Loading Ratings...

Top 10 Crypto Events That Shaped 2025 examines regulation, institutional adoption, market volatility, and macro forces shaping crypto.

Author: Akshat Thakur

Published On: Wed, 24 Dec 2025 13:37:52 GMT

The Top 10 Crypto Events That Shaped 2025 reflect a decisive transition year for the digital asset sector, defined less by speculative excess and more by structural integration into global financial, regulatory, and macroeconomic systems. After years of fragmented policy signals and cyclical boom-and-bust dynamics, 2025 marked a period where regulation, institutional capital, and geopolitical forces converged to reshape crypto’s role within the broader economy.

Throughout the year, crypto markets responded not only to internal developments such as protocol upgrades and corporate adoption strategies, but also to external macro pressures including monetary policy shifts, trade tensions, and evolving capital market conditions. Bitcoin’s price volatility, rising dominance, and increasing correlation with traditional risk assets underscored crypto’s growing sensitivity to global liquidity and policy expectations rather than purely endogenous narratives.

Understanding the Top 10 Crypto Events That Shaped 2025 is therefore essential not as a historical recap, but as a framework for assessing how digital assets are transitioning from an experimental financial layer into regulated, institutionally relevant infrastructure. These events reveal where structural durability is emerging, where systemic risks persist, and how crypto’s long-term trajectory is being recalibrated.

In 2025, crypto markets operated within a macro environment dominated by shifting interest rate expectations and uneven global growth signals. Rate adjustments by central banks altered liquidity conditions, reinforcing crypto’s increasing correlation with equities and other risk assets rather than isolating it as a purely alternative system.

Regulatory clarity accelerated unevenly across jurisdictions, but the overall direction was toward formal integration rather than suppression. This reduced existential risk for major crypto sectors while simultaneously raising compliance expectations, capital requirements, and institutional standards.

