Loading Search...

Crypto bear market failures reveal why major projects collapsed. Explore top crypto crashes, causes, and lessons from past bear markets.

Author: Kritika Gupta

Crypto Bear Market Failures reveal the true stress points of the digital asset industry. Cryptocurrency markets move in dramatic cycles of euphoria and despair. During bull markets, innovation accelerates, valuations expand rapidly, and adoption spreads quickly. In contrast, bear markets often described as crypto winters bring prolonged price declines, liquidity shocks, and widespread investor capitulation.

Historically, these downturns appeared in 2014–2015, 2018–2019, and 2022–2023, with continued volatility afterward. Importantly, each bear market functions as a stress test. It exposes overleveraged balance sheets, unsustainable business models, weak governance, and, in some cases, outright fraud. As a result, projects that appeared resilient during bull markets often fail once market conditions tighten.

While strong teams continue building through downturns, many others dissolve entirely. Teams abandon development, platforms shut down, tokens collapse toward zero, and billions in value disappear. These failures range from early Bitcoin exchanges to complex DeFi protocols and large centralized platforms.

Most crypto bear market failures do not result from a single flaw. Instead, they emerge from compounding economic, operational, psychological, and regulatory pressures that remain hidden during bull cycles.

However, when prices collapse, often by 70 to 90 percent for Bitcoin and more than 95 percent for many altcoins, revenues disappear rapidly. At the same time, funding dries up and users withdraw en masse, creating bank run dynamics. Consequently, weaknesses that seemed manageable during expansion become fatal during contraction and the key reasons include:

Liquidity and Funding Drought:

First, many projects rely on constant capital inflows. Lending platforms promising double-digit yields, ICOs with vague roadmaps, and DeFi protocols dependent on rising TVL all struggle once new money stops entering the system. Venture capital firms reduce exposure, retail participation declines, and token sales fail. Projects with limited runways often liquidate assets at depressed prices, accelerating insolvency. During the 2018 and 2022 bear markets, numerous teams exhausted treasuries without achieving product-market fit.

Overleveraging and Contagion:

Next, leverage amplifies downside risk. Hedge funds, centralized lenders, and on-chain protocols frequently borrow against volatile collateral. When prices fall, margin calls trigger forced liquidations, creating feedback loops that push prices lower. Algorithmic stablecoins and interconnected lending platforms demonstrate how one failure spreads across counterparties. Without circuit breakers, isolated stress quickly becomes systemic collapse. The 2022 cycle demonstrated how interconnected leverage rapidly magnifies crypto bear market failures.

Revealed Frauds and Scams:

In addition, fraudulent structures thrive during euphoric phases. Ponzi-like yield schemes, mismanaged customer funds, fabricated volumes, and exit scams persist as long as inflows exceed outflows. Once prices fall, withdrawal pressure exposes insolvency. What investors dismissed as fear, uncertainty, and doubt during bull markets becomes undeniable evidence during downturns, leading to shutdowns, legal action, and abandonment.

Operational Unsustainability:

Moreover, high burn rates become impossible to maintain. Lavish marketing, oversized teams, celebrity endorsements, and inflated executive compensation rely on bull-market revenues. When trading activity collapses, fee income and staking yields shrink sharply. Teams that scaled too aggressively often fail to pivot to lean operations, resulting in layoffs or frozen development. Many projects survive only in name, with no active progress.

Regulatory and Reputational Pressure:

At the same time, bear markets attract regulatory scrutiny. As losses mount, regulators respond to investor complaints with investigations, enforcement actions, and license revocations. Negative media coverage spreads quickly, discouraging new users and partners. For already fragile projects, legal costs and compliance burdens accelerate failure.

Psychological Factors:

Finally, sentiment plays a critical role. Fear spreads rapidly on social media, amplifying withdrawal pressure and panic selling. Herd behavior reverses from FOMO to mass exit. Meanwhile, founders and developers often experience burnout, further weakening execution and morale.

