

From a user perspective, interaction with payment protocols occurs through crypto wallets. These wallets manage private keys and allow users to send, receive, and store digital assets. Payment gateways and merchant integrations further extend these systems into e-commerce and retail environments, enabling businesses to accept cryptocurrency payments in real-world transactions.

Despite their advantages, crypto payment protocols must address several ongoing challenges. Network congestion can lead to rising fees during periods of high demand. Price volatility may discourage merchants from accepting cryptocurrency directly, leading to the growing use of stablecoins. Regulatory frameworks across different jurisdictions also continue to evolve.

Even with these challenges, crypto payment protocols have demonstrated clear advantages in areas such as cross-border remittances, decentralized finance, and digital commerce. By enabling faster settlement, lower fees, and global accessibility, they represent a significant shift in how value can move across digital networks.

The effectiveness of a crypto payment protocol depends on several core features that determine whether it can support large-scale adoption. Leading payment networks are designed to balance security, speed, cost efficiency, and user accessibility while maintaining the decentralized nature of blockchain technology. These attributes are what separate experimental payment networks from solutions capable of handling real-world financial transactions.

Below are the most important characteristics that define top crypto payment protocols.

Security is the foundation of any financial system, and crypto payment protocols must ensure that transactions cannot be altered or manipulated. Modern networks rely on advanced cryptographic techniques and extensive auditing to maintain trust.

Key security mechanisms include:

Strong security architecture is essential for protecting both users and merchants in decentralized payment systems.

Scalability determines how well a payment protocol can handle increasing transaction demand. Early blockchains struggled with limited throughput, but modern solutions introduce architectural improvements to support large user bases.

Common scalability solutions include:

These innovations allow payment networks to process thousands of transactions without overwhelming the base blockchain.

For payment systems to compete with traditional financial infrastructure, transaction confirmation must be fast and reliable. Many modern crypto protocols reduce settlement times significantly compared to early blockchain networks.

Key mechanisms that improve speed include:

Faster confirmations make crypto payments viable for everyday use cases such as retail transactions and online purchases.

Lower transaction fees are one of the main advantages of blockchain payments compared with traditional systems. Many protocols focus on minimizing costs so that micro-transactions and global transfers remain practical.

Cost-reducing strategies include:

These features allow payments to occur at significantly lower costs than conventional payment processors.

As the blockchain ecosystem expands, the ability for different networks to communicate with one another becomes increasingly important. Interoperability ensures that assets and payments can move seamlessly between blockchains.

Important interoperability tools include:

These mechanisms allow payment systems to function across a broader decentralized ecosystem.

While blockchains are transparent by design, advanced payment protocols often include optional privacy tools that protect sensitive financial data.

Common privacy features include:

These technologies help balance privacy with regulatory compliance.

For crypto payment systems to achieve widespread adoption, they must be easy to use for both consumers and businesses. Intuitive design and simple integration are therefore essential.

User-focused improvements include:

A seamless user experience significantly lowers the barrier to entry for new users.