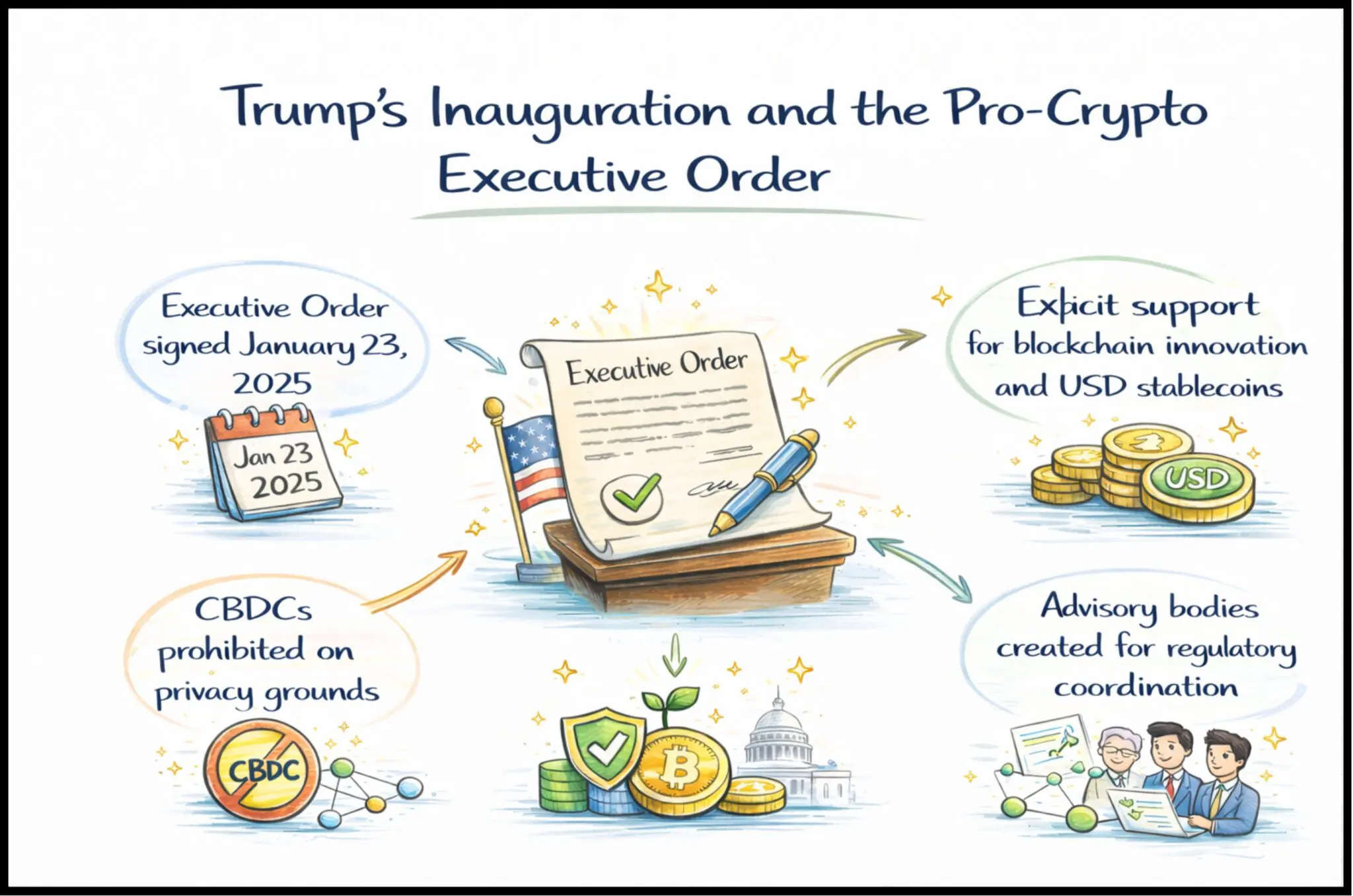

Donald Trump’s return to the U.S. presidency on January 20, 2025, immediately set a markedly pro-crypto tone for the year. On January 23, he signed the Executive Order on Strengthening American Leadership in Digital Financial Technology, signaling a strategic shift in how the U.S. government approached digital assets.

The order emphasized responsible blockchain innovation, support for U.S. dollar–backed stablecoins, and a firm rejection of central bank digital currencies due to privacy concerns. It rescinded restrictive Biden-era policies and established advisory groups tasked with shaping future digital asset regulation.

The market response was immediate. Bitcoin rallied approximately 25% in the first quarter, while total crypto market capitalization expanded by roughly 15%. Institutionally, the order eased banking integration for crypto services, contributing to decisions by firms such as Vanguard to open crypto ETF access to tens of millions of clients later in the year.

In a macro environment where U.S. CPI averaged 3.2% early in 2025, the order reinforced crypto’s narrative as a hedge against monetary debasement. Long-term, it positioned the U.S. as a competitive digital finance hub, reducing enforcement uncertainty and attracting offshore talent back to domestic market.

