Loading Search...

The State of DeFi is evolving within a fragmented global financial order, shaped by geopolitics, stablecoins, and energy constraints.

We are living through a fragmentation of the global financial order, not in theory, but in practice. The dollar still dominates, but payment systems are splitting, capital controls are spreading, and energy short supply is reshuffling the card on who can power what. World leader are marking the end of the post-WWII geopolitical state. This context defines the current State of DeFi.

DeFi is not just an experiment: it could become the neutral ecosystem that connects a world no longer united by trust.

This isn’t about hype or price charts. It’s about structural change and in this piece, I’m diving deep into what most analysts still don’t want to talk about when discussing the State of DeFi.

DeFi TVL market is priced today at ~$100B with ~100,000 daily active addresses, comparatively mobile fintech market is priced at $2T, PayPal account for 436M active accounts (implying millions daily); Stripe: Powers millions of businesses/merchants and Neobank holds $2.4T AUM. No need to say that DeFi is still in it’s early age, as @0xKolten said “If DeFi is going to grow, it needs to pursue the everyday users who make fintech massive”.

So the real question becomes:

What kind of global environment would actually allow DeFi to capture those flows, and can it truly scale beyond

Read it on my DeFI Hub

At first, we see that users adopt digital currency in different regions than those that fund and build it, a key dimension of the current State of DeFi. In Q3 2025, ~75% of total global funding activity “$8.4Bn” on digital asset & currency ”DA&C” start-up went to northern countries, which account for 47% in US, 28% in UK.

Those observations shows how on-chain activity is growing fast in developing countries. It shows that in times of stress, the permissionless and neutral settlement of digital currencies makes them especially attractive.

Sources : Chainalysis & Galaxi report

This geographic imbalance raises an important point. Adoption and usage are accelerating in regions facing monetary instability or structural stress, while capital and institutional funding remain concentrated in developed financial centers. In other words, the demand side and the funding side of DeFi are not perfectly aligned, a core tension shaping the State of DeFi today.

Understanding this tension is essential. Because while on-chain activity may be strongest where financial systems are weakest, the capital shaping the ecosystem is still largely coming from mature economies. That gap helps explain why DeFi appears both dynamic and constrained at the same time.

Which brings us to its current stage of development :

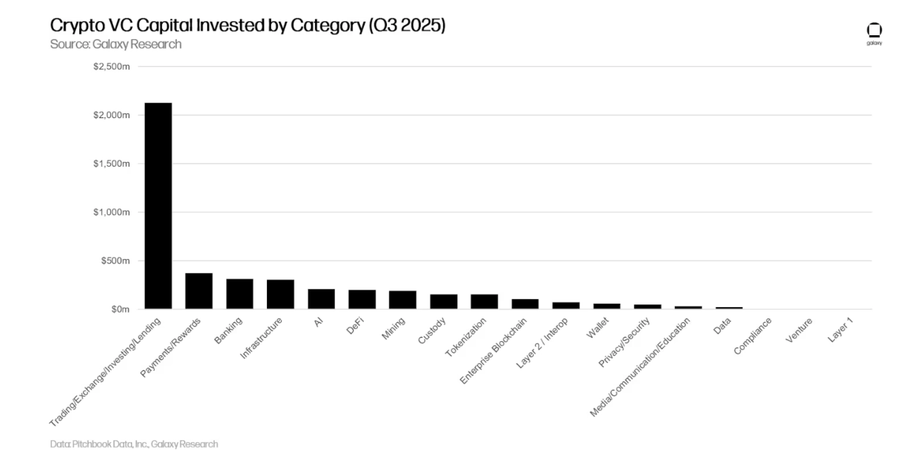

“DA&C” sector is in 2025 the sector with the highest funding activity, showing true interest. Exchange got most funding by far with $500m for Kraken and $1Bn for Revolut. The rest of sectors are put aside, investors seems to not be convinced yet of DeFi potential, seeing it as unmature, still in development phases. The digital asset attraction is here but DeFi seems to lack visibility towards the end user, another limitation in the State of DeFi today.

The lack of visibility is coming from 2 directions, the first is a lack of maturity and battle testing inherent to protocol competence to gain market share. The second has everything to do with it’s conceptual ideology. DeFi doesn’t respond to the need of the developed democracy’s societies but rather to the developing countries where they are economically instable, most people are unbanked and the population is tech savvy/younger. This correlate with the on-chain footprint being higher in 3rd tier countries.

