Loading Search...

The U.S. SEC issued a 68-page interpretive release that officially classifies 18 named crypto assets as digital commodities.

Author: Sahil Thakur

17th March 2026 — The U.S. SEC issued a 68-page interpretive release that officially classifies 18 named crypto assets as digital commodities, not securities under federal law.

High Signal Summary For A Quick Glance

Chad Steingraber

@ChadSteingraber

We have the official list of Digital Commodities from the SEC🔥 APT, AVAX, BTC, BCH, ADA, LINK, DOGE, ETH, HBAR, LTC, DOT, SHIB, SOL, XLM, XTZ and XRP.✅ Here's how Commodities are taxed: Commodities are generally taxed as capital assets, with futures contracts commonly https://t.co/W5FY2NJICk https://t.co/mLJKsnl6hV

Today the SEC released clarifying interpretation of federal securities law applying to "certain crypto assets and transactions". “It also acknowledges what the former administration refused to recognize – that most crypto assets are not themselves securities. And it reflects the https://t.co/IVL4Z5o8T1 https://t.co/FOkY3ngy9F

10:33 PM·Mar 17, 2026

Mark

@markchadwickx

🚨HUGE: The SEC and CFTC just released joint guidance on Crypto Classification - one of the clearest signals yet on how it will be treated going forward. Highlights: - Digital commodities (BTC, ETH, SOL, etc.) → CFTC oversight - NFTs / collectibles → generally outside https://t.co/VDWAFECZHv https://t.co/g9ct1wirmU

🚨JUST IN: The @SECGov and @CFTC have issued joint, Commission-level interpretive guidance outlining how federal securities laws apply to certain crypto assets and transactions. This follows a submission to OIRA earlier this month signaling the agencies’ intent, and was approved https://t.co/zMxHSlZUNB

08:09 PM·Mar 17, 2026

Paul Atkins

@SECPaulSAtkins

After more than a decade of uncertainty, this interpretation will provide market participants with a clear understanding of how the SEC treats crypto assets under federal securities laws. This is what regulatory agencies are supposed to do: draw clear lines in clear terms. https://t.co/wij5cA7N2i

TODAY 🚨: The Commission issued an interpretation that clarifies the application of federal securities laws to crypto assets. This is a major step to provide greater clarity regarding the Commission’s treatment of crypto assets. Read the release here: https://t.co/DDykVLHZQI https://t.co/zbLFS2JH6g

08:05 PM·Mar 17, 2026

High attention and emotional sentiment detected.

The Commodity Futures Trading Commission formally joined the document. Both agencies committed to enforcing their respective frameworks consistently with the new classification.

The release, titled “Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets,” carries Release Nos. 33-11412 and 34-105020. It took effect immediately.