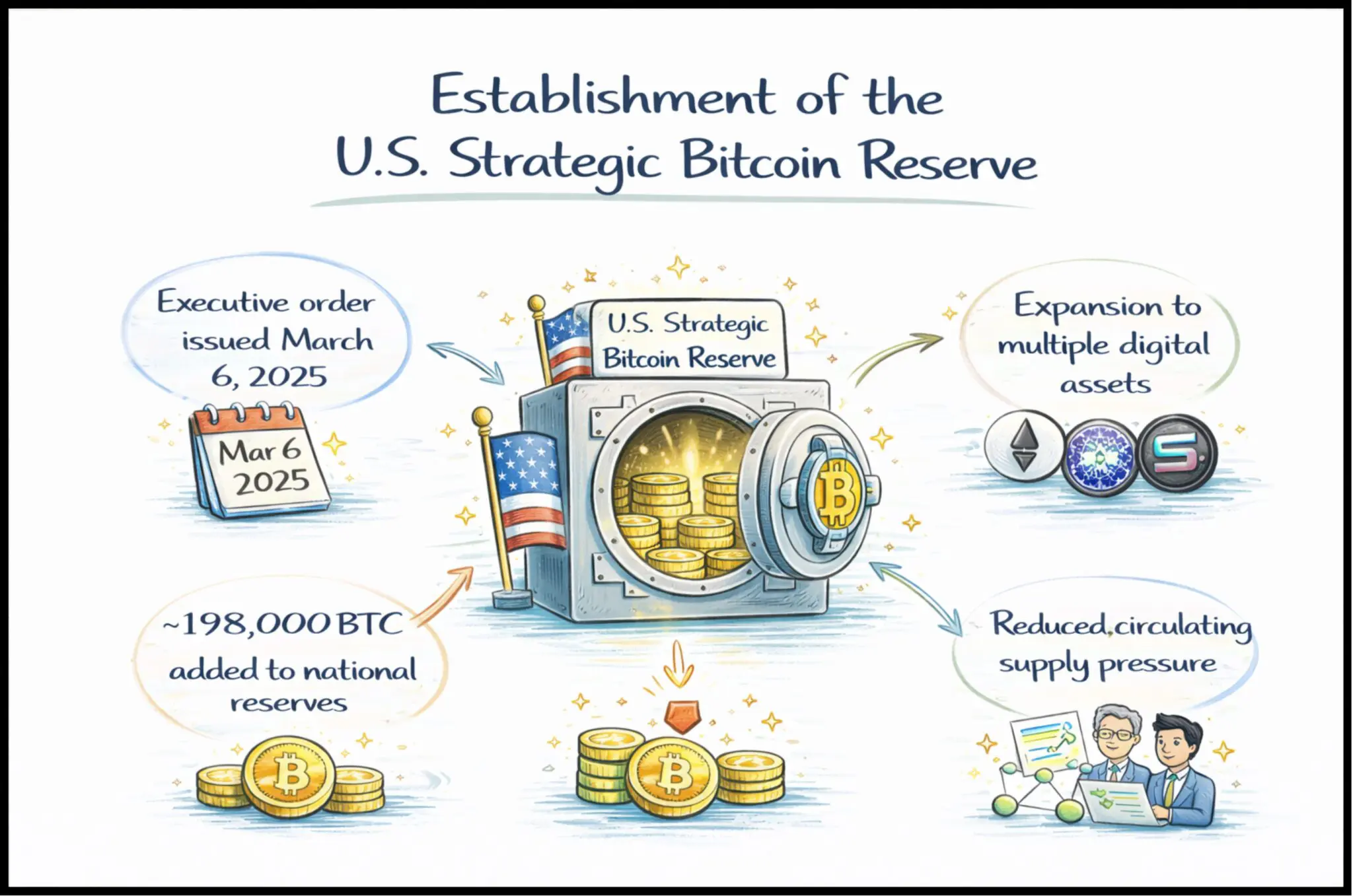

On March 6, 2025, President Trump issued an executive order creating the Strategic Bitcoin Reserve and United States Digital Asset Stockpile. The reserve incorporated approximately 198,000 BTC seized by federal authorities, reframing Bitcoin as a sovereign hedge against inflation and geopolitical risk. By mid-year, the reserve expanded to include other digital assets such as ETH, ADA, and SOL, reflecting a broader acknowledgment of crypto’s strategic relevance.

The announcement triggered a roughly 35% surge in Bitcoin prices in March, alongside record institutional inflows into spot ETFs. BlackRock’s IBIT fund alone approached tens of billions in assets under management. Macro alignment was reinforced by the IMF’s upward revision of global GDP growth to 3.2%, supporting risk assets broadly.

However, the reserve also exposed vulnerabilities, highlighted by a $15 billion Bitcoin seizure from a criminal operation later in the year. Strategically, the reserve intensified global competition and strengthened Bitcoin’s macro hedge narrative, contributing to its dominance surpassing 60% by year-end.

