Loading Search...

Discover where crypto actually makes money in 2026, from trading and wallets to lending, tokenized assets and real-world infrastructure.

Author: Arushi Garg

For years, crypto projects did not need to generate revenue. Growth alone was celebrated. If a project had a compelling narrative, a growing community on Discord, and a token that could trend on social media, the market assumed monetization would come later. Emissions were treated as adoption, and fees were optional. Now, in 2026, crypto makes money where users actually pay through trading, wallets, lending, tokenized assets, and real-world infrastructure.

That world no longer exists.

By 2026, the crypto landscape has matured. Capital is far less forgiving, liquidity is selective, and regulation is clearer. Institutions participate, but only where the economics make sense. In this environment, one question dominates every evaluation: Who is actually paying to use this?

Revenue has become the clearest signal of product-market fit in crypto. It shows whether users return without incentives, whether protocols can fund development without diluting tokens, and which narratives represent real businesses versus experiments still searching for demand.

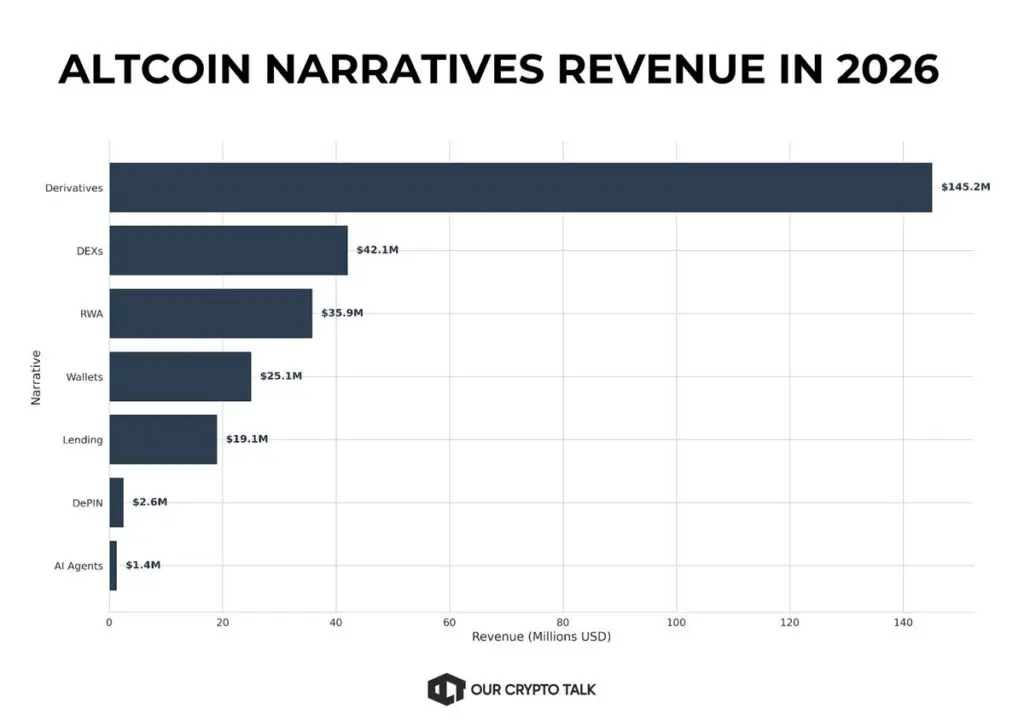

When you study crypto revenue in 2026, two patterns become clear quickly. First, only a handful of narratives generate meaningful cash flow. Second, within those narratives, revenue concentrates rapidly. One or two projects dominate, while the rest struggle to stay relevant.

This section explores where crypto revenue is coming from in 2026, why certain narratives lead, and why dominance forms so quickly once monetization begins.

Derivatives are the top revenue-generating segment in crypto. They succeed because they monetize urgency:

This creates a natural revenue engine. Unlike speculative tokens, derivatives protocols earn consistently whenever activity occurs, making them highly attractive to investors and institutions alike.

Leverage, hedging, and speculation exist in every market condition. Perpetual futures removed expiry while keeping leverage, making them appealing to both retail traders and institutional participants.