Looking at economy statistic we observe that rich countries tend to have older population in which Baby Boomers (61y-79y) and Generation X*(45y-60y)* owns >60% of the total country wealth. Hard to imagine this population invest or even build into a non-centralized system. You can check yourself this data in your X analytics, if your account is fully oriented CT, you probably have most of your audience as younger generation “<45y”.

It is this misalignment between the need of Retails from centralized capitalist countries and DeFi ideology which block growth (partly). The lack of maturity is also a blocking factors as most of the TVL from DeFi is staked token heavily correlated to BTC variation. As time pass, ETF makes BTC, ETH and SOL correlated to the real economy, yield bearing stablecoin and RWA are growing at fast paste and law enforcement sending green light signal for serious actor like institutions to jump in. Those are reason to believe DeFi is maturing.

Galaxy Research data shows that in Q3 2025, 57% of crypto VC capital went to later-stage companies, a clear sign that DeFi is maturing, as investors are increasingly funding, scalable protocols rather than early-stage experiments.

DeFi may be maturing at the protocol level, but maturity alone does not determine direction. The real question is what kind of monetary system it is integrating into, and whether it is reinforcing that system or quietly reshaping it.

Because as DeFi grows, it does not operate in a vacuum. It expands inside a global currency framework dominated by the dollar, shaped by sanctions, and increasingly defined by geopolitical competition. And nowhere is this more visible than in the rise of stablecoins.

Which brings us to the deeper layer beneath DeFi’s growth story: the monetary battlefield itself.

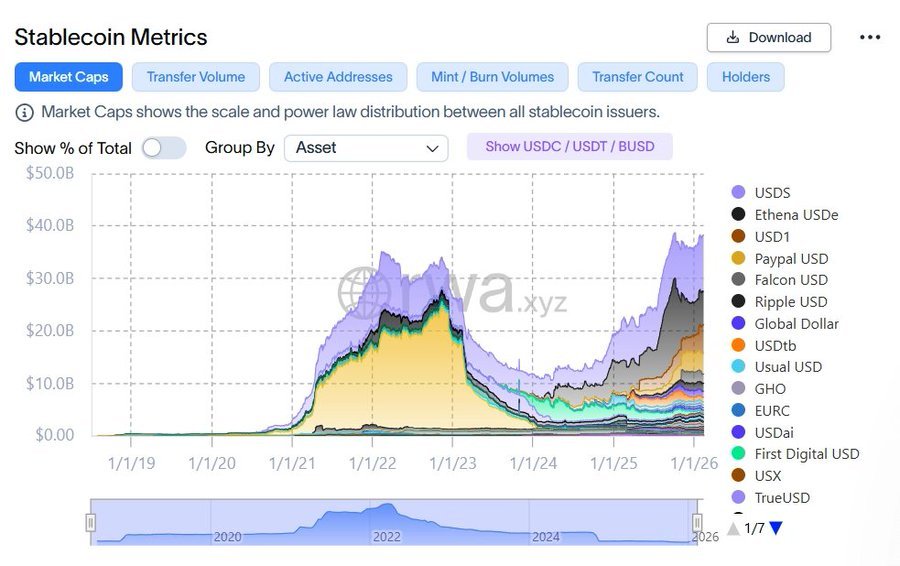

You’ve probably seen the chart a thousand times by now. The one showing the explosive rise of stablecoin market cap. The one usually saying: “ look DeFi is growing.”

And at first glance, it looks undeniable. Stablecoins have expanded massively over the last few years. Billions upon billions in circulating supply. Record on-chain volumes. Increasing integration across exchanges, protocols, and payment flows.

But here’s what’s almost always omitted.

Most of that growth is not decentralized.

The overwhelming majority of stablecoin expansion has been concentrated in centralized, state-regulated issuers, primarily USDT and USDC. These are corporate entities, operating under legal jurisdictions, compliant with sanctions regimes, capable of freezing funds, blacklisting addresses, and responding to government directives. They are not neutral protocols.

USDT alone accounts for more than 70% of stablecoin trading volume. That includes centralized exchange activity, perpetual futures markets, cross-border transfers, remittances, OTC settlement etc. In other words, most of what is being labeled as “DeFi growth” is actually liquidity built on top of centralized monetary infrastructure.

Is this DeFi growing, or is it just the dollar extending itself into crypto rails?