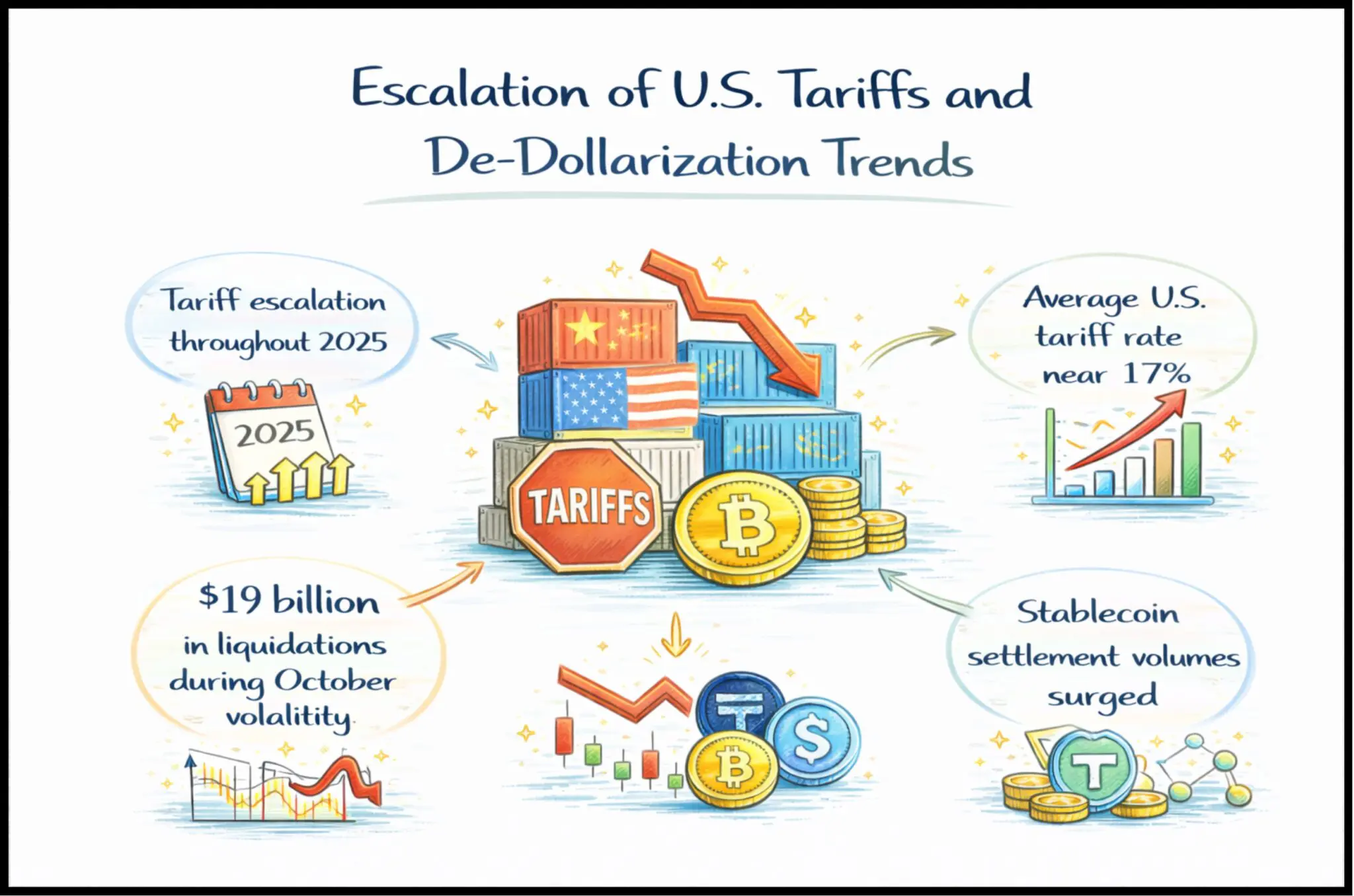

U.S. tariff policy escalated sharply in 2025, beginning in April and peaking in October with threats of 100% tariffs on Chinese imports and expanded software export controls. These measures pushed the average U.S. tariff rate toward 17%, reigniting global trade uncertainty. Crypto markets reacted with heightened volatility as tariffs amplified risk-off sentiment and equity market stress.

While tariffs contributed to the October 11 flash crash, they also accelerated de-dollarization trends. Stablecoin usage in emerging markets for cross-border settlements rose sharply, with monthly volumes reaching approximately $772 billion.

Macroeconomically, tariffs fueled inflation risks and raised projections of a U.S. GDP slowdown to 1.9% in 2026. Long-term, the episode demonstrated crypto’s dual role: vulnerable to global risk-off cycles yet increasingly valuable as neutral settlement infrastructure during trade fragmentation.