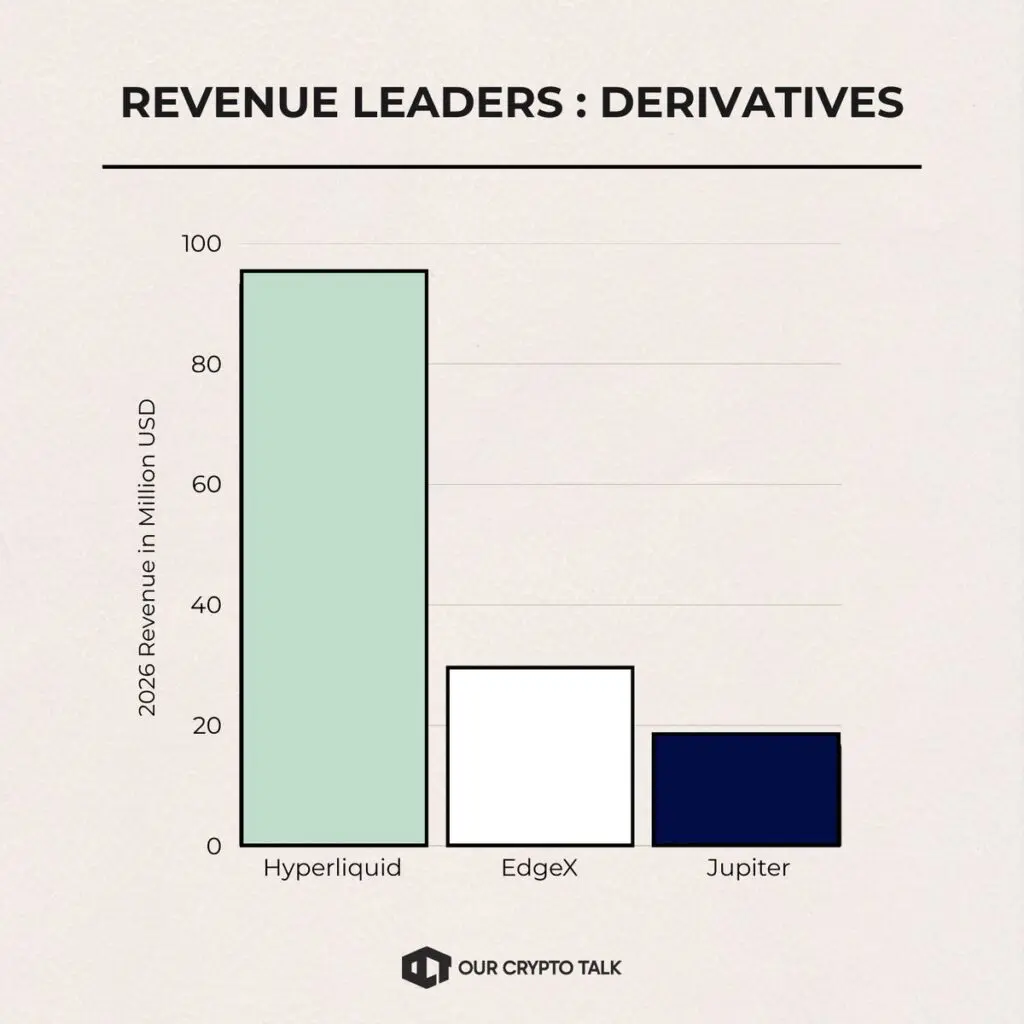

As on-chain execution improved and regulatory pressure increased on centralized exchanges, trading volume steadily shifted on-chain. This is where dominance formed quickly. Hyperliquid leads the derivatives category. It generated over $90 million in recent fees and operates at an annualized rate near $800 million. Its scale comes from deep liquidity, strong market maker participation, and execution that traders trust for large positions.