These forces rarely act alone. Instead, they reinforce one another, as seen clearly during the 2022 sequence involving Terra, Three Arrows Capital, Celsius, Voyager, BlockFi, and FTX. One collapse undermines confidence in the next, freezing liquidity across the system. Nevertheless, bear markets also reward resilience. Survivors such as Ethereum after 2018, or projects founded during downturns like Solana and Uniswap, highlight the purifying function of crypto winters.

BitConnect launched in 2016 as a lending platform promising up to 1 percent daily returns through an undisclosed trading bot. During the 2017 bull run, aggressive referral marketing and viral promotion pushed BCC to a market cap above $2 billion. However, once the market turned in early 2018, regulators intervened and user inflows slowed.

Texas issued a cease-and-desist order, and BitConnect abruptly shut down its lending program. As a result, BCC collapsed over 96 percent in days. Investigations later confirmed it operated as a Ponzi scheme that depended on constant new deposits. Ultimately, BitConnect became the industry’s most cited warning against guaranteed yields and opaque strategies. No recovery followed, and the project fully dissolved.

Terra launched in 2018 with the goal of building a DeFi ecosystem centered on UST, an algorithmic stablecoin stabilized through arbitrage with LUNA. During the 2021 bull market, Anchor Protocol’s high yields attracted massive capital, pushing LUNA into the top ten by market cap.

However, in May 2022, large UST redemptions broke the peg during a market downturn. The protocol responded by minting enormous amounts of LUNA, which triggered hyperinflation and a rapid collapse. Over $40 billion evaporated within days. Although Terra later launched a fork without UST, confidence never returned. The failure permanently changed how the industry views algorithmic stablecoins and systemic DeFi leverage.

OneCoin promoted itself as a Bitcoin alternative starting in 2014 and spread primarily through multi-level marketing. It raised billions globally despite never running a real blockchain. Instead, it relied on centralized databases and aggressive sales of educational packages.

As the 2017 bull market faded, regulators and journalists exposed the fraud. Founder Ruja Ignatova disappeared in 2017 and remains a fugitive. Once new capital inflows stopped during the bear market, the scheme collapsed entirely. The token became worthless, and all operations ceased. OneCoin stands as one of crypto’s largest frauds and remains a landmark case in how hype-driven narratives unravel when markets turn.