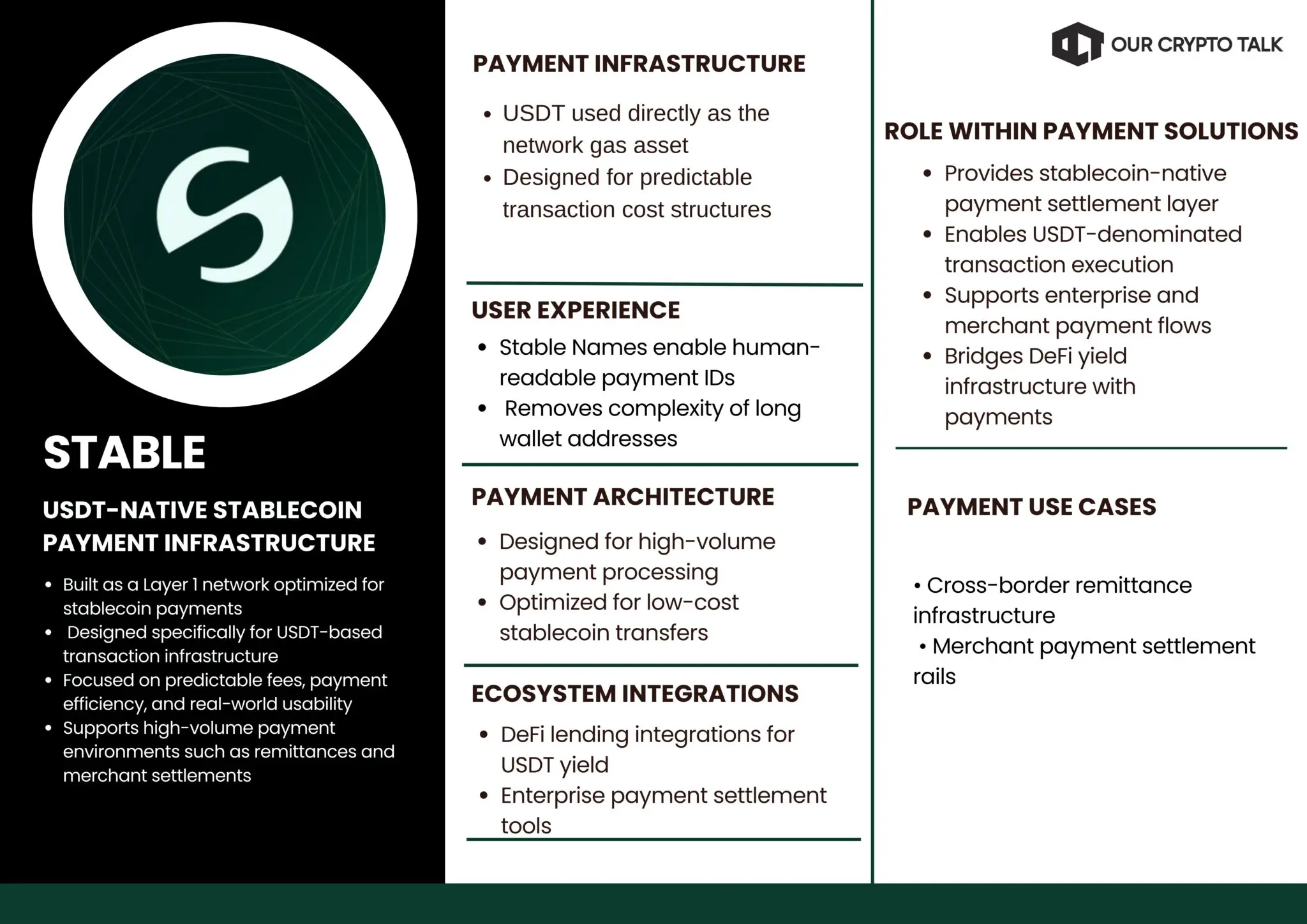

Stable ($STABLE) is a Layer 1 blockchain protocol designed specifically for stablecoin payments, with a primary focus on USD₮ (USDT). Among the top crypto payment projects, Stable focuses on creating infrastructure optimized for USDT-based transactions. Unlike general-purpose blockchains that support a wide range of decentralized applications, Stable is built as dedicated infrastructure for stablecoin-based transactions. The project aims to address persistent limitations in existing stablecoin ecosystems, including unpredictable transaction fees, congestion during high demand, and the need to hold volatile native tokens to pay for gas.

At the core of the protocol is the concept of a USDT-native payment network. Transactions on StableChain use USDT directly as the gas asset, eliminating the requirement for users to maintain separate tokens to execute transfers. This approach simplifies the payment process and improves cost predictability, particularly for businesses that rely on stable transaction expenses. By removing the dependency on volatile native tokens, Stable positions itself as infrastructure optimized for real-world financial usage rather than speculative activity.

Stable’s architecture is designed to support high transaction throughput and low-cost transfers, making it suitable for high-volume payment use cases such as remittances, merchant settlements, and microtransactions. In traditional blockchain networks, transaction fees can fluctuate significantly during periods of congestion. Stable attempts to address this issue by maintaining predictable fee structures that remain low even during increased network activity.

A key component of the ecosystem is Stable Pay, a non-custodial payment application built on top of StableChain. The application enables users to send and receive payments using human-readable identifiers known as Stable Names instead of complex wallet addresses. This simplifies the user experience and reduces the risk of sending funds to incorrect addresses. Transactions are designed to settle quickly, improving usability for everyday payments.