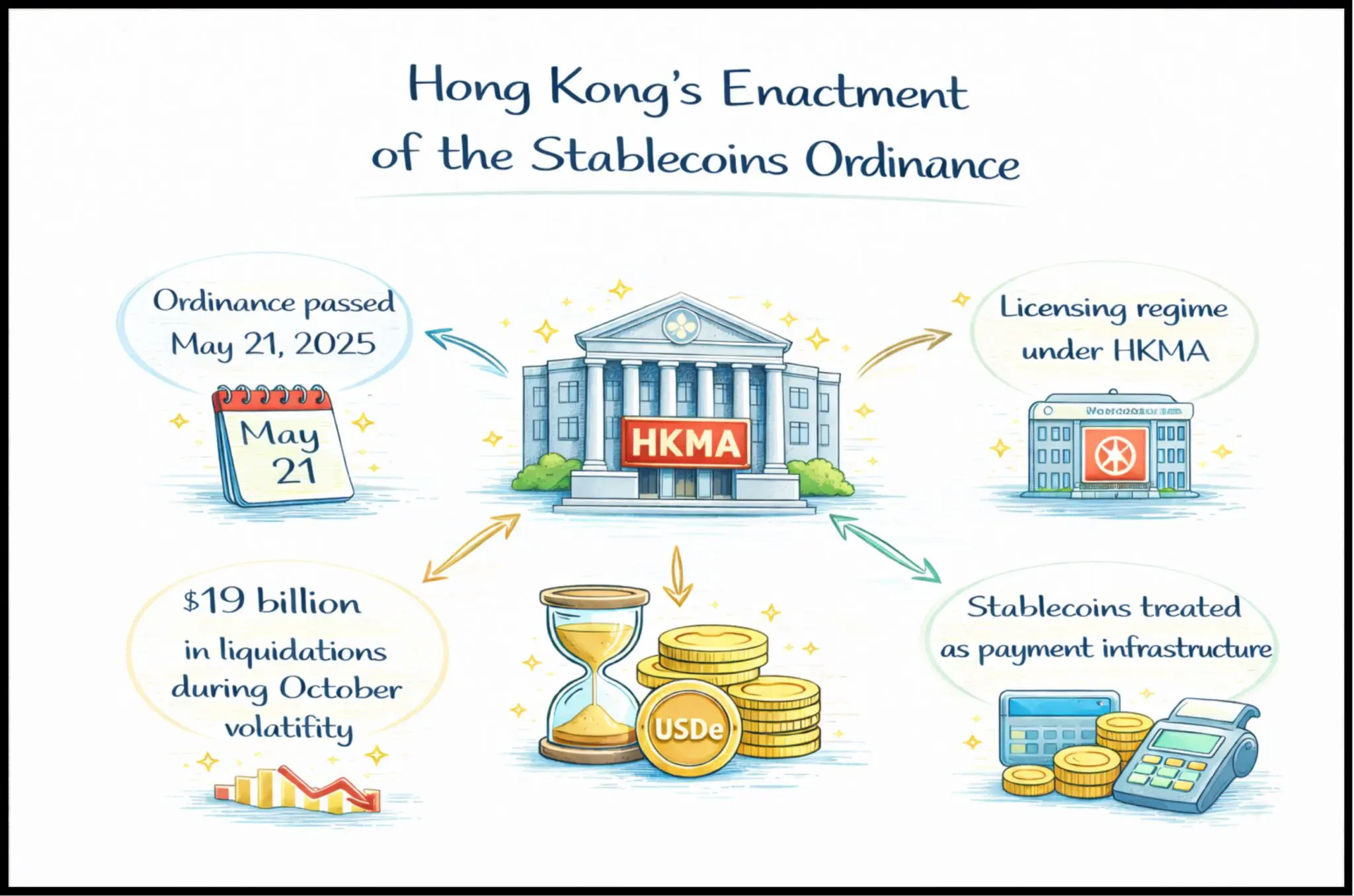

On May 21, 2025, Hong Kong’s Legislative Council passed the Stablecoins Ordinance, effective August 1. The law established a comprehensive licensing regime under the Hong Kong Monetary Authority covering stablecoin issuance, custody, and operations. A six-month transitional period allowed existing operators to comply while reinforcing stablecoins as regulated payment infrastructure.

The ordinance catalyzed a stablecoin expansion, with assets such as USDe reaching approximately $15 billion in market capitalization. It complemented U.S. legislation like the GENIUS Act and pushed global stablecoin transaction volumes to new highs.

In a macro context shaped by tariffs and currency fragmentation, Hong Kong’s framework positioned stablecoins as credible alternatives to traditional cross-border payment rails. By year-end, similar regulatory approaches began appearing in other jurisdictions, strengthening institutional trust.