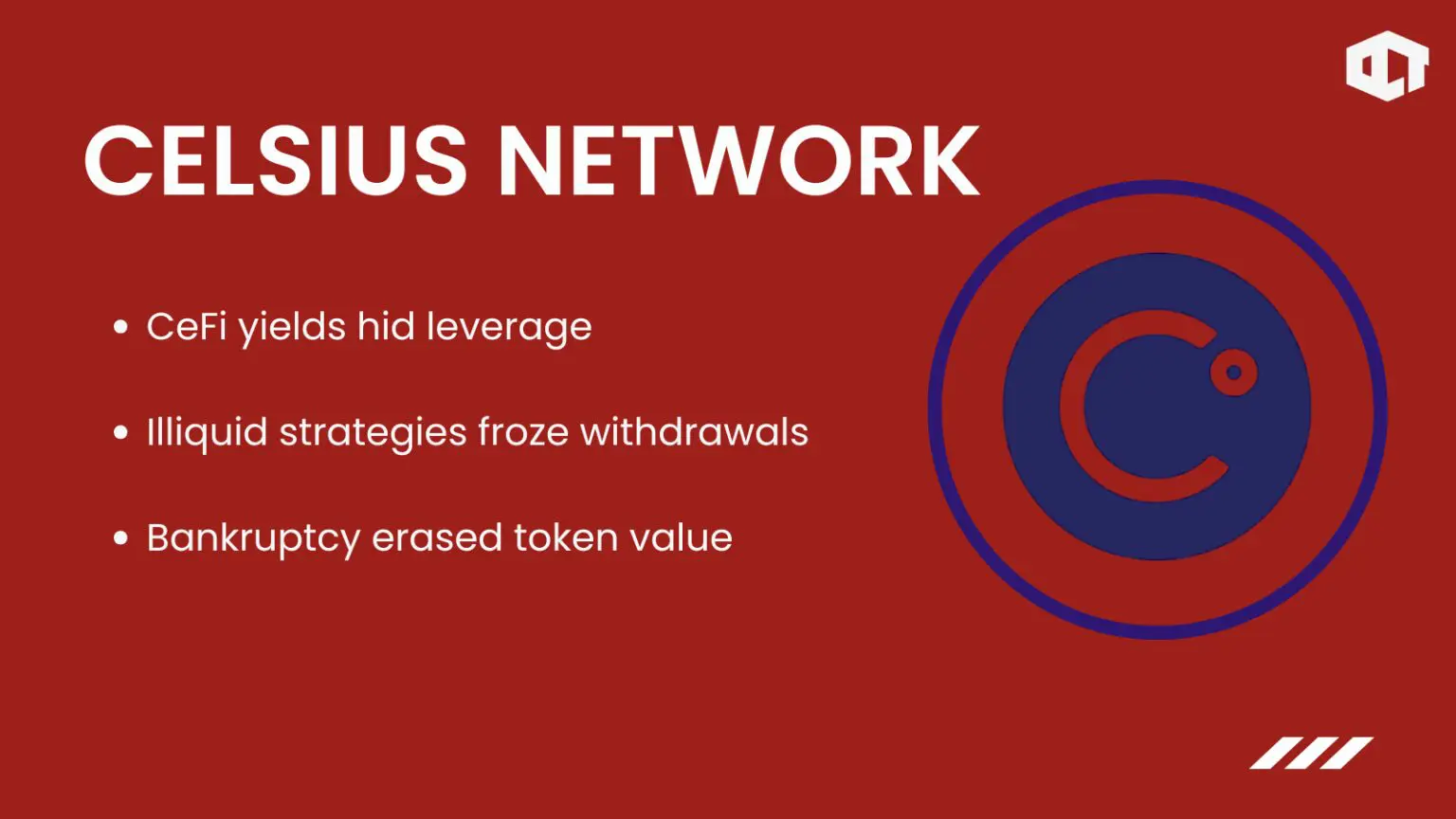

Celsius launched in 2017 as a centralized crypto lending platform offering double-digit yields. During the 2021 bull run, it attracted billions in deposits and promoted the CEL token as a rewards and governance asset. However, Celsius took excessive risk by deploying user funds into illiquid and leveraged strategies.

When the market declined in 2022 and counterparties like Three Arrows Capital defaulted, Celsius froze withdrawals. Shortly afterward, it filed for bankruptcy. CEL lost more than 99 percent of its value. Ultimately, restructuring efforts failed to revive the platform. The collapse exposed the fragility of CeFi yield models that depend on rising asset prices and continuous liquidity.

Voyager entered the market in 2018 as a retail-focused crypto brokerage offering trading, lending, and yield products. It grew quickly during the 2021 bull market and used the VGX token to incentivize users. However, Voyager had heavy exposure to Three Arrows Capital. When 3AC collapsed in 2022, Voyager suffered catastrophic losses.

The platform suspended withdrawals and filed for bankruptcy shortly afterward. Although parts of its assets were later sold, Voyager ceased operating as a business. VGX became effectively worthless. The failure reinforced how interconnected CeFi firms amplified contagion during the 2022 bear market.

