Loading Search...

Guide to perpDEX platforms, covering perpetual trading basics, top exchanges, key metrics, and major risks.

Author: Chirag Sharma

Crypto markets have always been driven by speculation, leverage, and volatility. Over time, the tools traders use to express these views have evolved. One of the most important outcomes of that evolution is the rise of the perpDEX.

In 2026, perpDEX platforms routinely process tens of billions of dollars in daily trading volume during periods of high volatility. This growth is not accidental. It reflects a structural shift away from centralized exchanges and toward self-custodial, on-chain trading systems.

The collapse of major centralized players like FTX exposed a fundamental weakness in crypto markets: counterparty risk. Traders could be correct on direction yet still lose funds due to exchange insolvency or misuse of customer deposits. PerpDEX platforms directly address this issue by using smart contracts to ensure non-custodial execution. Users retain control of their funds at all times.

Beyond security, perpDEXs offer global access. Anyone with a wallet can open leveraged long or short positions on assets like Bitcoin or Ethereum without KYC, geographic restrictions, or banking dependencies. This open access has attracted both retail traders seeking opportunity and professional traders seeking efficiency.

However, perpDEXs are not simply copies of centralized derivatives platforms. They introduce new trade-offs, including oracle dependency, liquidation mechanics, and funding-rate dynamics that require deeper understanding.

This article breaks down perpDEX from the ground up. It explains what it is, how it works, how it evolved, and how to evaluate platforms properly. For anyone serious about crypto trading or DeFi infrastructure, understanding perpDEX is no longer optional.