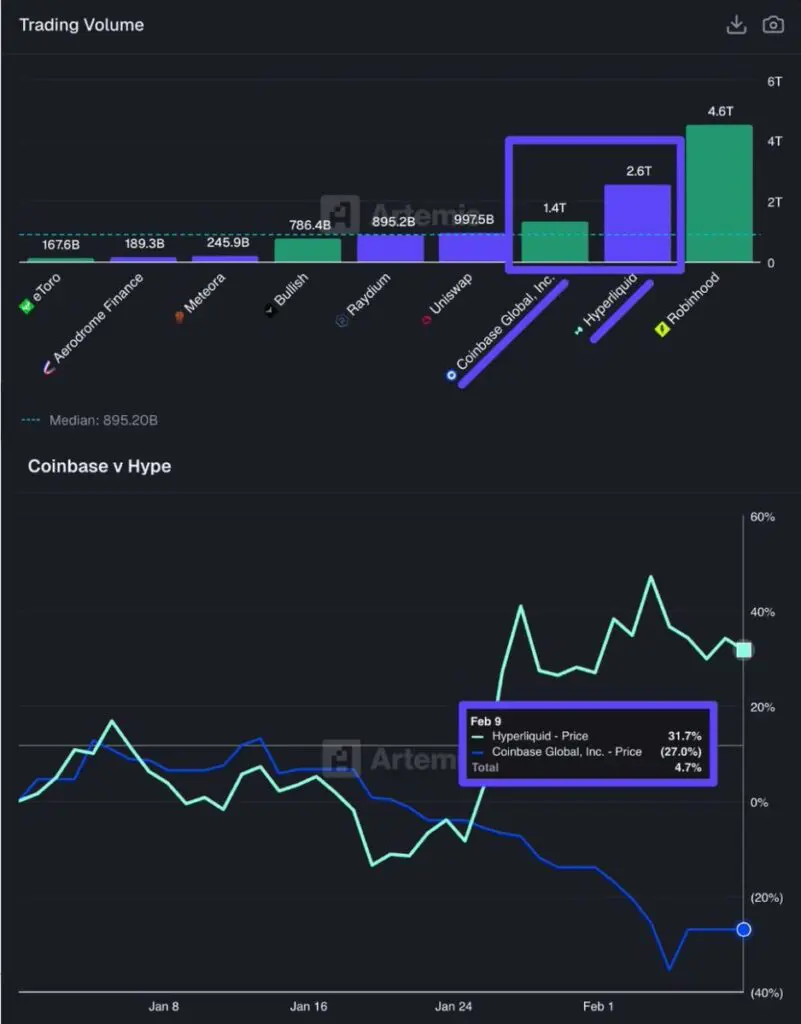

Hyperliquid expanded monetization without increasing risk. Outcome contracts, prediction-style markets, and options boosted revenue per user instead of simply chasing new users. Recently, Hyperliquid even outpaced Coinbase in notional volume, recording $2.6 trillion compared to Coinbase’s $1.4 trillion.

Once traders settled on effective platforms, liquidity and fees began to compound. EdgeX demonstrates that growth is still possible without full dominance. Low fees and a strong mobile UX generated close to $30 million in fees, but without deep liquidity, revenue remains less sticky.

Jupiter benefits from distribution. Its derivatives revenue is stable because users already route trades through it, but its upside is capped compared to a pure derivatives leader. Derivatives reward reliability. Once a platform proves it can handle volatility at scale, traders stop experimenting, and revenue concentrates quickly.

Pump leads because it monetizes speculation directly. Memecoin launches and rapid rotation generated over $15 million in recent fees. Pump does not fight trader behavior; it charges for it. Meteora succeeds through market structure. Dynamic liquidity pools and improved capital efficiency drove massive volume and over $12 million in fees. This reflects DeFi maturing from ideology to engineering.

Aerodrome stabilized revenue by fixing token economics. Reduced emissions and buybacks turned inflation-driven growth into sustainable fee generation. DEXs no longer reward neutrality. Platforms that understand trader behavior or design better markets are the ones that keep generating fees consistently.

