Loading Search...

Uniswap recently experienced a major economic shift when its long-discussed fee switch finally activated along with a 100M $UNI burn.

Author: Sahil Thakur

Uniswap is the largest decentralized exchange on Ethereum. Recently, it experienced a major economic shift when its long-discussed fee switch finally activated. This change came through a governance proposal called UNIfication. The proposal turned on a built-in protocol fee and also changed how Uniswap manages its UNI token supply.

In late December 2025, the Uniswap community voted strongly in favor of this plan. At the same time, they burned 100 million UNI tokens. That event became one of the largest token burns in DeFi history.

This article explains what changed, how it affects users and liquidity providers, how the new revenue model works, what happened during the UNI burn, and what it could mean for DeFi in the future.

Since Uniswap V2 launched in May 2020, the protocol included a hidden fee switch. It allowed Uniswap to redirect part of trading fees to the protocol. However, the switch stayed turned off for years. Liquidity providers received all fees, and the protocol itself received nothing.

That situation is now different. The community vote activated the switch. A share of the fees that traders pay now flows to the protocol. The protocol uses these fees in a buyback-and-burn mechanism for UNI. As a result, the protocol gains revenue and reduces token supply at the same time.

Trading fees for users do not increase. The structure simply changes behind the scenes.

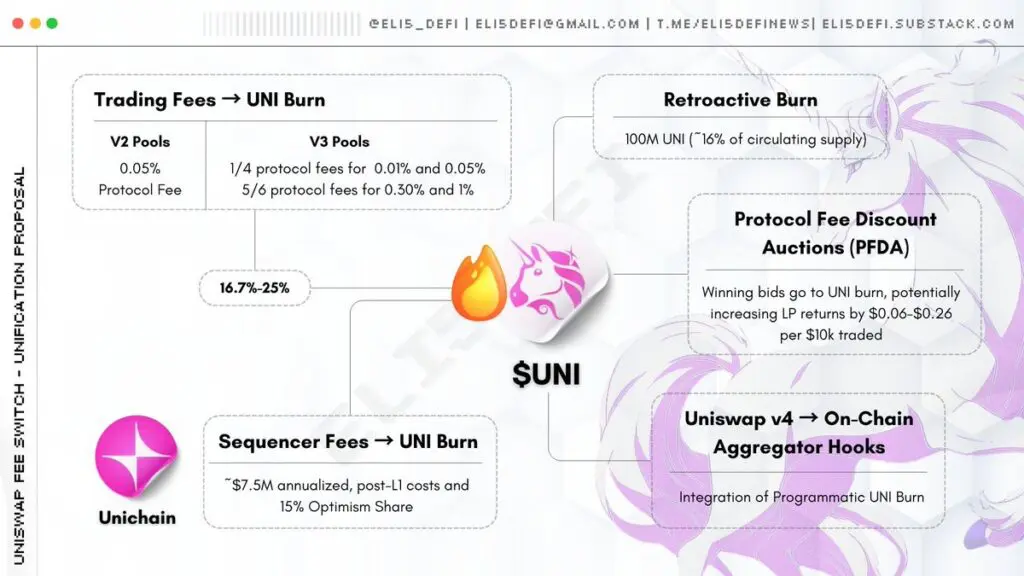

In Uniswap V2, trades still cost 0.30 percent. Liquidity providers now receive 0.25 percent. The remaining 0.05 percent goes to the protocol.

Uniswap V3 works differently. It uses multiple fee tiers. Governance decided that the protocol receives one sixth of LP fees on the 0.30 percent and 1 percent tiers. It receives one fourth of LP fees on the 0.01 percent and 0.05 percent tiers.

So, 16 to 25 percent of fees that once belonged entirely to LPs now supports the protocol instead. Importantly, traders do not pay extra. Only the distribution changes.

At first, the switch applies to Uniswap V2 and to selected V3 pools on Ethereum. These pools represent roughly 80 to 95 percent of LP fees on Ethereum. The plan is gradual expansion to other networks and to future Uniswap versions after results are reviewed.

Alongside protocol fees, Uniswap Labs removed fees from its interface, wallet, and API. Previously, some trades included small charges at the app level. Now, those fees are set to zero.

This choice puts more focus on the protocol itself. It also aligns more closely with decentralization principles. Uniswap Labs has stated that it will concentrate on development and growth. It is also coordinating more closely with the Uniswap Foundation to simplify ecosystem strategy.