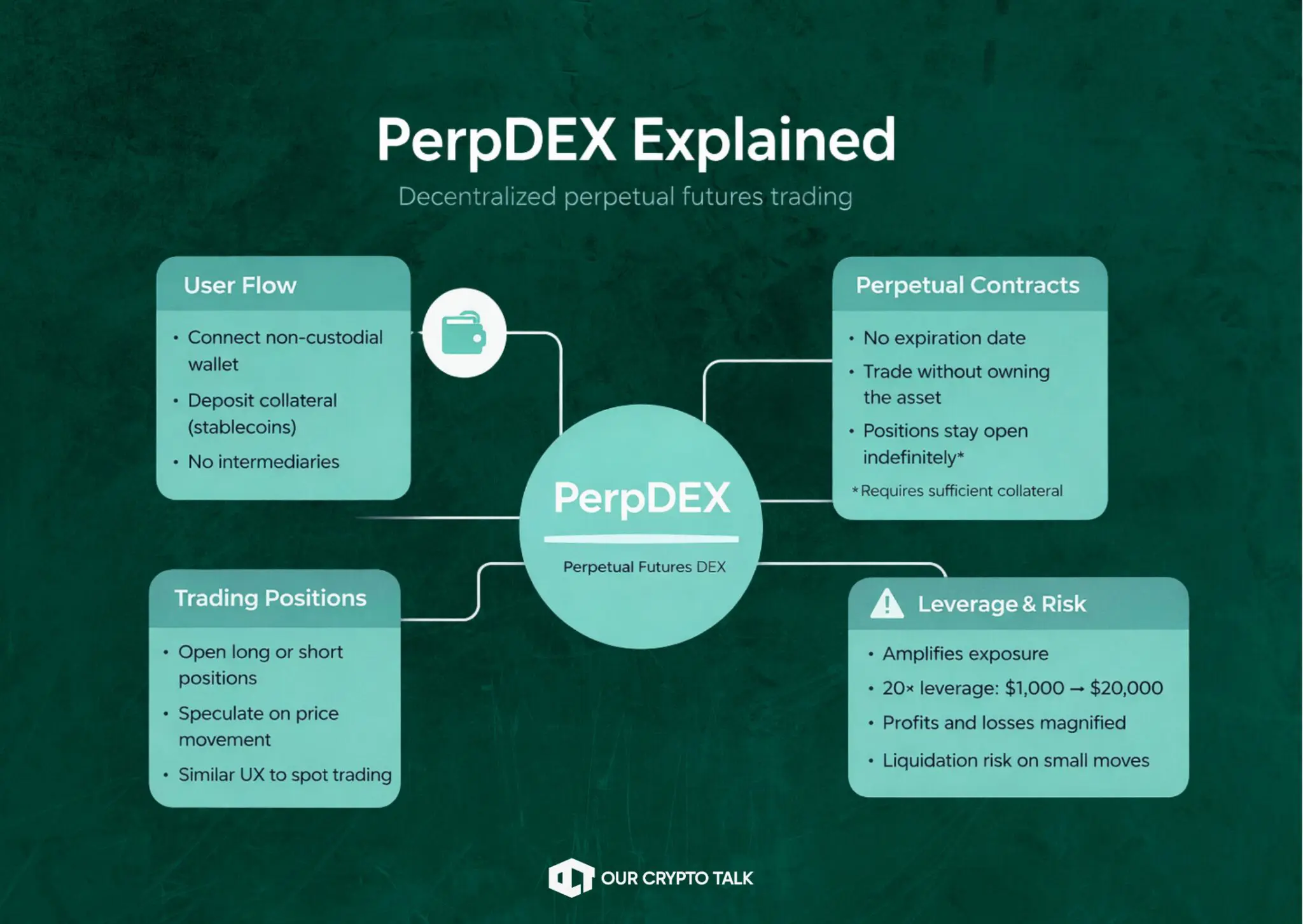

A perpDEX is a decentralized exchange designed specifically for perpetual futures trading. Unlike spot markets, where traders buy or sell the underlying asset, perpetual contracts allow traders to speculate on price movements without owning the asset itself.

The defining feature of perpetual contracts is the absence of an expiration date. Positions can remain open indefinitely, provided the trader maintains sufficient collateral. This design closely resembles spot trading while enabling leverage.

On a perpDEX, users typically:

Leverage allows traders to amplify exposure. For example, using 20x leverage, $1,000 in collateral controls a $20,000 position. This magnification works both ways. Small price movements can generate large profits or trigger liquidation.

To keep perpetual prices aligned with the spot market, perpDEXs use funding rates. These are periodic payments exchanged between long and short traders depending on market imbalance. If the perpetual price trades above spot, longs pay shorts. If it trades below, shorts pay longs. Over time, this mechanism anchors prices without needing contract expiry.