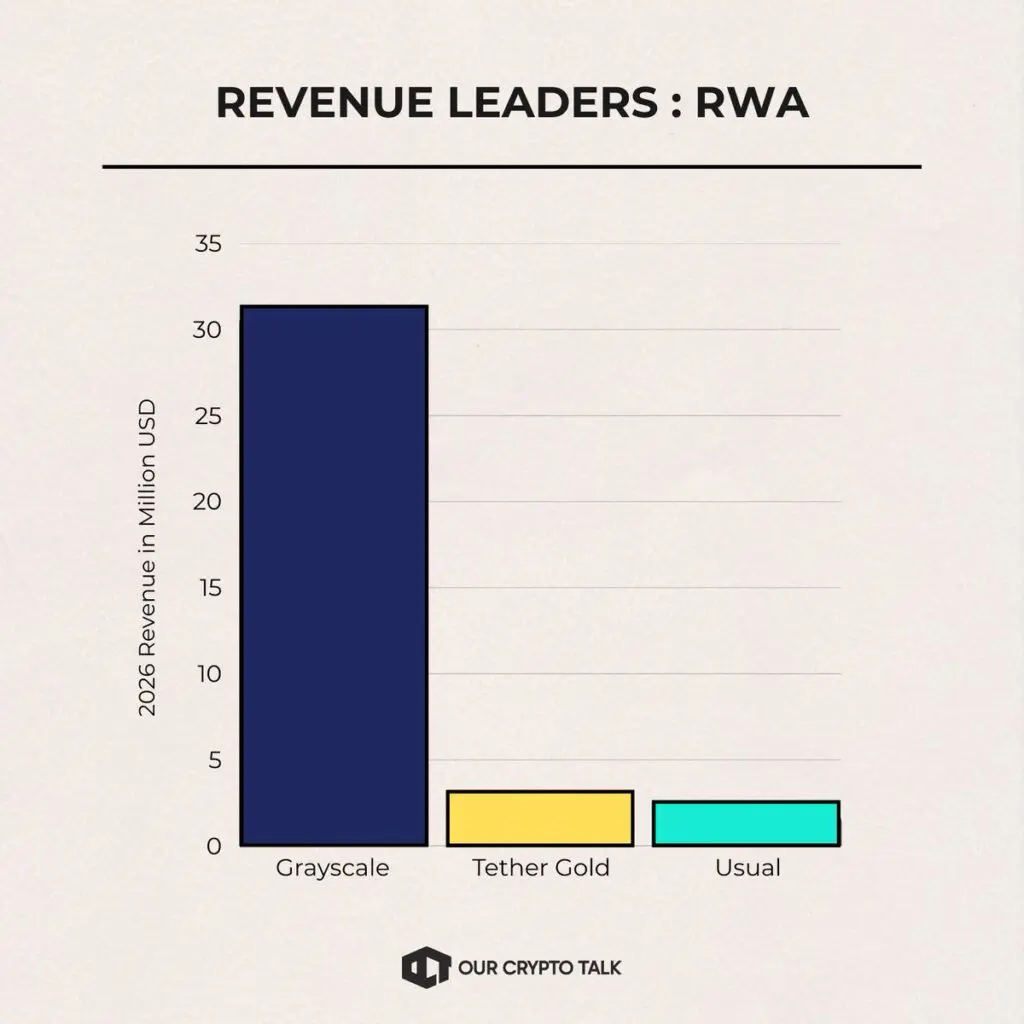

Real World Asset (RWA) protocols often feel slow or underwhelming to retail participants. Token prices move gradually, engagement is low, and the narrative lacks the excitement of AI or DePIN. Revenue tells a different story. RWA projects like Grayscale show that even when narratives feel weak, monetization can be strong, driven by institutional participation and predictable fee generation.

Real World Assets (RWAs) generate revenue by monetizing trust, compliance, and distribution rather than speculation. This approach makes them slower to scale but extremely sticky once adoption begins.

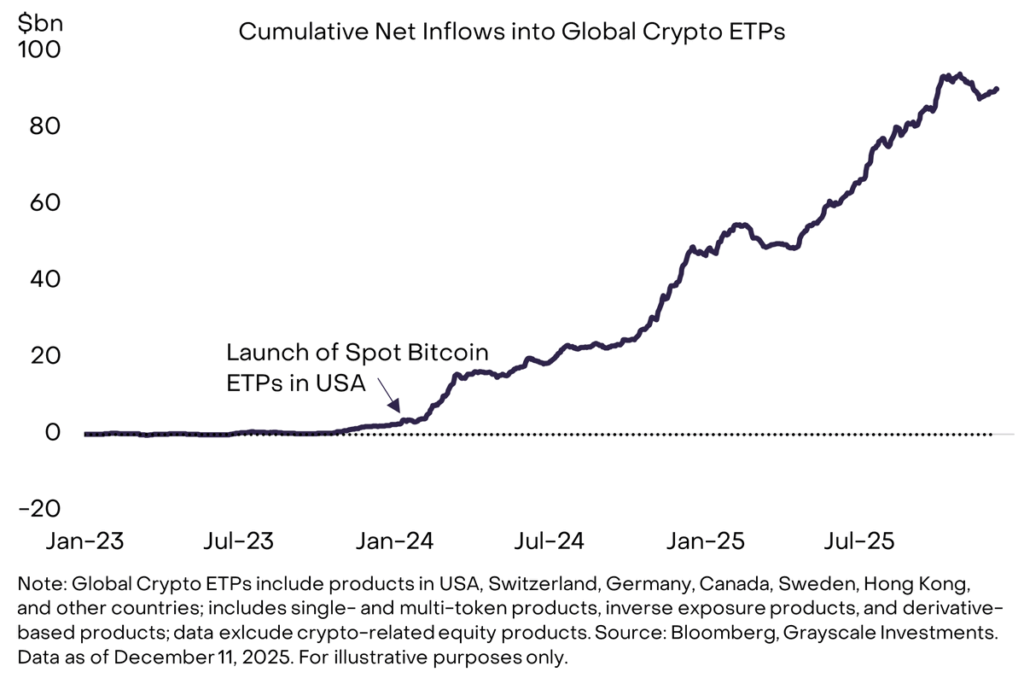

Grayscale dominates this category. In early 2026, Grayscale generated over $30 million in fees, far surpassing other RWA-focused protocols. Its exchange-traded products attract institutional inflows even when broader crypto sentiment is weak.

Since 2024, global crypto ETPs have seen tens of billions in net inflows, and Grayscale has captured a significant share. This highlights that reliable revenue in crypto increasingly comes from predictable, trust-based products rather than hype-driven narratives.

The reason for Grayscale’s dominance is structural. Grayscale operates as an asset manager first and a crypto-native platform second. Its products fit seamlessly into existing institutional workflows. Compliance is built in, and scaling is familiar.

While retail interest in RWAs fluctuates, institutions continue allocating. Even small allocation percentages represent enormous capital pools. Less than one percent of advised wealth in the United States is allocated to crypto products, leaving room for massive growth. Grayscale benefits from this asymmetry.

Competitors like BlackRock’s BUIDL exist, but Grayscale’s early positioning and distribution advantage give it an edge. The platform focuses on revenue-generating blockchains and established assets rather than experimental structures. While the RWA narrative may feel quiet, revenue concentration tells the real story: institutions commit slowly, but when they do, they commit at scale.