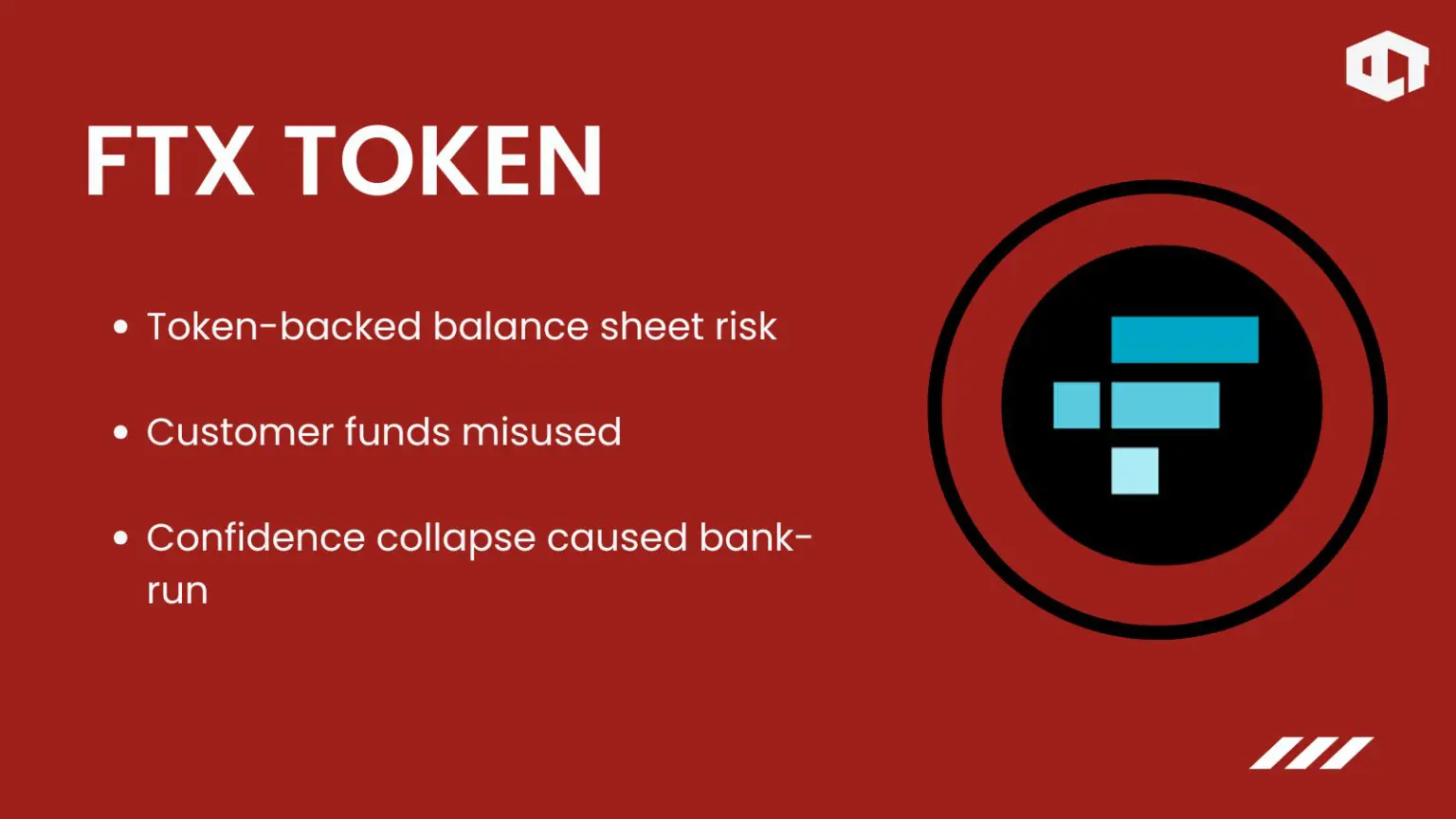

FTT served as the utility token for FTX, which became one of the largest crypto exchanges during the 2021 bull run. The token offered fee discounts and ecosystem benefits and was widely used as collateral. In November 2022, reports revealed that Alameda Research had misused customer funds and relied heavily on FTT’s inflated value.