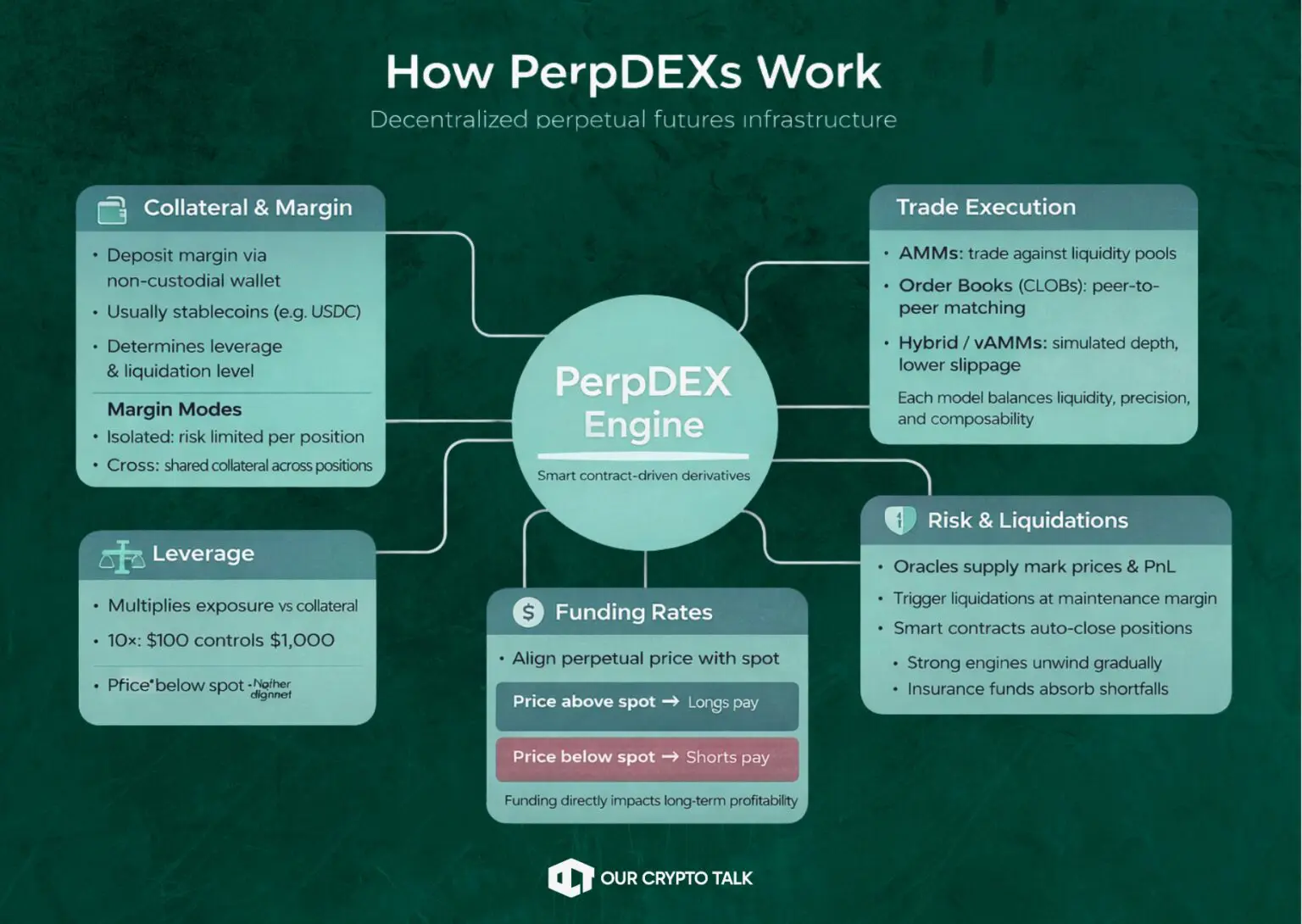

Technically, perpDEXs operate entirely on blockchain infrastructure. Smart contracts manage margin, calculate profit and loss, enforce liquidations, and distribute fees. There is no central operator holding custody or approving trades.

This structure differentiates perpDEXs from:

Different perpDEXs use different execution models. Some rely on automated market makers, where traders interact with liquidity pools. Others use order-book systems that match buyers and sellers directly. Hybrid designs attempt to combine both.

At their core, perpDEXs aim to deliver professional-grade derivatives trading while preserving the core DeFi principles of transparency, permissionless access, and self-custody.

The idea of perpetual futures did not originate in crypto. In traditional finance, economist Robert Shiller proposed continuous futures contracts in the early 1990s. However, it was crypto that turned theory into practice.

In 2016, BitMEX launched the first widely adopted crypto perpetual contract. The introduction of funding rates solved the price-tracking problem without requiring settlement dates. This innovation quickly made perpetuals the dominant derivatives instrument in crypto.

Decentralized versions emerged much later. Early attempts struggled with high gas fees, slow execution, and limited liquidity. The DeFi boom of 2020 changed that trajectory.

Platforms like dYdX demonstrated that decentralized perpetual trading could scale by moving matching engines off-chain while settling on-chain. Later, AMM-based designs like GMX simplified liquidity provisioning, allowing traders to trade directly against pooled capital.

The collapse of centralized exchanges accelerated adoption. Traders began prioritizing self-custody and transparency over convenience. Layer 2 solutions reduced costs, while purpose-built app chains improved execution speed.

By 2024–2026, perpDEXs no longer felt experimental. Some platforms achieved sub-second latency, deep liquidity, and institutional-grade tooling. At that point, perpDEXs stopped being “alternatives” and started becoming competitors.

At a glance, trading on a perpDEX may feel similar to using a centralized derivatives exchange. Under the hood, however, the mechanics are fundamentally different. Every action is governed by smart contracts, not custodial intermediaries.

Trading on a perpDEX begins with collateral. Users connect a non-custodial wallet and deposit margin, typically in stablecoins such as USDC. This collateral backs all open positions and determines how much leverage can be used.

Leverage is expressed as a multiplier. A 10x position means $100 of collateral controls $1,000 of exposure. Higher leverage increases capital efficiency but sharply raises liquidation risk.

PerpDEXs usually support two margin modes:

Cross margin improves capital efficiency but increases systemic exposure during volatility.

Different perpDEXs use different trade execution models.

Some platforms rely on automated market makers (AMMs). In this design, traders open positions against liquidity pools rather than other traders. Pricing is determined algorithmically, and liquidity providers earn fees in return for absorbing risk.

Other perpDEXs use central limit order books (CLOBs). Here, buy and sell orders are matched peer-to-peer, similar to traditional exchanges. This model offers tighter spreads and better price discovery but requires higher throughput.

Hybrid approaches also exist. Virtual AMMs simulate order-book depth mathematically, reducing slippage without requiring massive liquidity pools.

Each model has trade-offs. AMMs are simpler and more composable. Order books favor professional traders who demand precision.

Funding rates are central to how a perpDEX functions.

Because perpetual contracts never expire, funding payments keep prices aligned with the underlying spot market. These payments occur periodically, often every eight hours.

Over time, this mechanism discourages imbalance and anchors prices without settlement.

For traders, funding rates are not just a technical detail. They directly impact profitability, especially for long-held positions.

Oracles supply external price data to perpDEX smart contracts. These feeds determine:

Most modern perpDEXs use multi-source, time-weighted oracle systems to reduce manipulation risk. Weak oracle design can lead to unfair liquidations, making oracle integrity a key evaluation factor.