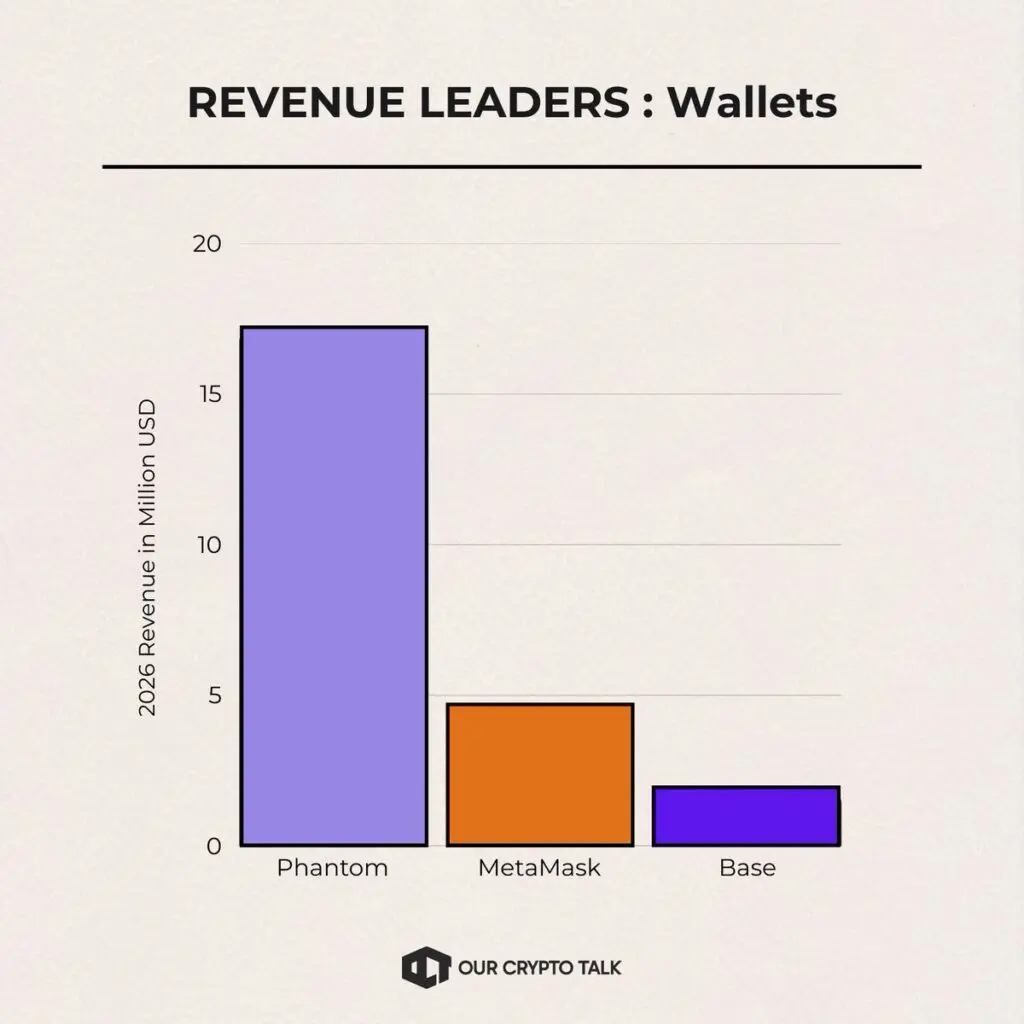

Phantom leads the wallet category decisively. It generated over $17 million in recent revenue and has accumulated hundreds of millions in lifetime fees.

Its user base expanded rapidly alongside Solana’s growth, reaching tens of millions of active users. Phantom’s strength lies in comfort: users trust it, stay inside it, and once that happens, monetization becomes seamless. Swaps feel native. Stablecoins feel integrated. Perpetuals feel accessible. The integration with Hyperliquid in 2025 alone drove billions in volume and meaningful fee capture, solidifying Phantom’s position as a revenue leader.

Phantom placed revenue opportunities directly in front of users, making monetization seamless. MetaMask operates differently. With over 30 million monthly active users, it benefits from default status across EVM chains. Its revenue from swaps and bridges remains substantial even without rapid innovation. Habit is its moat.

Base App demonstrates how ecosystem alignment drives revenue. As Base adoption grows, wallet usage follows. Revenue becomes a byproduct of chain growth rather than wallet superiority. The long-term trend is clear: wallets are evolving into vertically integrated financial apps. As non-custodial markets expand, wallet revenue will continue to grow even as competition intensifies.

Lending no longer dominates crypto headlines, and that is intentional. Excess leverage nearly broke the system in previous cycles. What remains in 2026 is a leaner, more conservative version of on-chain credit, offering stable returns without the extreme volatility of earlier cycles.