Before this change, Uniswap did not capture value for UNI holders. All trading fees supported liquidity providers only. Now, every trade indirectly benefits the UNI supply.

Part of each fee goes to buy UNI and burn it. Over time, this reduces total supply. The token becomes scarcer. This connects the token more directly to protocol success and long-term usage.

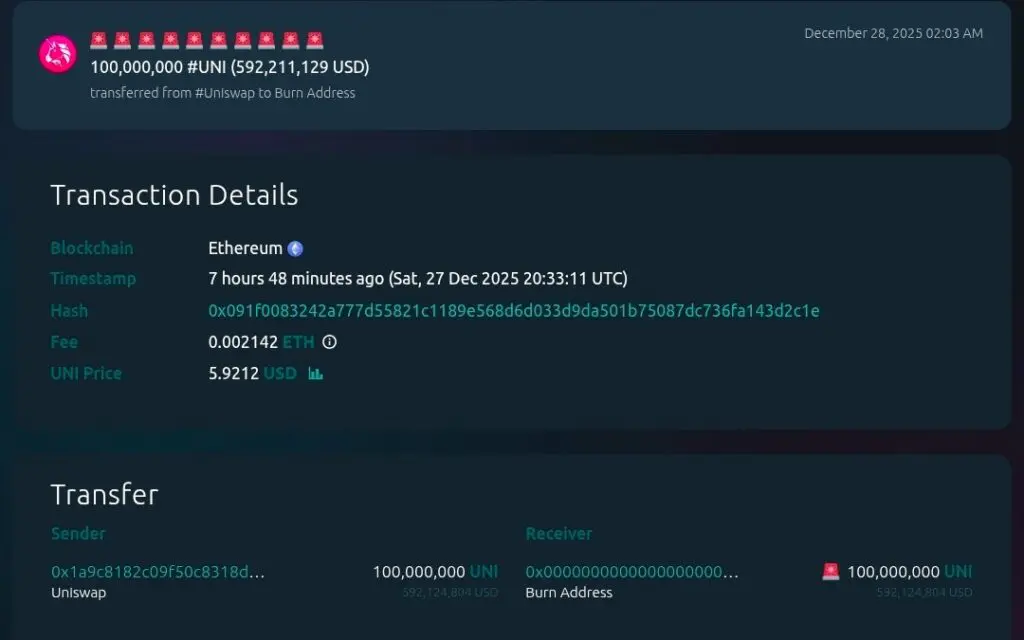

The first major step was immediate. The community burned 100 million UNI. The circulating supply dropped from about 830 million to nearly 730 million. From now on, regular burns will continue as the protocol collects fees.

Src: X (Eli5Defi)

Traders feel little change at first. Their fees stay the same. Their experience stays familiar.

Over time, users might benefit indirectly. More sustainable funding could support new features and deeper liquidity. The rollout is slow on purpose to avoid sudden disruption.

Liquidity providers receive less per trade. In active pools, they now keep about 75 to 83 percent of former fee revenue. For instance, in V2 they receive 0.25 percent instead of 0.30 percent.

This reduction could push some LPs to reconsider participation. Even so, governance plans to monitor outcomes and explore incentives that offset the reduction.

One idea is the Protocol Fee Discount Auction. In this system, third parties bid for temporary trading discounts. The winning bids go toward UNI burns. This may also capture MEV that would otherwise leave the protocol. If effective, LPs could benefit through better execution and potentially stronger volume.

In the early days, the fee switch generated about 30,000 dollars per day on Ethereum. That equals roughly 11 million dollars per year. Relative to total fees, this figure is small. As adoption expands across more pools and chains, LPs will watch closely to see if profitability remains attractive.

UNI holders gain the most direct benefit. They now own a token tied to protocol revenue and supply reduction. This model creates clearer economic value and stronger alignment between participants and governance.

However, market reaction was cautious. UNI fell slightly after the burn. Many traders likely expected the change earlier. Others may want to see real revenue results before reacting.

Still, the token now has a sustainable mechanism that ties growth to scarcity. Many analysts see this as a move toward more mature token economics in DeFi.

The fee switch sits inside a broader restructuring of Uniswap’s operations. This proposal came jointly from Uniswap Labs and the Uniswap Foundation, which signaled a rare level of alignment.