Stable also integrates financial utility beyond payments by allowing users to earn yield on USDT balances through DeFi integrations. Partnerships with lending networks enable users to deposit stablecoins while maintaining access to the payment infrastructure. This creates a hybrid model where users can simultaneously store value, earn yield, and perform transactions without leaving the ecosystem.

For businesses, the protocol offers enterprise payment tools that enable automated settlements, transaction monitoring, and compliance features aligned with global financial regulations. These capabilities are particularly relevant for companies exploring blockchain-based payment rails for cross-border operations.

Stable’s primary focus is enabling stablecoins to function as efficient digital payment rails rather than simply acting as reserve assets within trading ecosystems. If adoption continues to grow, infrastructure built specifically around stablecoin transactions could play an important role in expanding real-world crypto payments.

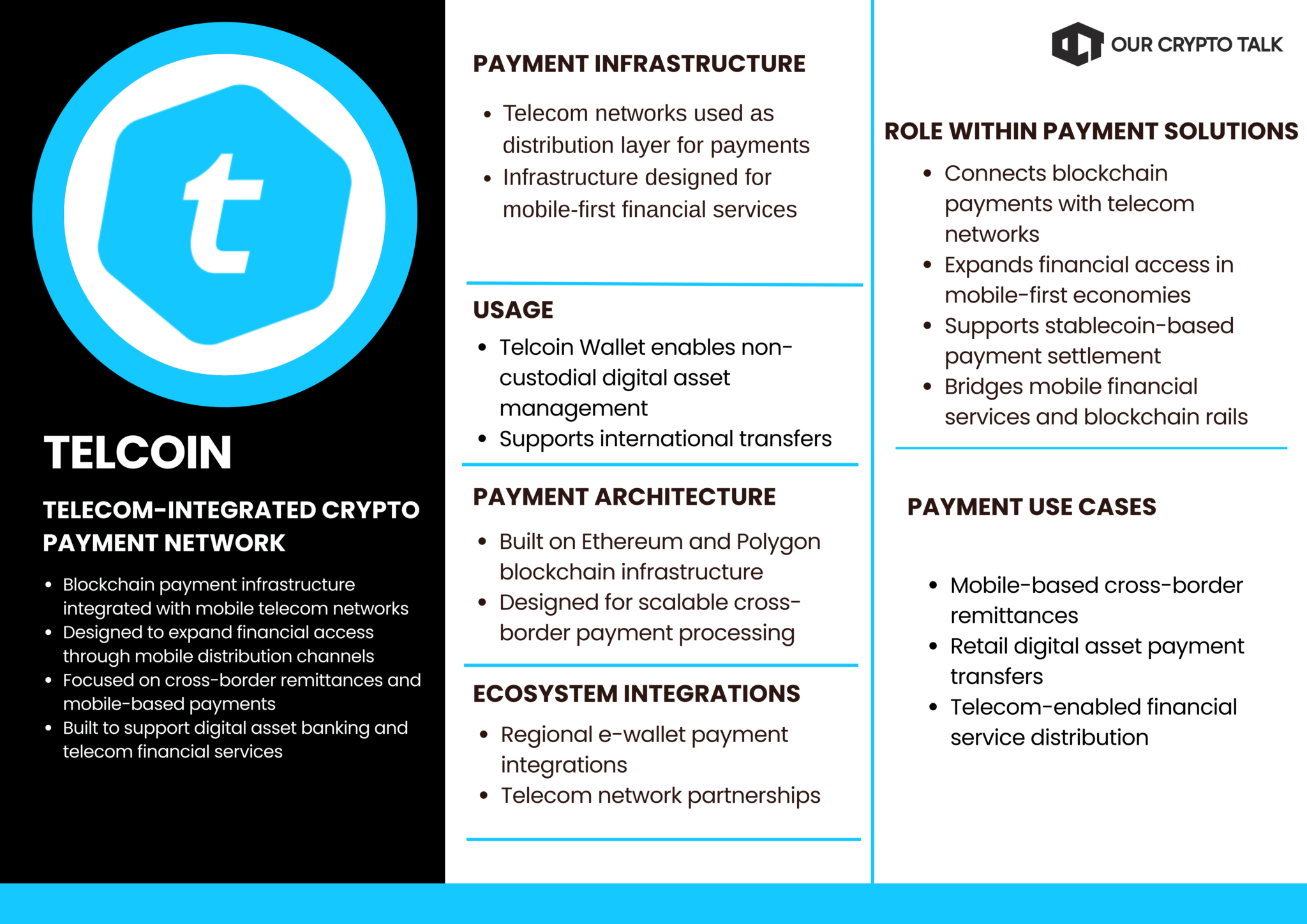

Telcoin ($TEL) represents another approach among the Top 7 Crypto Payment Projects, focusing on integrating blockchain payments with global telecommunications networks. Founded in 2017, the project initially focused on cross-border remittances and later expanded into a broader digital asset banking ecosystem.