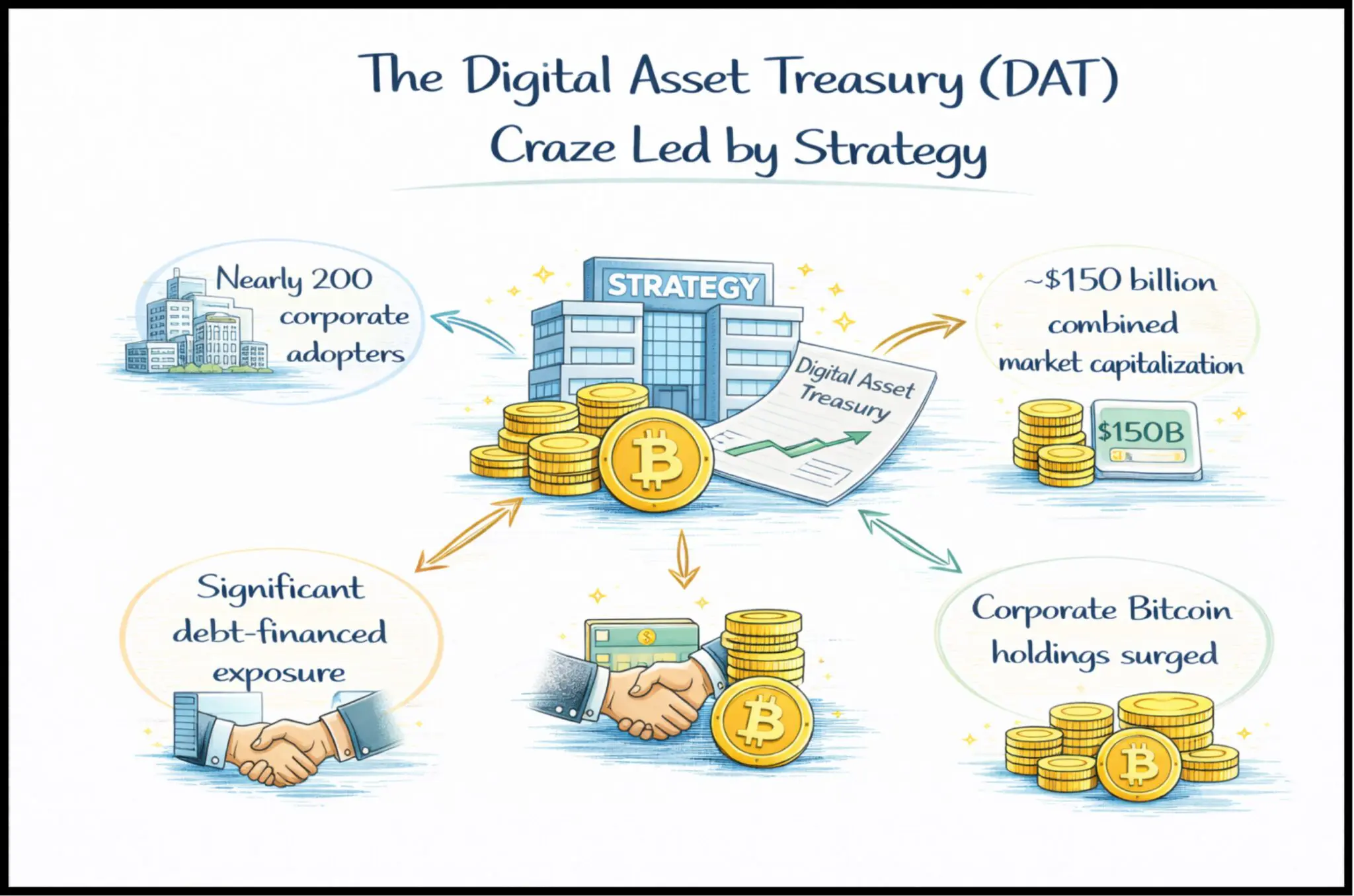

Strategy’s aggressive, debt-financed Bitcoin accumulation ignited the Digital Asset Treasury trend in 2025. Nearly 200 corporations adopted similar balance sheet strategies, collectively reaching approximately $150 billion in market capitalization by September. Public companies held an estimated 725,000 to 1 million BTC collectively.

The DAT trend legitimized crypto within corporate finance but introduced leverage and dilution risks. While it provided inflation hedging benefits during Fed rate cuts, it amplified downside volatility during market corrections, including a 15% sector drawdown in Q3.

The trend also bridged traditional finance and crypto, evident in tokenized real-world assets such as a $10 billion mortgage migration on-chain. By late 2025, valuations normalized, signaling maturation rather than abandonment.