Several teams from the Foundation are moving into Uniswap Labs. As a result, development efforts now consolidate under a single organization.

Uniswap Labs also made a clear commitment. It will focus on protocol development and long-term growth. It will stop charging front-end fees on its products. Therefore, Uniswap Labs will rely more on the protocol’s success and the value of its UNI holdings, instead of collecting direct user fees.

Src: Blockworks

Uniswap set aside 20 million UNI from the treasury for a Growth Budget. This budget supports grants, development work, and expansion efforts.

The plan ensures something important. Even while UNI supply declines through burning, Uniswap still keeps resources to fund contributors. Developers can continue to build, experiment, and launch new features such as Uniswap v4 hooks.

Overall, Uniswap is investing in long-term innovation. The protocol wants to fund itself through its treasury and future fee revenue. Consequently, it becomes less dependent on venture capital or inflationary token issuance. Investors also benefit from a more attractive token economy.

Uniswap runs on Ethereum, but it is not its own blockchain. Therefore, it does not have validators. Ethereum validators still process transactions and still earn gas fees as usual.

The fee switch mainly changes how Uniswap splits internal fees. It does not affect Ethereum gas pricing or how blocks get validated.

If Uniswap volume grows, validators could earn slightly more gas revenue. If volume shrinks, they could see slightly less. However, early data showed no major change in trading activity just because of the fee switch.

One part of the roadmap could have a secondary effect. The PFDA auctions aim to capture some MEV that arbitrage bots or validators currently receive. If that system succeeds, validators might earn a little less MEV on some Uniswap trades. Still, this remains speculative and depends on future implementation.

In summary, Ethereum validators feel no direct impact. The fee switch mainly redistributes value within Uniswap itself, between LPs and UNI holders.

Before this change, Uniswap generated no revenue for its own treasury. LPs earned fees, while governance collected nothing. As a result, UNI relied mostly on speculation and governance rights, not cash flow.

Now the situation is different. The fee switch gives Uniswap a real revenue mechanism. The protocol collects part of trading fees across supported pools. Then, instead of storing that revenue, it buys UNI and burns it.

This process creates a buyback-and-burn model. It resembles a company buying back shares. Over time, UNI supply shrinks as usage grows. That shift creates deflationary pressure and stronger value alignment.

Uniswap produced more than 1.05 billion dollars in trading fees in 2025 across all deployments. None of that previously benefited the protocol. With even a small fraction redirected, the impact becomes meaningful.

Depending on fee tiers and pool coverage, Uniswap could route tens of millions per year into UNI burns. Early projections suggested about 22 million dollars annually under partial activation. As more pools activate and new sources like Layer 2 fees and MEV auctions come online, that figure could increase.

Governance intentionally chose burning instead of distributing profits to token holders. This avoids giving UNI characteristics similar to a traditional dividend, while still creating value accrual.

3-year revenue earned by Dexs. Src: Token Terminal

The treasury previously held large UNI reserves. Burning 100 million tokens and allocating 20 million to growth signaled a firm shift in priorities. Uniswap chose deflation and sustainability over hoarding supply.

The remaining treasury will support development and ecosystem initiatives. In the future, governance might decide to redirect some fees to insurance, reserves, or operations. For now, nearly all value flows into burns after covering operating expenses.

Uniswap’s new Layer 2 rollup, Unichain, also contributes. After paying costs such as Ethereum data posting and Optimism’s share, remaining sequencer fees go toward UNI burns. Thus, every component of the ecosystem now feeds value into the token.

Once the switch activated, Uniswap instantly joined the top revenue-generating protocols with captured protocol income. It had already ranked high in total fees. Now those fees support both sustainability and token value.

This move sets a precedent. DeFi protocols can sustain themselves by capturing a portion of platform fees instead of relying only on incentives or inflation. Uniswap transitions from zero protocol revenue to a controlled fee capture model that still favors LP competitiveness.

The path to activating the fee switch took years. Many in the community describe it as a multi-year saga.

Uniswap leaders began debating protocol fees as early as 2020. The fee switch code already existed in Uniswap V2. Yet governance chose to leave it off. The priority focused on growth, liquidity, and regulatory caution.

As a result, conversations dragged on across forums and social channels. People debated benefits, risks, and timing. Progress felt slow, but the topic never disappeared.