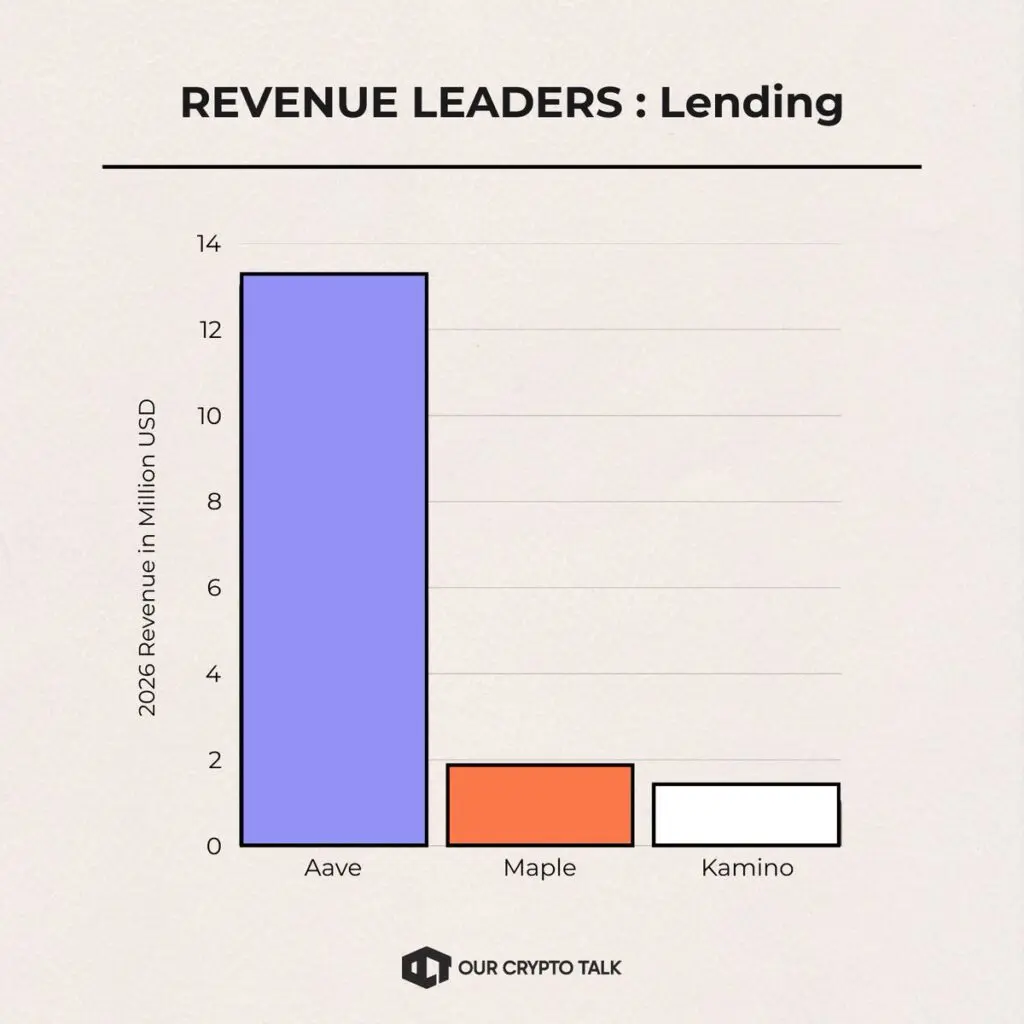

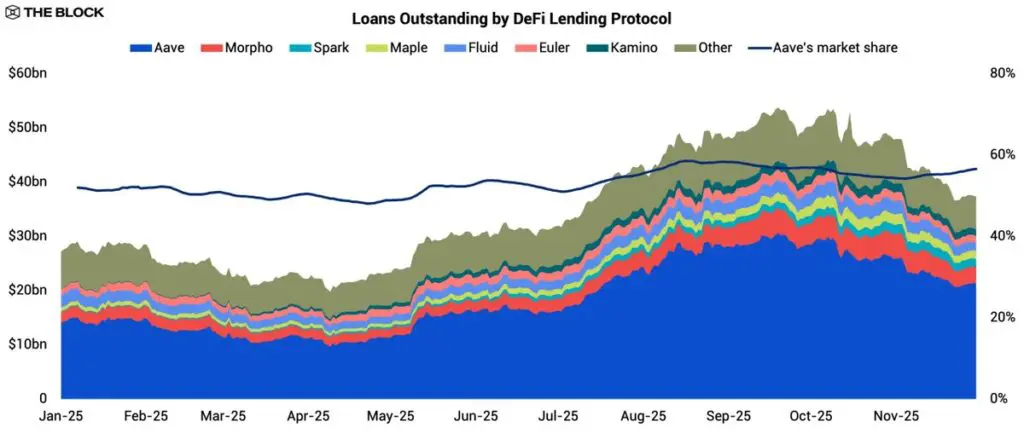

Aave continues to dominate the lending sector. It generated over $13 million in recent fees and facilitated tens of billions in loans. Its strength lies in predictability. Multi-chain deployment, deep liquidity, and conservative risk parameters make Aave a reliable platform for both retail and institutional users.

This reliability drives dominance. Institutions and sophisticated traders consistently prefer stability over novelty, ensuring that Aave maintains its position as the top lending protocol in 2026.

Maple Finance occupies a unique niche in crypto lending. Focusing on institutional credit and structured lending, its assets under management expanded rapidly, and revenue followed. Partnerships with other DeFi protocols and traditional financial entities helped Maple reach meaningful scale.