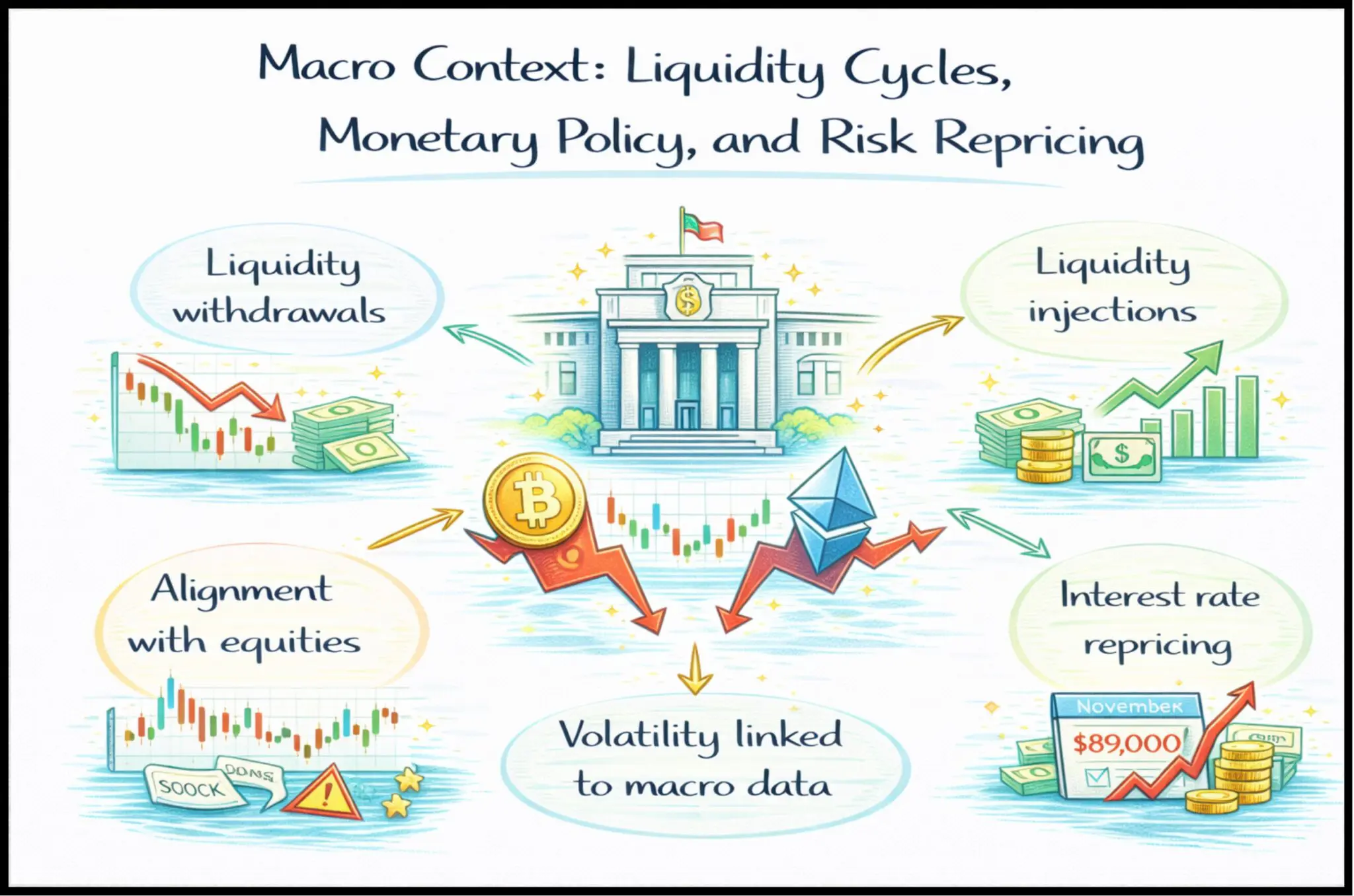

By 2025, cryptocurrency markets were no longer operating in isolation from global liquidity conditions. Monetary policy decisions particularly in the United States had become a primary driver of crypto price action, volatility, and capital flows. As inflation moderated into the low-to-mid 2% range, central banks gained room to adjust interest rates, shifting market expectations around risk assets broadly. Crypto responded not as an alternative system detached from macro forces, but as a high-sensitivity component within them.

This period marked a structural repricing of crypto’s risk profile. Bitcoin and large-cap digital assets increasingly moved in alignment with equities, credit spreads, and forward rate expectations, reflecting their growing integration into institutional portfolios. Liquidity injections and withdrawals transmitted more rapidly into crypto markets than in prior cycles, amplifying both upside momentum and downside drawdowns. As a result, volatility became less episodic and more continuous, driven by macro data releases rather than crypto-native catalysts alone.