When we look at truly decentralized stablecoins, the ones governed by smart contracts rather than corporate boards, the story is very different. Protocol with algorithm designs like USDS or USDe have not experienced the same exponential curve. They haven’t exploded in dominance. At best, those true decentralized stablecoin have been multiplied mostly.

They exist. They function. But They have not yet captured a substantial share of the market.

Dollar dominance vs fragmentation

Centralized stablecoins grow faster because they fit comfortably within the current geopolitical framework. They cooperate closely with regulators and maintain reserves within traditional banking systems. Because of this structure, they can be audited, frozen, sanctioned, and integrated into existing financial frameworks. Rather than threatening state control over money, these mechanisms ultimately reinforce it.

They are permissionless, composable, transparent, capital efficient, decentralized. In short, they do not “bow” to sovereign directives. That is precisely why they face resistance.

The global financial order today is increasingly fragmented. The United States remains at the center, with the dollar as a base layer in trades, debt markets, energy contracts, and reserve allocations. Stablecoins denominated in USD effectively export dollar liquidity into crypto markets.

In that sense, American regulatory tolerance toward centralized stablecoins serves a strategic purpose: it extends dollar influence into the permissionless layer of the internet. But this expansion is not neutral.

For other countries, crypto, especially dollar-backed stablecoins, represents a challenge to monetary sovereignty. If citizens and businesses transact in digital dollars rather than local currencies, domestic policy tools weaken. Capital controls become harder to enforce. Sanctions regimes become more complex.

What we are witnessing is not merely a technological transition. It is a form of monetary competition, arguably a new kind of forex war.

In that environment, decentralized finance occupies a strange position. On one side, centralized stablecoins extend dollar dominance through crypto infrastructure. On the other, truly decentralized systems offer the possibility of something more “international”: a foreign exchange market native to the blockchain, where any currency (not just USD) can be represented, traded, and settled without geopolitical imposition.

If DeFi fulfills that vision, it does not become an instrument of a single state. It becomes a neutral settlement layer. This represents one possible trajectory for DeFi’s evolution

Monetary fragmentation, however, does not happen in isolation. Currency dominance, sanctions power, and financial infrastructure ultimately rest on something more fundamental: economic capacity. And economic capacity, in modern economies, is inseparable from energy.

If finance is the surface layer of global power, energy is the foundation beneath it. The ability to issue currency, sustain digital infrastructure, and expand financial systems depends on access to reliable and affordable energy. Which means that any discussion about DeFi’s long-term trajectory must also account for the physical systems that make it possible.

This brings us to the deeper constraint behind monetary competition: energy itself.

The U.S. leads DeFi not just through regulation, but through energy consumption, and crypto runs on electricity supply / energy. Bitcoin, validators, and data centers depend on cheap, abundant power. The countries with the lowest-cost and most reliable energy will ultimately shape where blockchain infrastructure lives and grow.

But the U.S. is not the one holding major energy capacity, in that sens it have everything to gain at cooperating with other countries and not imposing their dollar to the world. As energy becomes more strategic and scarce, nations increasingly protect their resources, reinforcing a fragmented global order. In that environment, DeFi could evolve into neutral “peace rails,” leveraging its composability to facilitate fairer international trade and align incentives between countries rather than deepen competition.

Much of modern economic theory historically treated natural resources as secondary or substitutable inputs. Coming back to 1723 with Adam Smith, Jean-Batiste Say, Ricardo to 1956 with Robert Solow, claiming that natural resources aren’t a big deal ! They argued that natural resources could be ignored or treated as substitutable; Solow even claimed that ‘the world can, in effect, get along without natural resources.

Recent energy data increasingly challenges those thinkers assumption, which raises important questions about the long-term sustainability of growth models heavily reliant on expanding energy consumption. Modern economic growth requires abundant energy; GDP per capita correlates directly with energy per capita. Global growth in OECD economies has slowed since the 1980s, with some analysts pointing to energy constraints as the main contributing factor.