By mid-2022, the community attempted a small experiment. A proposal suggested turning on fees in a few pools. That idea never became permanent. However, it showed that interest in revenue capture was growing.

Pressure intensified throughout 2023 and early 2024. UNI holders increasingly questioned why Uniswap collected no protocol revenue. Trading volume soared, yet token holders saw little direct benefit.

A major vote was scheduled for May 31, 2024. The idea involved rewarding UNI holders who staked and delegated tokens. In short, fees would have gone directly to stakers.

At the last minute, the Foundation delayed the vote. A stakeholder raised concerns. Governance paused to reassess. Many suspected regulatory risk. Sharing protocol fees directly can resemble dividend payments. In the U.S. that risked treating UNI as a security. So Uniswap slowed down instead of pushing ahead recklessly.

By late 2025, conditions looked different. The regulatory environment appeared less hostile, and DeFi was maturing.

Uniswap Labs and the Foundation worked together on a comprehensive proposal called UNIfication. Instead of sharing fees with stakers, the proposal emphasized burning UNI. That structure offered benefits to holders while reducing regulatory exposure.

The plan appeared on the governance forum on November 10, 2025. It presented an eight-point roadmap that covered fees, burns, organizational realignment, and growth initiatives. After public feedback, the team refined pool selections and details. On December 18, 2025, governance submitted the final proposal on-chain.

Voting ran from December 19 through Christmas Day. Support came in overwhelmingly. Roughly 99.9 percent of votes supported the proposal. More than 125 million UNI voted yes. Only 742 tokens voted no.

The result showed a dramatic shift in sentiment. After years of reluctance, the community now embraced value accrual. Hayden Adams celebrated the outcome publicly, calling the decision unified in spirit.

After a standard two-day timelock, implementation began. The protocol burned 100 million UNI. Governance activated fee switches on selected pools. Uniswap Labs removed frontend fees and redirected focus to protocol development. Execution finished only two days after voting ended.

Src: X

The final vote moved quickly. Yet the journey stretched across more than five years. Uniswap V2 first included the fee switch in 2020. The community attempted major proposals in 2022 and 2024. Countless forum debates filled the years in between.

The lesson is simple. DeFi governance tends to move slowly by design. Uniswap waited until the community felt confident, conditions improved, and the model balanced incentives with regulatory caution.

Once consensus formed around burning fees instead of distributing them, the decision came swiftly. After years of uncertainty, Uniswap finally flipped the elusive fee switch.

One of the headline outcomes of the fee switch change was the massive burn of 100 million UNI tokens immediately following the vote. This burn was executed on-chain on December 28, 2025 around 4:30 AM UTC , effectively permanently destroying 100M UNI from the Uniswap Community Treasury. At the time, these tokens were valued at roughly $590–$600 million USD . The burn transaction was confirmed by Uniswap Labs on Twitter, stating “UNIfication has officially been executed on-chain” as the 100M UNI were sent to a null address .

This 100M burn has multiple significances:

Src: Etherscan

Going forward, regular continuous burns will occur as the protocol accumulates fees. Uniswap has implemented an on-chain module (often called the TokenJar) where various fee streams will be deposited and from which UNI will be periodically burned . In the initial setup, fees from Ethereum pools and Unichain (Uniswap’s Layer-2 rollup launched 9 months prior) will start flowing into this burn system . The first 100M burn was a one-off event, but it kicks off a new era where UNI’s supply is on a downward trajectory whenever Uniswap usage remains strong.

Uniswap founder Hayden Adams emphasized that the initial burn should not be over-interpreted in terms of long-term effects . He explained that only some fee sources were live at the start, and that the burn mechanism needs time to ramp up (fees accrue in many tokens and are converted gradually, etc.) . The “steady state” of UNI burns will become clearer over time. Nonetheless, the 100M burn was a clear signal of Uniswap’s new direction – turning past momentum into tangible value for its ecosystem.

Uniswap now operates with deflationary economics. As protocol fees accumulate, the system uses them to burn UNI. Over time, circulating supply should fall.

If trading volume grows, burn rates rise as well. This creates a reinforcing cycle. More usage leads to more fees. More fees lead to more UNI burned. Scarcity then may support higher value, which can attract more users and investors.