The core concept behind Telcoin is to use mobile network infrastructure as a distribution layer for blockchain-based financial services. In many regions, particularly in developing economies, mobile phone adoption significantly exceeds access to traditional banking services. By integrating blockchain payments with telecom networks, Telcoin aims to provide digital financial services to populations that remain underserved by conventional financial institutions.

Telcoin originally launched on Ethereum but later expanded to Polygon to improve transaction scalability and reduce fees. This transition allowed the platform to support faster transactions and lower costs, which are essential for remittance use cases where small fee differences can significantly impact users sending money across borders.

A central component of the ecosystem is the Telcoin Wallet, a non-custodial application that allows users to store digital assets and send payments internationally. Through integrations with local payment providers and e-wallet platforms, the wallet supports transfers to multiple countries and payment networks. This approach allows recipients to receive funds through familiar local services rather than requiring direct interaction with blockchain infrastructure.

Telcoin has also introduced eUSD, a stablecoin designed for retail payments and remittances. Stablecoins play a critical role in payment ecosystems because they reduce volatility, making digital assets more practical for everyday financial transactions. eUSD is backed by reserves and is intended to function as a stable settlement asset within Telcoin’s payment network.

A notable development for the project was the approval of Telcoin Digital Asset Bank under Nebraska’s Financial Innovation Act. This regulatory framework allows Telcoin to operate as a compliant digital asset bank capable of issuing stablecoins, processing payments, and holding deposits within a regulated structure.

Telcoin’s strategy focuses on connecting blockchain payments with mobile financial services. By leveraging telecom networks as distribution channels, the platform attempts to expand access to digital payments in regions where traditional banking infrastructure remains limited.

Zebec Network ($ZBCN) is a blockchain-based financial infrastructure platform focused on programmable payment streaming and real-time payroll solutions. Originally launched in 2021 on the Solana blockchain, Zebec later expanded into a multi-chain ecosystem supporting multiple assets and networks. Within the Top 7 Crypto Payment Projects, Zebec Network ($ZBCN) stands out for introducing programmable payment streaming and real-time payroll infrastructure.

Traditional payment systems typically operate on batch-based settlement models. Salaries, subscriptions, and vendor payments are often processed at fixed intervals such as weekly or monthly. Zebec introduces a different approach through continuous payment streaming, where funds can be distributed in real time rather than in periodic batches. This model enables payments to be streamed per second, allowing recipients to access earnings as they accumulate.

The protocol’s core infrastructure enables businesses, decentralized organizations, and Web3 companies to automate recurring payments using programmable smart contracts. Instead of waiting for scheduled payouts, workers can receive compensation continuously, improving liquidity and financial flexibility.

One of the primary applications of this model is crypto payroll infrastructure. Companies using Zebec can distribute salaries in stablecoins or other supported assets across multiple blockchains. The platform currently supports various tokens and networks, allowing organizations to manage payroll without relying on centralized payment processors.

Zebec has also expanded into consumer-facing financial services. The platform introduced Zebec Cards, debit cards powered by Mastercard that allow users to spend cryptocurrency globally. These cards enable real-time conversion from crypto assets to fiat currencies, allowing users to make purchases through traditional payment networks while maintaining crypto balances.

Another component of the ecosystem is the Zebec Super App, a financial management application designed to integrate on-chain payments with everyday financial tools. This application allows users to manage assets, stream payments, and spend funds through integrated card systems.

By enabling continuous payment flows and programmable payroll systems, Zebec introduces a different model for digital payments that moves beyond traditional periodic settlement structures.