When a position’s equity falls below maintenance margin, liquidation is triggered automatically. Smart contracts close positions to prevent losses from exceeding collateral.

Liquidation engines vary by platform. Strong systems unwind positions gradually to avoid cascading failures. Weak ones cause abrupt market impact and systemic risk.

Insurance funds absorb shortfalls when liquidations fail to cover losses, protecting the protocol and other traders.

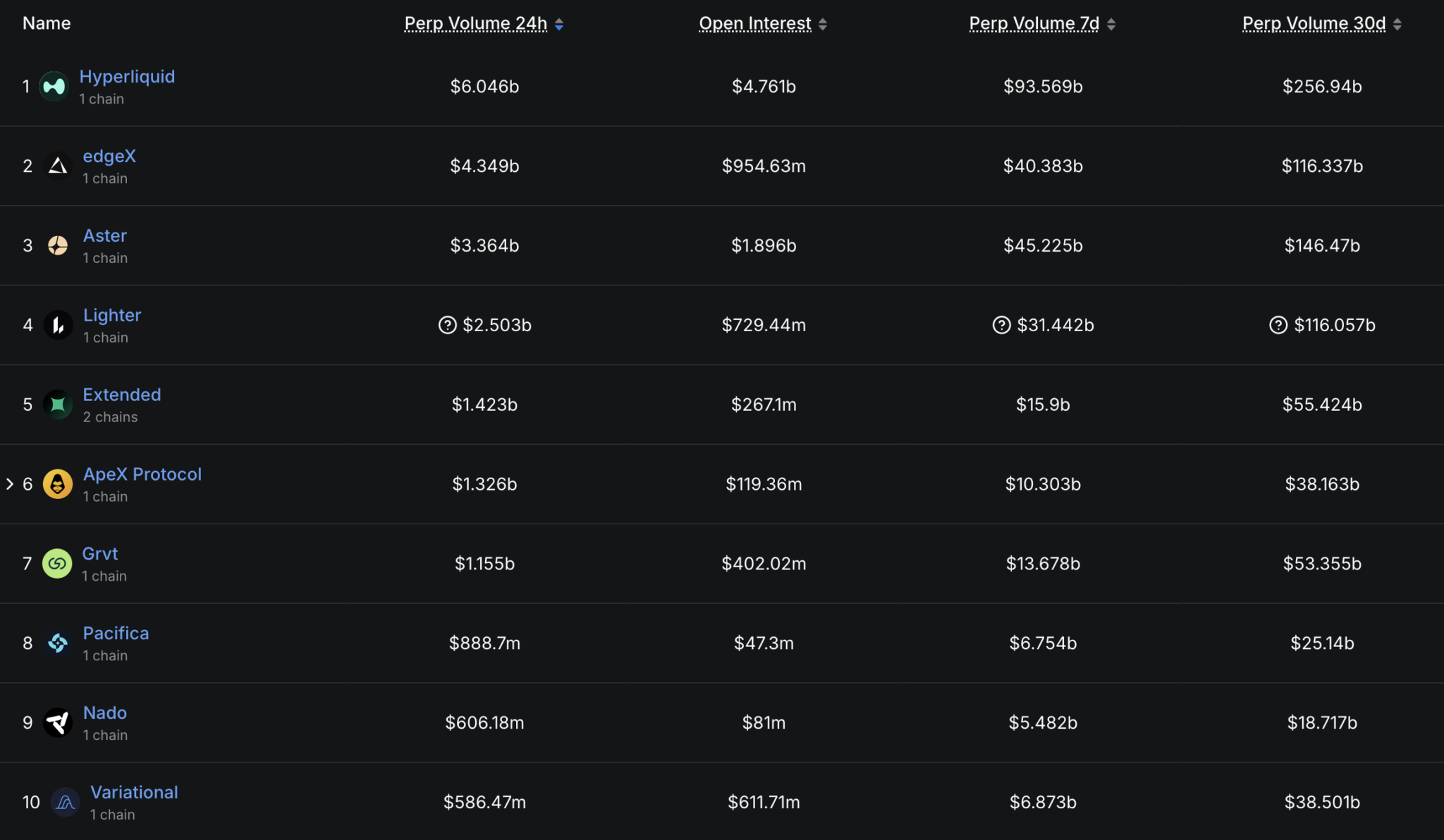

Not all perpDEXs are created equal. Evaluating them requires looking beyond surface-level volume numbers.

Volume shows activity, but it can be misleading. Incentive programs sometimes inflate numbers without real demand.

Open interest (OI) provides better insight. It represents the total value of open positions. A high OI relative to volume suggests traders are holding positions rather than wash trading.