However, the effect will take time. Initial revenue sits around 30,000 dollars a day on Ethereum. That level burns UNI slowly. As new fee sources activate, the pace should increase.

Unichain already contributes sequencer revenue. Additional deployments and fee switches across other chains could amplify this trend significantly.

UNI now has clearer economic purpose. Previously, critics argued that UNI only offered governance rights. Now it absorbs value from Uniswap’s activity.

This shift could attract long-term investors who look for assets tied to real protocol economics. It may also motivate more holders to participate in governance, since their decisions directly influence value creation.

If 2026 brings renewed focus on fundamentals, UNI could benefit. Tokens without revenue models may struggle to compete.

In the near term, Uniswap governance plans to observe results closely. Key metrics include liquidity levels, trading volume, and weekly burn totals.

Some early analysts claimed revenue numbers looked underwhelming. Hayden Adams pushed back, arguing the rollout was only beginning and early estimates ignored future fee sources.

As more elements go live, revenue should compound. These include MEV auctions, aggregator fees in Uniswap v4, and expansion to more pools and networks. Each improvement can raise burn totals and refine incentives for LPs.

The buy-and-burn model introduces consistent market demand tied to usage. Over longer horizons, this should act as a supportive force for price.

Still, crypto markets respond to many variables. Sentiment, macro trends, and competition all matter. UNI did not spike immediately after activation, which shows traders want proof of sustained revenue.

Governance retains flexibility. If conditions change, the community can adjust fee fractions or expand the switch to additional pools.

With funding secured, Uniswap can invest in innovation more confidently. The Growth Budget funds grants, ecosystem partnerships, and development initiatives.

Uniswap v4 also introduces hooks and aggregator capabilities. The protocol can route trades across DEXs to secure best pricing while collecting fees that burn UNI. That combination strengthens both user experience and protocol economics.

Over time, Uniswap can compete more directly with centralized exchanges. A self-funded system can launch new features, incentivize adoption, and support integrations without depending on outside capital.

Uniswap also hopes to that the fee switch will help to operate more clearly within regulatory expectations. By using token burns instead of direct payouts, UNI avoids functioning like a dividend-bearing security.

Authorities may continue to review these models. However, many in the community believe this structure represents a safer framework. If regulators accept it, other protocols may follow.

In effect, Uniswap becomes a test case for how decentralized systems can create value responsibly.

Uniswap marks a turning point for governance tokens. More projects are now searching for meaningful value capture.

Tokens like xSUSHI and veCRV pioneered rewards tied to protocol revenue. Uniswap’s move further legitimizes this direction. Many DeFi teams may now feel pressure to design similar models that align users, LPs, and token holders.

Some LPs may consider moving to platforms without protocol fees. However, many leading DEXs already implement fee capture.

In practice, LPs focus on net earnings, not just percentages. High trading volume on Uniswap may still make participation attractive. Meanwhile, protocols that refuse to capture revenue could struggle to sustain themselves.

With revenue flowing to development, protocols can innovate faster. Uniswap’s work on MEV capture, aggregation, and cross-chain strategies may inspire others to experiment as well.

Instead of competing primarily through liquidity incentives, DeFi could shift to competition around revenue optimization and user experience.

The UNIfication vote attracted high turnout and near-unanimous support. That success demonstrates what coordinated governance can achieve.

Communities may become more engaged when they see governance translate into tangible outcomes. Other DAOs could use Uniswap as a model for patient debate followed by decisive execution.

Regulators will watch closely. If Uniswap operates smoothly and avoids enforcement actions, more teams may adopt burn-based models. If challenges arise, the industry will adjust.

Either way, DeFi gains clarity from observing how such a large protocol moves forward.

Uniswap now has financial durability similar to established businesses. As it scales, it becomes a stronger rival to centralized exchanges.

More users may shift activity toward decentralized markets, especially if they trust the economics and transparency of protocols like Uniswap. Centralized exchanges may need to innovate to keep pace.

Uniswap has created a sustainable economic loop: protocol usage funds UNI burns, which strengthen incentives, which then support more usage.

The effects will unfold slowly but steadily. Over months and years, Uniswap could evolve from a pioneering DEX into a fully self-sustaining financial network.

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?

What If Satoshi Nakamoto Was Here in 2026?

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?

What If Satoshi Nakamoto Was Here in 2026?