This revelation triggered a bank-run-style liquidity crisis. FTX halted withdrawals and filed for bankruptcy, while FTT collapsed over 90 percent. Although administrators continue restructuring efforts, the original FTX ecosystem effectively ended. The collapse became one of crypto’s most damaging trust events.

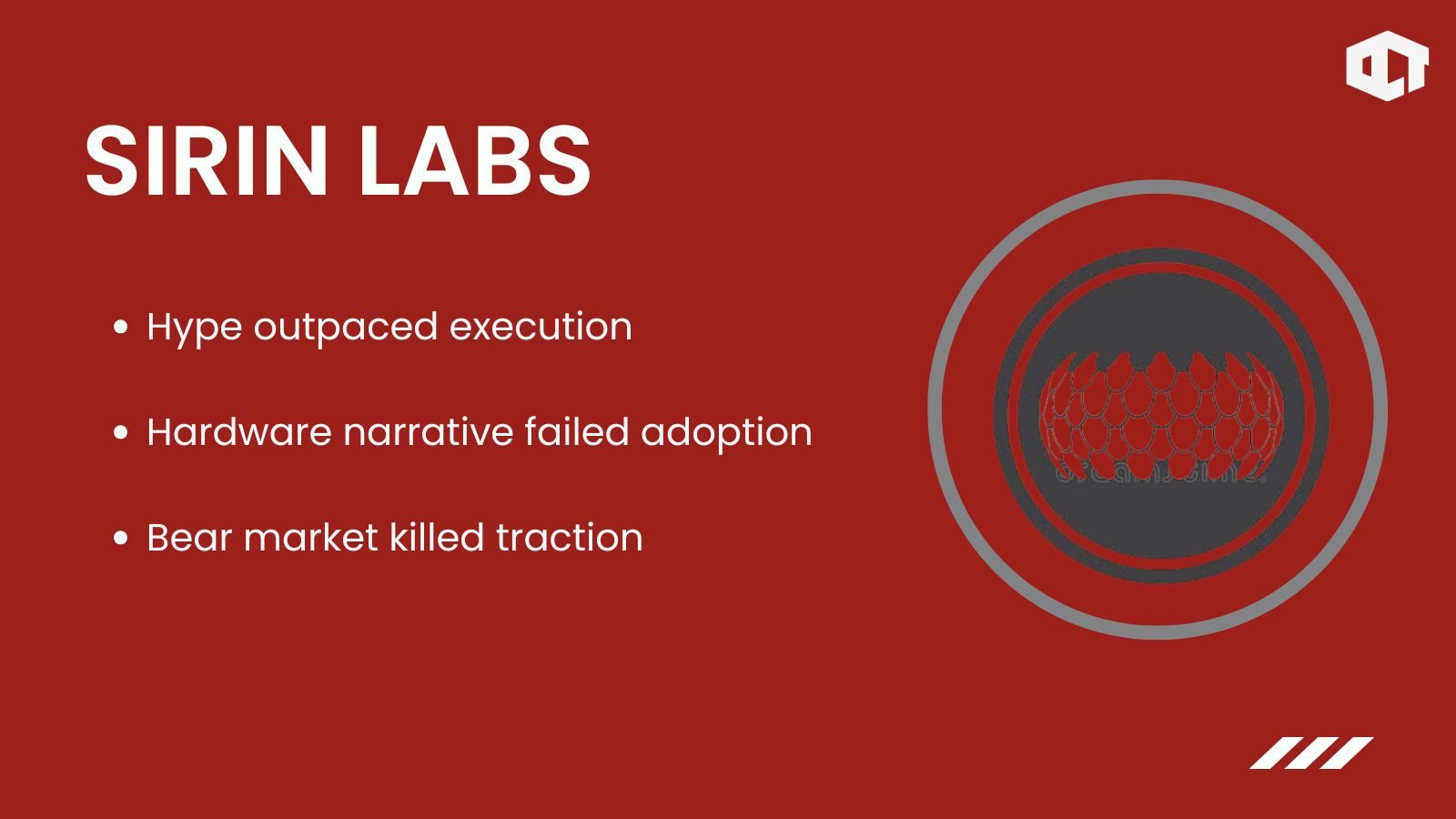

Sirin Labs raised over $158 million in a 2017 ICO to build blockchain-enabled smartphones. During the bull market, the SRN token surged on hype and celebrity endorsements. However, execution faltered once markets cooled. Smartphone sales disappointed, development slowed, and layoffs followed in 2019.

As liquidity dried up during the bear market, SRN lost more than 99 percent of its value and faced delistings. With no viable product traction, the project faded from relevance. Sirin Labs became a textbook case of ambitious hardware narratives failing in crypto downturns.

Veritaseum emerged during the 2017 ICO boom, promising a decentralized capital markets platform. The project raised significant funds but struggled to deliver working infrastructure. Regulatory scrutiny, legal disputes, and alleged security incidents followed. As the bear market deepened, development slowed and communication declined.

VERI collapsed over 99 percent from its peak, and network activity disappeared. Eventually, the project became inactive. Veritaseum reflects a broader pattern from the ICO era where overpromising met regulatory and financial reality during prolonged downturns.

Dragon Coin raised roughly $320 million in 2018 for a Macau-focused casino and payment ecosystem. During the ICO peak, the project claimed major partnerships and regulatory workarounds. However, investigations later revealed false claims and misused funds.

The proposed casino never materialized. When the bear market hit, trading volume vanished and development stopped. DRG rapidly lost value and faded from exchanges. Dragon Coin illustrates how real-world integration narratives collapse quickly when execution and transparency fall short.

GetGems aimed to build a Bitcoin-integrated messaging app with tokenized rewards. Although it gained brief attention during the 2017 bull run, it never achieved meaningful adoption. Once markets turned in 2018, funding dried up and development stalled.