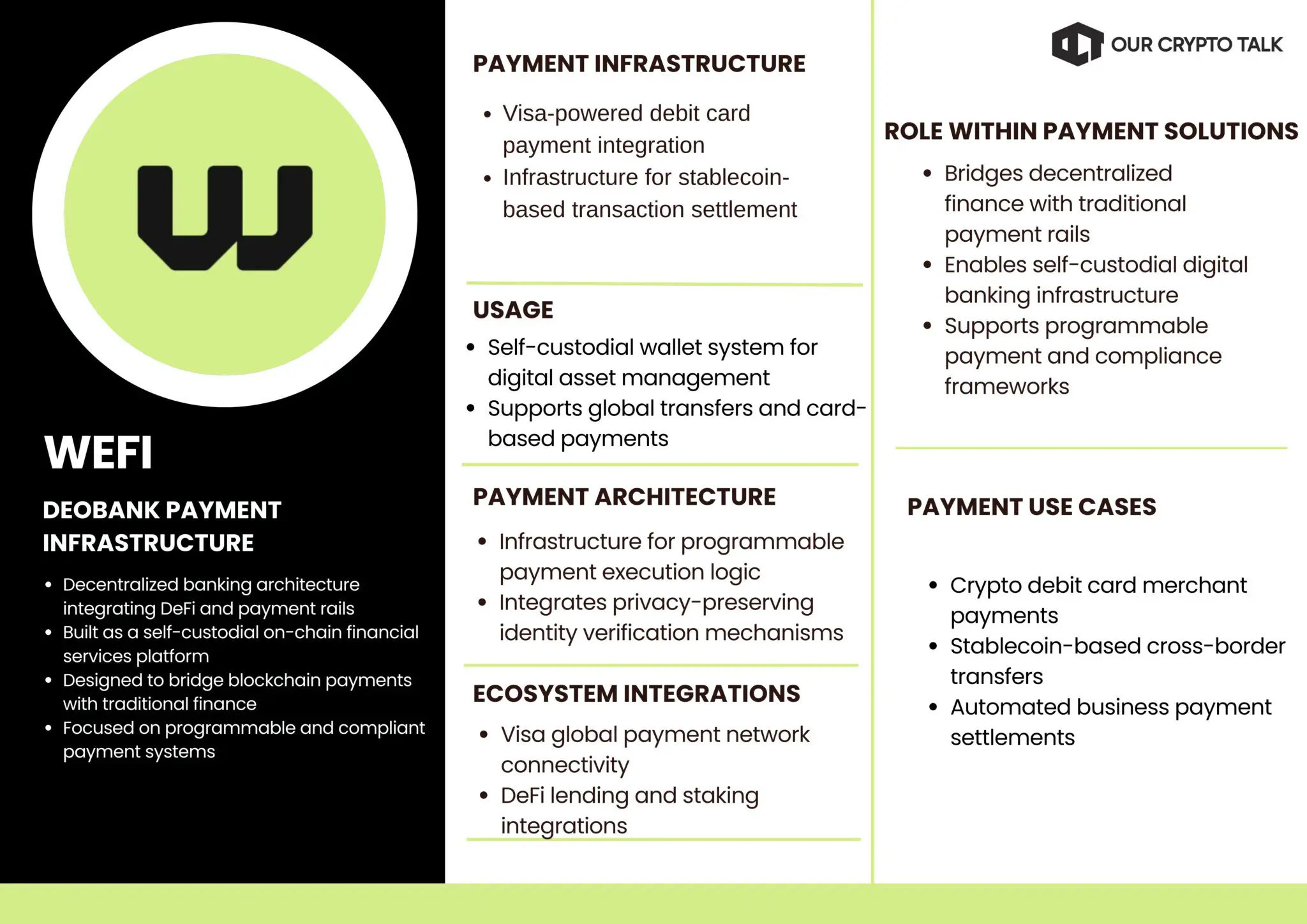

WeFi ($WFI) is one of the Top 7 Crypto Payment Projects designed to merge decentralized finance with traditional payment systems. Launched in 2024, the project positions itself as a decentralized on-chain banking system, sometimes referred to as a “deobank.” Its architecture focuses on providing self-custodial financial services that integrate cryptocurrency wallets, payment cards, global transfers, and yield-generating accounts within a single ecosystem.

Unlike many crypto payment platforms that operate purely within decentralized networks, WeFi attempts to bridge DeFi with existing financial systems. The platform uses a permissioned blockchain framework that prioritizes regulatory compliance while maintaining user-controlled custody of assets. This hybrid design allows the platform to support financial services typically associated with traditional banking while preserving the transparency and programmability of blockchain systems.