Kamino represents chain-specific lending. By integrating with Solana-based DeFi and leveraging looping strategies, it generated consistent fees. Lending in 2026 is becoming more contextual, tailored to specific ecosystems rather than attempting a one-size-fits-all approach. The key takeaway: lending survived by shrinking, and what remains now is closer to real finance.

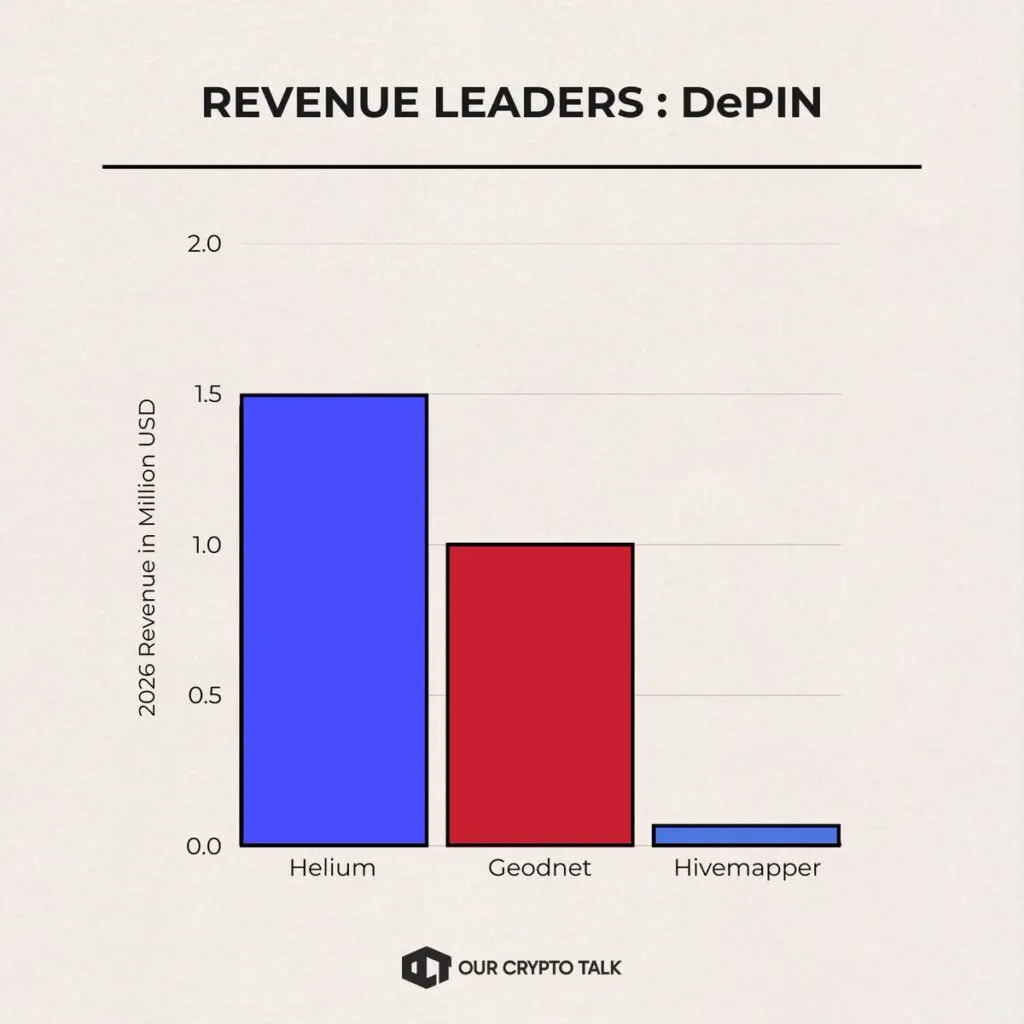

DePIN (Decentralized Physical Infrastructure Networks) is one of the most ambitious crypto narratives. It seeks to rebuild physical infrastructure using decentralized incentives, but monetization is difficult.

Hardware deployment, geographic coordination, and enterprise adoption all move slowly. Most DePIN projects remain speculative because they have not yet crossed the revenue threshold. Only a few, like Helium and Geodnet, are generating meaningful income in this sector.

Helium generates revenue by providing real-world services. Affordable mobile plans and carrier offload services create repeatable demand. Subscribers pay monthly, and data usage translates directly into fees. The network also burns credits as usage grows, aligning tokenomics with utility.

Despite token price volatility, Helium expanded its user base and geographic footprint. Revenue grew consistently, even as incentives shifted toward network expansion.

Geodnet follows a similar model in a specialized market. It sells precision geospatial data used in surveying, drones, and navigation. Enterprises pay for access, and a significant portion of revenue is funneled into token buyback and burn mechanisms, linking usage to value capture.

By steadily expanding its global station network and enterprise customer base, Geodnet achieved revenue growth even when token prices underperformed.

Most DePIN projects fail because they lack repeatable customers. Without consistent demand, monetization remains elusive. Helium and Geodnet demonstrate that once real-world usage exists, revenue follows—even if speculative interest fades.