Healthy perpDEXs maintain a balanced relationship between volume and OI.

TVL reflects how much capital is committed to the platform. Higher TVL usually indicates trust, liquidity depth, and resilience during volatility.

Comparing volume-to-TVL ratios helps assess capital efficiency. High efficiency suggests strong utilization of liquidity.

Fees affect both traders and protocol sustainability.

Key considerations include:

Some perpDEXs use protocol revenue for buybacks, insurance funds, or governance incentives. Transparent fee models signal maturity.

Execution speed matters, especially for active traders.

Metrics like:

directly influence slippage and liquidation outcomes. Modern perpDEXs increasingly rival centralized exchanges in performance.

Frequent liquidation cascades indicate weak risk management. Monitoring liquidation volume during volatile periods reveals how well a perpDEX handles stress.

Finally, organic usage matters. Sustained growth without heavy incentives signals product-market fit.

Metrics such as active traders, retention rates, and repeat volume provide context beyond headline numbers.

By 2026, the perpDEX landscape has matured into a competitive, multi-model ecosystem. Different platforms optimize for speed, depth, accessibility, or innovation, rather than trying to serve everyone.

Hyperliquid has emerged as the dominant perpDEX by volume and open interest. Built on a proprietary Layer 1 chain, it prioritizes execution speed and reliability. Sub-second latency and high throughput allow it to rival centralized exchanges in trading experience.

Its strengths lie in:

However, its design favors experienced users. Risk management tools are powerful but assume discipline and familiarity with leverage.

Aster focuses on accessibility and breadth. It supports perpetuals across crypto, synthetic equities, and forex-style markets, lowering the barrier for traders migrating from traditional finance.

Zero-fee models and simplified UX attract retail users, but liquidity depth can lag behind specialist platforms during extreme volatility.

dYdX remains one of the most established perpDEXs. Its v4 iteration runs on a Cosmos-based app chain, combining decentralized governance with a professional order-book model.

The platform appeals to:

While execution is solid, competition from faster app-chain designs has pressured its market share.

GMX takes a different approach. Instead of order books, it relies on pooled liquidity through GLP. Traders interact directly with liquidity providers, reducing reliance on counterparties.

This model works well for:

The trade-off is less precise price discovery compared to order-book-based perpDEXs.

Newer entrants continue to experiment. Some prioritize zero fees using zk-proofs, while others focus on cross-chain margin or institutional tooling. The common theme is specialization rather than generalization.

The appeal of perpDEX platforms is structural, not cyclical.

PerpDEXs eliminate custodial risk. Funds remain in user-controlled wallets, governed by transparent smart contracts. This directly addresses failures seen in centralized derivatives markets.

All trades, liquidations, and fee flows are either on-chain or cryptographically verifiable. This visibility enables independent monitoring and reduces information asymmetry.

PerpDEXs operate without geographic restrictions or mandatory KYC. Anyone with a wallet can participate, aligning with crypto’s open-access ethos.

Perpetual contracts allow traders to express directional views without tying up large amounts of capital. For hedging, market-making, or short-term speculation, this efficiency is unmatched.

PerpDEXs integrate naturally with other DeFi primitives. Collateral, yield strategies, and governance tokens can interoperate in ways centralized systems cannot support.

Despite their strengths, perpDEXs introduce unique risks that require discipline and understanding.

High leverage magnifies volatility. Small adverse moves can trigger liquidations, wiping out positions quickly. This risk is structural and unavoidable.

During sharp market moves, forced liquidations can cascade, pushing prices further against open positions. Platforms with weaker risk engines are particularly vulnerable.

PerpDEXs rely on external price feeds. Oracle failures or manipulation can cause incorrect mark prices and unfair liquidations. Robust oracle design is critical.

Even audited contracts can fail. Bugs, edge cases, or economic exploits remain an ongoing risk in decentralized systems.

For long-held positions, funding payments can erode returns over time. Traders who ignore funding dynamics often misjudge profitability.

Looking ahead, perpDEXs are positioned to play a central role in crypto market structure.

More platforms are adopting custom chains to achieve low latency and high throughput. This trend blurs the line between centralized and decentralized performance.

Future perpDEXs are likely to support seamless cross-chain collateral, reducing fragmentation and improving capital efficiency.

Synthetic perpetuals on equities, commodities, and macro indices are gaining traction. This could open perpDEXs to entirely new user bases.

AI-assisted liquidation engines, predictive funding models, and adaptive margin requirements aim to reduce systemic risk without sacrificing efficiency.

As frameworks mature, compliant perpDEXs may attract institutional capital without abandoning self-custody principles.