One of the core elements of the ecosystem is the WeFi Card, a Visa-powered debit card that enables users to spend cryptocurrency directly through global payment networks. The card can be issued in both virtual and physical formats and connects to users’ self-custodial wallets. Rather than converting assets into fiat in advance, the system performs conversion at the moment of purchase. This structure allows users to retain custody of digital assets until the transaction occurs while minimizing exposure to exchange rate fluctuations.

The platform also focuses on enabling cross-border transfers through stablecoin payments. By using blockchain settlement rather than traditional banking rails, transfers can be processed quickly with lower transaction costs. For businesses, WeFi offers payment tools that include automated settlements, transaction monitoring, and compliance modules designed to align with regulatory requirements such as anti-money laundering (AML) and identity verification frameworks.

Technologically, WeFi incorporates programmable payment infrastructure that allows assets to be converted and transferred automatically based on predefined conditions. The system also integrates privacy-preserving verification tools, including zero-knowledge based identity mechanisms that enable compliance checks without exposing sensitive user data.

Beyond payments, WeFi integrates decentralized finance services such as lending and staking, allowing users to generate yield on stablecoin balances held within the ecosystem. This structure merges payments with asset management by enabling funds stored for transactions to also participate in on-chain financial activity.

By combining traditional payment infrastructure with decentralized asset custody, WeFi aims to provide a banking-style experience while maintaining blockchain-based financial control.

Keeta Network ($KTA) appears among the Top 7 Crypto Payment Projects as a blockchain designed to connect traditional financial systems with decentralized settlement networks. Launched in 2025, the project focuses on addressing inefficiencies in cross-border payments, asset transfers, and financial settlement processes by providing a blockchain-based payment layer capable of interacting with both crypto and conventional banking systems.

The network architecture emphasizes interoperability between financial environments. Rather than focusing exclusively on decentralized applications, Keeta’s design centers on enabling financial institutions, payment providers, and blockchain platforms to exchange assets within a unified settlement framework. This approach targets a longstanding limitation in the crypto ecosystem, where payment networks often operate in isolation from traditional banking infrastructure.

One of the network’s core features is its Anchor mechanism, which allows institutions to tokenize external assets and represent them on-chain. Through this mechanism, issuers can create fiat-backed stablecoins or other financial instruments on Keeta with a one-to-one backing structure. These tokenized assets can then move across blockchain networks, or users can exchange them through atomic transactions without relying on centralized intermediaries.

Keeta also focuses heavily on compliance infrastructure. Many blockchain payment networks struggle to integrate regulatory requirements while maintaining decentralization. Keeta incorporates identity verification frameworks, traceable asset issuance, and permissioned financial gateways designed to enable regulated institutions to interact with blockchain settlement systems.

The ecosystem includes a non-custodial wallet that supports asset storage, cross-chain transfers, and fiat on/off ramps through partner integrations. Planned financial tools include merchant payment systems, card-based spending products, and decentralized exchanges that enable asset conversion within the network.

Another key component of Keeta’s design is its role in real-world asset tokenization. By allowing traditional assets to be issued and transferred on-chain, the network supports financial use cases such as cross-border settlements, tokenized securities, and programmable payment flows.

Keeta’s strategy focuses on positioning blockchain technology as a settlement layer for global financial systems rather than simply a decentralized transaction network.

Avici Money ($AVICI) is included in the Top 7 Crypto Payment Projects due to its focus on crypto-backed spending tools and digital banking services. Built on the Solana network, the platform combines self-custodial wallet infrastructure with payment cards, lending features, and on-chain asset management. Its objective is to allow users to access traditional financial services while maintaining direct control of their cryptocurrency holdings.

A central feature of the platform is the Avici Card, a Visa-powered debit and credit card that allows users to spend cryptocurrency at global merchants. The card connects to non-custodial wallets, meaning users retain control of their assets until a transaction occurs. Instead of selling assets in advance, the system converts cryptocurrency to fiat currency during payment execution.

The platform also introduces a borrowing model where users can access credit lines backed by their cryptocurrency holdings. By depositing assets as collateral, users can obtain spending power without liquidating their holdings. This model plays a key role in decentralized finance, allowing users to maintain exposure to underlying assets while accessing liquidity.