GDP≈Energy Efficiency×Energy Consumed

(efficiency improves slowly at ~0.8%/year)

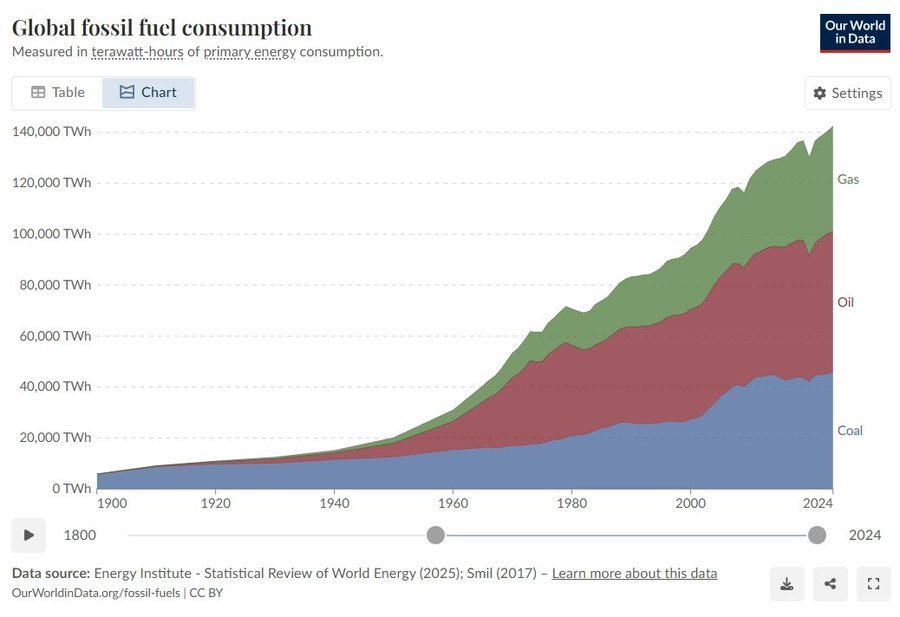

Global primary energy consumption reached a new record high in 2024, growing ~2% YOY (faster than the 2013-2023 average of 1.3%). Electricity demand surged >4%. Fossils still dominate ~80-85% of the mix, with renewables (excluding hydro) at ~7.3%, hydro ~2.7%, and nuclear ~5.1%. Non-OECD countries (especially Asia) drive nearly all growth.

At current consumption levels, fossil fuel reserves are estimated to last roughly 50 years (coal not included). While alternative energy sources exist “most notably nuclear“ , their ability to fully offset this decline remains limited.

Uranium resources are themselves finite, with estimates suggesting 90 to 100 years of supply, and nuclear energy currently accounts for less than 10% of global energy consumption. To better support this assumption, the NEA forecasts that under realistic scenarios, uranium resources would last until around 2100.

Other renewable energy sources, while essential to the transition, are not yet sufficient to meet long-term global energy demand on their own and remain constrained by intermittency and efficiency limitations (see the 2025 summer blackout in Portugal / Spain ).

If current reserve and demand trends continue without meaningful technological breakthroughs, structural energy constraints could slow down global economic growth

By extension, sectors such as DeFi, AI, and broader fintech (all of which rely on expanding digital infrastructure) depend on sustained and affordable energy supply. If energy growth becomes harder to achieve, the assumption of indefinite expansion across these sectors becomes increasingly difficult to sustain. Energy supply limits DeFi growth and, by extension, global economic growth this cannot continue indefinitely.

Quick note for the people saying “some years scientist are saying 10y left. Then the year later 50y left … they are just lying”. Fossils energy is not 1 entity it is 3 different natural resources with different “time to maturity” like the graph is showing.

As we observe, tensions surrounding energy access and resource control have already increased geopolitical friction (USA’s intervention in Venezuela highlight tension regarding energy control) and battle for energy resources have escalated. This political tension is also a threat to peace and economic expansion. Some analysts interpret recent interventions as the renewal on Monroe doctrine and the end of the international law norms.

Countries with the largest fossil fuel reserves: Venezuela and Saudi Arabia sit atop global oil reserves, while Russia and Qatar are key gas holders; meanwhile the U.S., China, Australia, and India control significant coal reserves that still power much of the world’s electricity system … will heavily shape how the energy transition unfolds.

I believe these nations have everything to gain by trading energy through neutral infrastructure, laying the foundation to cope the potential energy shortfalls of the century to come, putting cooperation first rather than competition in a fragmented global order.

DeFi will not win because it is neutral. It will win if it becomes more efficient, reliable, and economically aligned than the systems it seeks to complement. The global order is fragmenting, the demand for neutral infrastructure is rising.

The open question is whether DeFi can mature fast enough to meet that demand.

I hope this piece will help you shape a better view on how DeFi could develop from a macro perspective, my vision is my own feel free to use it to build yours. I share about strategy, concept and protocol with great new ideas.

Finance & DeFi - Yield wizard | Stablecoin risks & LP strats | Macro analysis

https://t.co/sRIG59xi0U