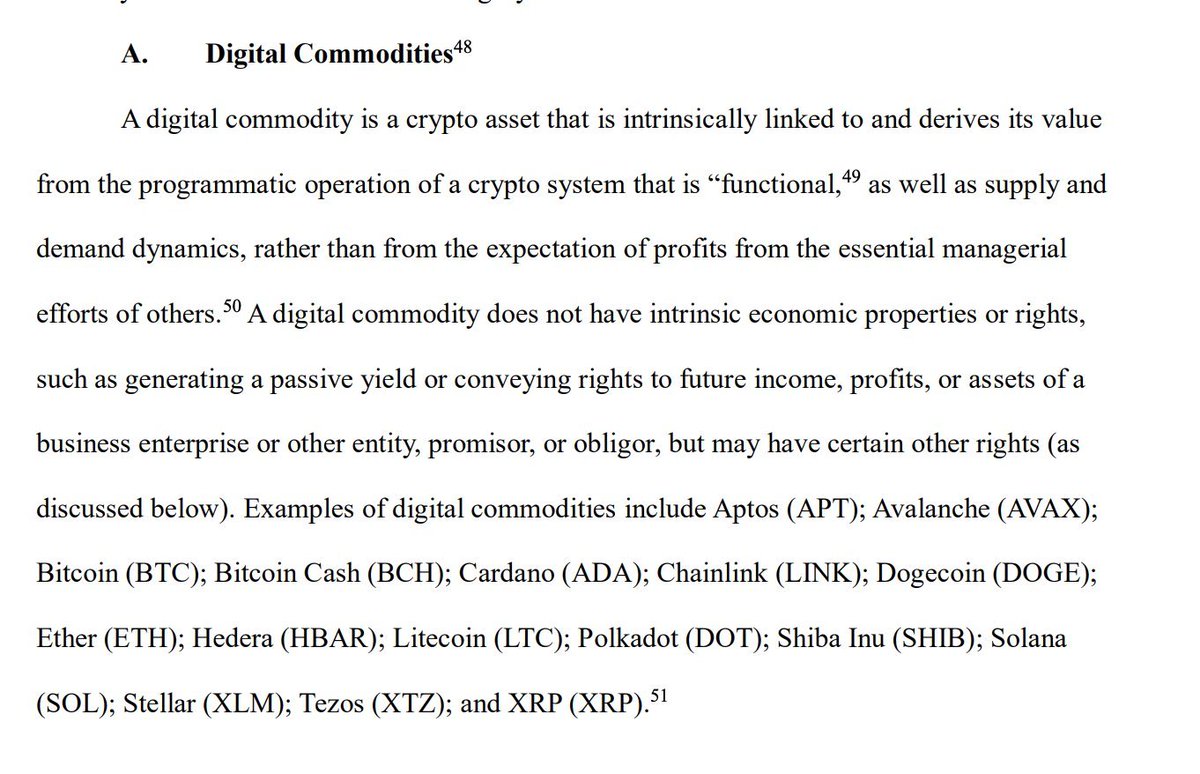

The SEC explicitly named 16 crypto assets as digital commodities: Aptos, Avalanche, Bitcoin, Bitcoin Cash, Cardano, Chainlink, Dogecoin, Ether, Hedera, Litecoin, Polkadot, Shiba Inu, Solana, Stellar, Tezos, and XRP. Additional examples include Algorand and LBRY Credits, bringing the total to 18.

Several of these tokens were previously the subject of SEC enforcement actions or investigations. Solana, XRP, and Cardano all faced scrutiny under former Chair Gary Gensler. They are now officially classified as commodities.

The release defines a digital commodity as “a crypto asset that is intrinsically linked to and derives its value from the programmatic operation of a crypto system that is ‘functional,’ as well as supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others.

In practical terms, the asset must serve a programmatic function within its network. It cannot offer passive yields or rights to profits from an enterprise. Decentralization is noted as a factor but is not a strict requirement.

Source: US SEC

The document introduces a formal token taxonomy with five categories. Digital commodities cover functional crypto assets like Bitcoin and Ether. Digital collectibles cover non-fungible tokens. Tools cover utility tokens used within specific ecosystems.

Payment stablecoins fall under the framework outlined in the GENIUS Act. Digital securities remain subject to federal securities laws and SEC registration requirements.

Under former SEC Chair Gary Gensler, who served from April 2021 to January 2025, the agency pursued what critics called “regulation by enforcement.” The SEC initiated 125 cryptocurrency enforcement actions during that period, imposing $6.05 billion in monetary penalties.

Gensler maintained that most crypto tokens qualified as investment contracts under the Howey test. That position drove major actions against Ripple, Coinbase, Binance, and Kraken, among others.

The new release explicitly rejects that broad approach. It states that “most crypto assets are not themselves securities” and acknowledges that investment contracts can begin and end once a crypto system becomes sufficiently functional.

The release followed more than a year of deliberate groundwork. President Trump signed an executive order in January 2025 establishing a Presidential Working Group on Digital Asset Markets. That group published a 160-page report in July 2025 with over 100 recommendations.

The SEC launched “Project Crypto” in July 2025, which became a joint initiative with the CFTC in January 2026. Over 300 public submissions informed the final document.

On March 11, 2026, the two agencies signed an updated Memorandum of Understanding replacing the 2018 version. The MOU established a Joint Harmonization Initiative focused on reducing duplicative rules and coordinating crypto oversight.

SEC Chair Paul Atkins said the interpretation “will provide market participants with a clear understanding of how the Commission treats crypto assets under federal securities laws.” He added: “This is what regulatory agencies are supposed to do: draw clear lines in clear terms.”

Atkins also proposed a token safe harbor, described as a “fit for purpose startup exemption.” The safe harbor would allow crypto entrepreneurs to raise funds or operate for a defined period while exempt from SEC registration rules.

The release addresses several related activities. Protocol staking and mining are generally not considered securities transactions under the new framework. Wrapping a non-security crypto asset does not convert it into a security.

Airdrops are analyzed under the Howey test. Free distributions that do not involve an investment of money generally do not create securities obligations.

The classification removes one of the largest barriers to institutional participation in U.S. crypto markets. Spot Bitcoin ETFs have attracted $57.7 billion in net inflows since launching in January 2024. Spot Solana and XRP ETFs debuted in late 2025 and have drawn $92 million and $883 million respectively.

More than 126 crypto ETF applications are currently pending with the SEC. Bitwise projects that over 100 new crypto ETFs could launch in 2026.

With clear commodity classification for assets like Cardano, Chainlink, and Polkadot, additional spot ETF products targeting those tokens could move forward.

The interpretive release is not legislation. It serves as an interim framework while Congress advances two key bills. The CLARITY Act would grant the CFTC exclusive jurisdiction over digital commodity spot markets. The GENIUS Act would establish the first federal regulatory framework for payment stablecoins.

Both bills are working through committee. A future administration could technically reinterpret the release, though it carries significant weight as a Commission-level document approved by both agencies.

The release supersedes the SEC staff’s 2019 Framework for “Investment Contract” Analysis of Digital Assets. It invites public comments for refinement and does not create new statutory authority.

Tokens not named in the release may still qualify as digital commodities if they meet the stated criteria. The definition of a “functional” crypto system leaves room for case-by-case analysis on borderline assets.

For the 18 named assets, the regulatory picture is now clear. Secondary trading, staking, and related activities no longer face securities-law risk. Primary oversight for these assets shifts to the CFTC as commodities under the Commodity Exchange Act. This article does not constitute financial advice.

Our Crypto Talk is committed to unbiased, transparent, and true reporting to the best of our knowledge. This news article aims to provide accurate information in a timely manner. However, we advise the readers to verify facts independently and consult a professional before making any decisions based on the content since our sources could be wrong too. Check our Terms and conditions for more info.