Avici integrates this functionality with payment infrastructure, allowing users to spend borrowed funds through the card network. The system can support digital wallet payments through mobile platforms such as Apple Pay and Google Pay, as well as physical card transactions through existing merchant networks.

The platform’s application integrates multiple financial functions, including asset storage, swaps, transfers, and payment management. Fiat on-ramps allow users to convert traditional currency into cryptocurrency, while named accounts support transfers through payment systems such as ACH or SEPA.

Avici also supports peer-to-peer transfers between users, allowing digital assets to move directly between wallets without centralized intermediaries. This feature can support remittances, merchant payments, and personal transfers while maintaining self-custody.

By combining lending, wallet infrastructure, and card-based spending, Avici Money attempts to replicate traditional banking functionality within a decentralized asset environment.

Concordium ($CCD) rounds out the Top 7 Crypto Payment Projects with a payment infrastructure built around regulatory compliance and identity verification. Unlike many blockchain networks that prioritize anonymity, Concordium integrates a native identity layer directly into the protocol. This allows users and institutions to verify identity attributes while still preserving privacy, enabling financial services that meet regulatory requirements without relying on external identity providers.

The network’s architecture supports real-world financial use cases where compliance and accountability are critical. Through its identity framework, users can prove attributes such as age, residency, or regulatory eligibility using zero-knowledge proofs. These cryptographic mechanisms allow verification of specific data points without revealing the underlying personal information, creating a balance between transparency and privacy.

Concordium positions its infrastructure within the emerging “PayFi” category, which combines payment functionality with programmable financial services. The platform supports stablecoin transactions and programmable payments that developers can embed into decentralized applications or financial workflows. Its payment infrastructure aims to reduce reliance on centralized processors by enabling direct blockchain-based settlement for merchants and financial institutions.

A key component of this system is Concordium Pay, a payment framework designed to enable stablecoin transactions with predictable costs and fast settlement times. Transactions are processed within seconds, and fees are paid in the native $CCD token. To maintain cost stability, the protocol dynamically adjusts fees relative to token price fluctuations, ensuring predictable transaction costs for users and businesses.

The platform also supports programmable financial flows. Payments can be scheduled, automated, or executed based on predefined conditions within smart contracts. These capabilities enable applications such as automated payroll, subscription services, compliance-controlled payments, and tokenized real-world asset settlements.

By embedding identity and compliance directly into the blockchain protocol, Concordium attempts to address a key barrier to institutional adoption of crypto payments. Its infrastructure is designed to support payment systems that combine regulatory alignment with the efficiency of decentralized settlement.

The payment protocols explored throughout this article demonstrate how blockchain infrastructure is evolving beyond simple peer-to-peer transfers into full financial ecosystems. Projects such as Stable, Telcoin, Zebec Network, WeFi, Keeta Network, Avici Money, and Concordium approach the payments challenge from different angles, yet they share a common goal: building scalable, efficient systems that can support real-world financial activity. The Top 7 Crypto Payment Projects explored in this article demonstrate how blockchain infrastructure is evolving beyond simple peer-to-peer transfers into full financial ecosystems.

Some networks focus on stablecoin infrastructure to enable predictable and low-cost global transfers. Others concentrate on remittances, programmable payroll systems, or integrated banking services that combine decentralized finance with traditional payment tools. Meanwhile, platforms like Concordium emphasize regulatory alignment and identity verification to make blockchain payments more suitable for institutional adoption.

These approaches highlight a broader shift in the crypto industry toward practical financial infrastructure. Payment protocols are increasingly designed to support everyday use cases such as merchant transactions, cross-border remittances, and automated financial flows. Innovations in programmable payments, stablecoin settlement, and interoperable networks are helping address long-standing challenges in global finance, including high transaction costs and slow settlement times.

However, the path toward mainstream adoption still involves important challenges. Regulatory frameworks continue to evolve, stablecoin governance remains under scrutiny, and user experience must improve to match traditional payment platforms. Addressing these issues will determine whether blockchain payment systems can scale beyond niche crypto markets.

As adoption continues to expand, the top 7 crypto payment projects featured here highlight the different approaches developers are taking to build scalable, secure, and accessible payment systems. Despite these challenges, the continued development of specialized payment protocols signals a growing focus on real-world utility. As infrastructure improves and integration with traditional financial systems expands, blockchain-based payments may increasingly become part of the broader digital financial landscape.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.