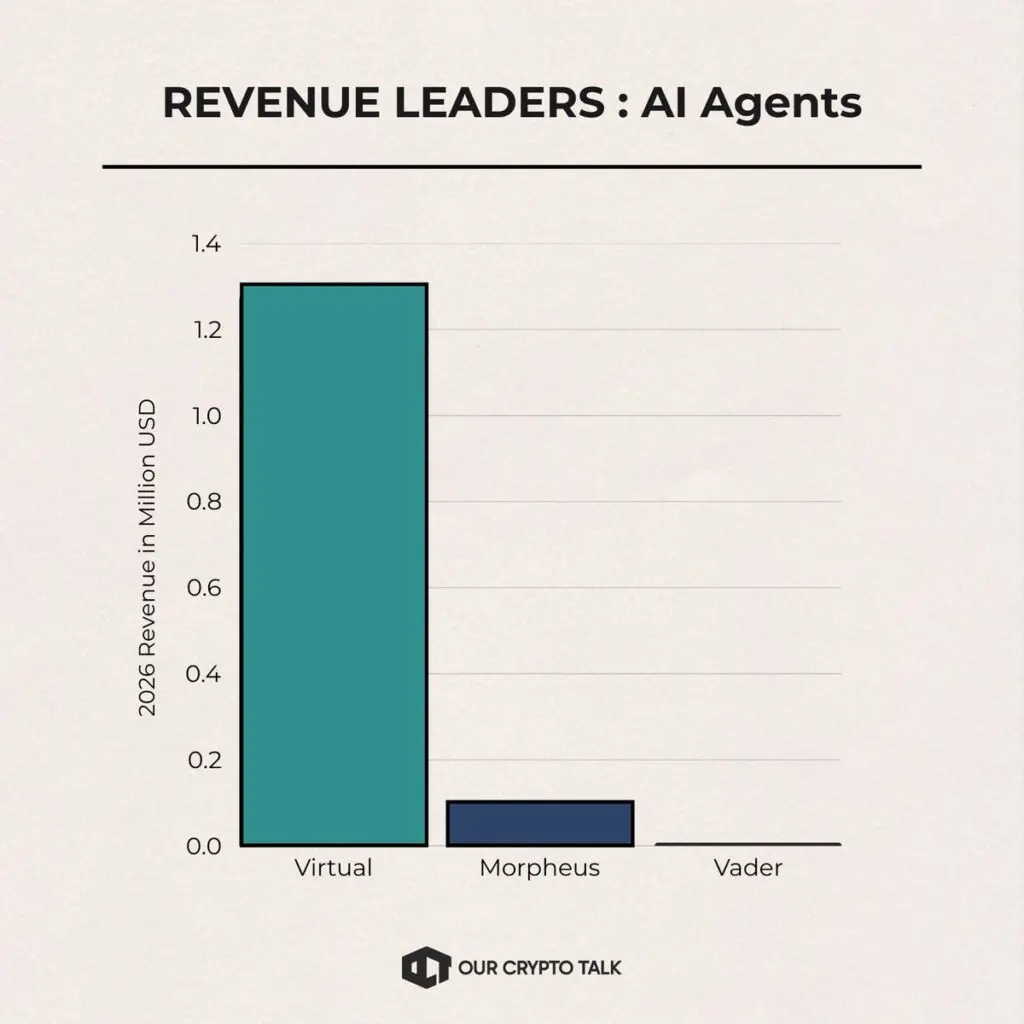

AI dominates crypto discussions but barely contributes to meaningful revenue. This gap is structural. Most AI projects prioritized building capabilities over establishing clear economic models. They launched agents, tools, and frameworks, but usage often does not translate into payment. Monetization remains a challenge for the sector in 2026.

Virtuals Protocol stands out among AI projects. The platform focuses on agent ownership rather than mere access. Agents can be launched, monetized, and co-owned, allowing revenue to flow as they perform tasks and generate value.

This model aligns incentives better than most AI projects. While overall AI revenue remains low in 2026, Virtuals demonstrates how the agent economy could eventually produce meaningful cash flow. Most AI projects are still early, and their business models have not yet caught up to the technology.

Across all top-performing crypto projects, the same traits repeat. Leaders monetize existing behavior, remain close to capital flows, reduce friction, and do not rely on token emissions to survive. Once revenue appears, dominance forms quickly. Liquidity attracts liquidity, distribution attracts more distribution, and trust compounds. Most narratives never reach this stage and remain experimental.

The market now rewards projects that can self-fund, retain users organically, and scale without dilution. Narratives still matter, but only when they translate into payments. If you want to understand where crypto is heading, stop watching price alone. Focus on who gets paid—that is where long-term survival and success truly lie.

All the opinions in this article are that of the author and in no way are financial advice. Our Crypto Talk and the author always suggest you do your own research in crypto and to never take anything as financial advice that you read on the internet. Check our Terms and conditions for more info.

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?

What If Satoshi Nakamoto Was Here in 2026?

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Where Crypto Actually Makes Money in 2026?

What If Satoshi Nakamoto Was Here in 2026?