Exchanges delisted GEMZ, and community activity disappeared. The project quietly dissolved. GetGems represents the many utility-token apps that failed because speculation replaced real demand. Bear markets exposed the lack of product-market fit and ended the experiment.

This analysis carries several important limitations. First, it focuses on high-profile failures, which introduces selection bias and may overrepresent extreme outcomes while underweighting quieter project shutdowns. Second, the definition of “dissolved” varies, as some projects rebranded, merged, or continue in limited form, complicating direct comparisons.

Third, public data remains incomplete for many collapses, particularly regarding private lending arrangements and off-chain liabilities. In addition, hindsight bias affects interpretation, as fraud or mismanagement often becomes clear only after failure. Finally, bear markets differ in structure and regulation across cycles, so past patterns do not guarantee future outcomes or risk severity. Any analysis of crypto bear market failures must account for survivorship and hindsight bias.

Crypto bear markets function as harsh but necessary filters. From Mt. Gox to FTX, these failures reveal recurring themes such as excessive leverage, weak governance, centralization risk, and unsustainable incentives. Although they erased enormous value, they also strengthened the ecosystem by forcing higher standards.

For investors, the implications remain clear. Prioritize self-custody, understand incentives, avoid guaranteed yields, and limit leverage. For builders, resilience, transparency, and sustainable economics matter more than growth at all costs. Bear markets may be brutal, but they prepare the foundation for the next phase of crypto’s evolution. Ultimately, crypto bear market failures serve as painful but necessary filters for the industry.

Genome Protocol Rug Pull: Explained

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio

Genome Protocol Rug Pull: Explained

Top 6 ZachXBT Revelations That Shocked The World

AI Agent Payments Explained: Circle Nanopayments and the x402 Protocol

Top 7 Projects in the World Liberty Financial (WLFI) Portfolio