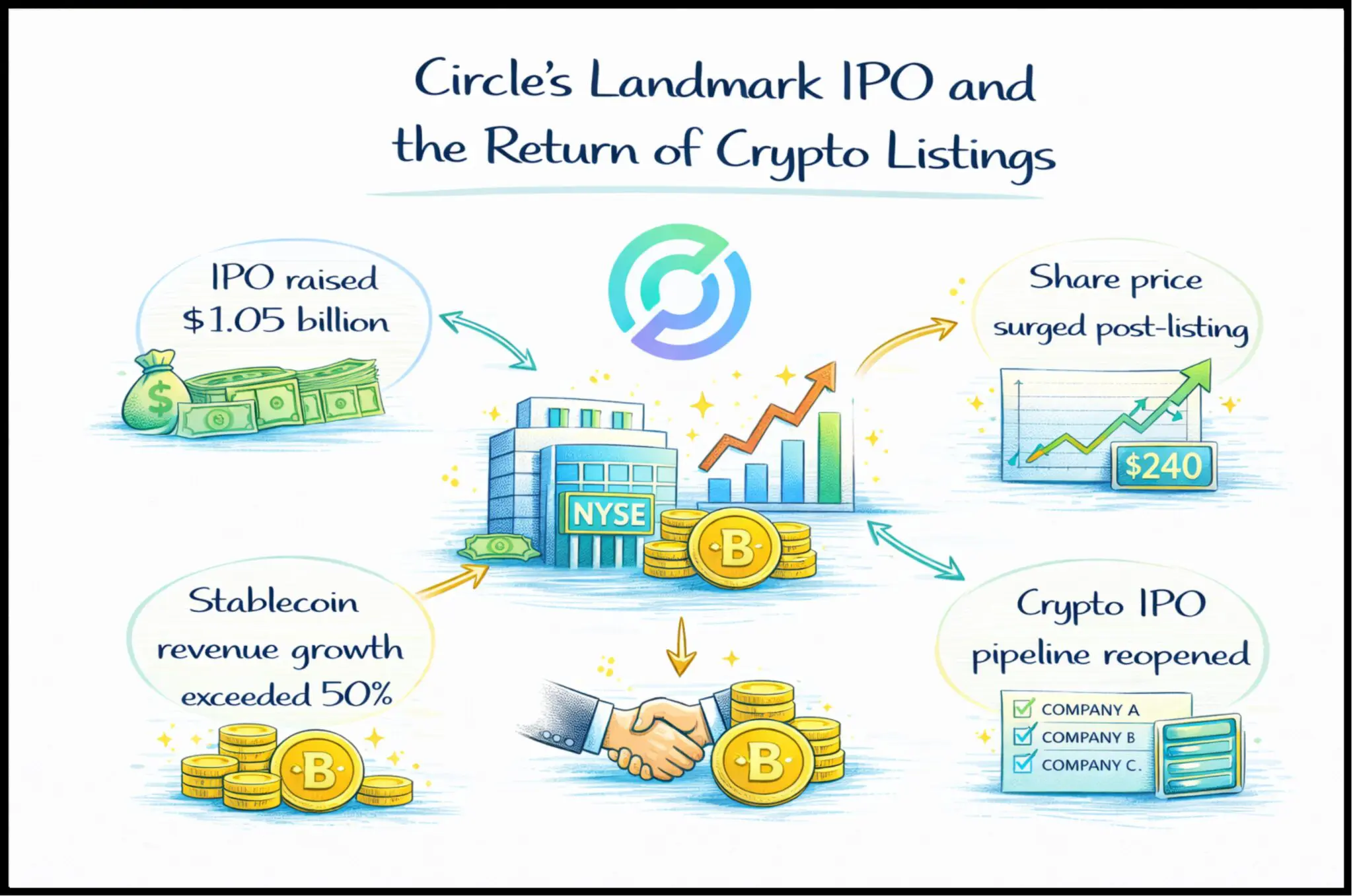

Circle’s initial public offering on June 5, 2025, marked a major reopening of traditional capital markets for crypto-native infrastructure companies. Listed under ticker CRCL, the deal was upsized to raise $1.05 billion at $31 per share, and Circle debuted on the NYSE before surging nearly 500% to $240 by mid-year. The IPO’s market impact extended beyond Circle itself, signaling that stablecoin issuers and crypto payment rails could be assessed through institutional valuation frameworks rather than purely narrative cycles.

The strategic importance of this event was not the early price spike, but the normalization of crypto infrastructure within public-market funding pathways. By tying stablecoin businesses to audited reporting, institutional investor access, and multi-quarter performance narratives, crypto’s capital cycle became more comparable to traditional fintech and payments firms. The year-end price level around $86 reflected a transition from momentum-driven repricing toward a more mature valuation regime.

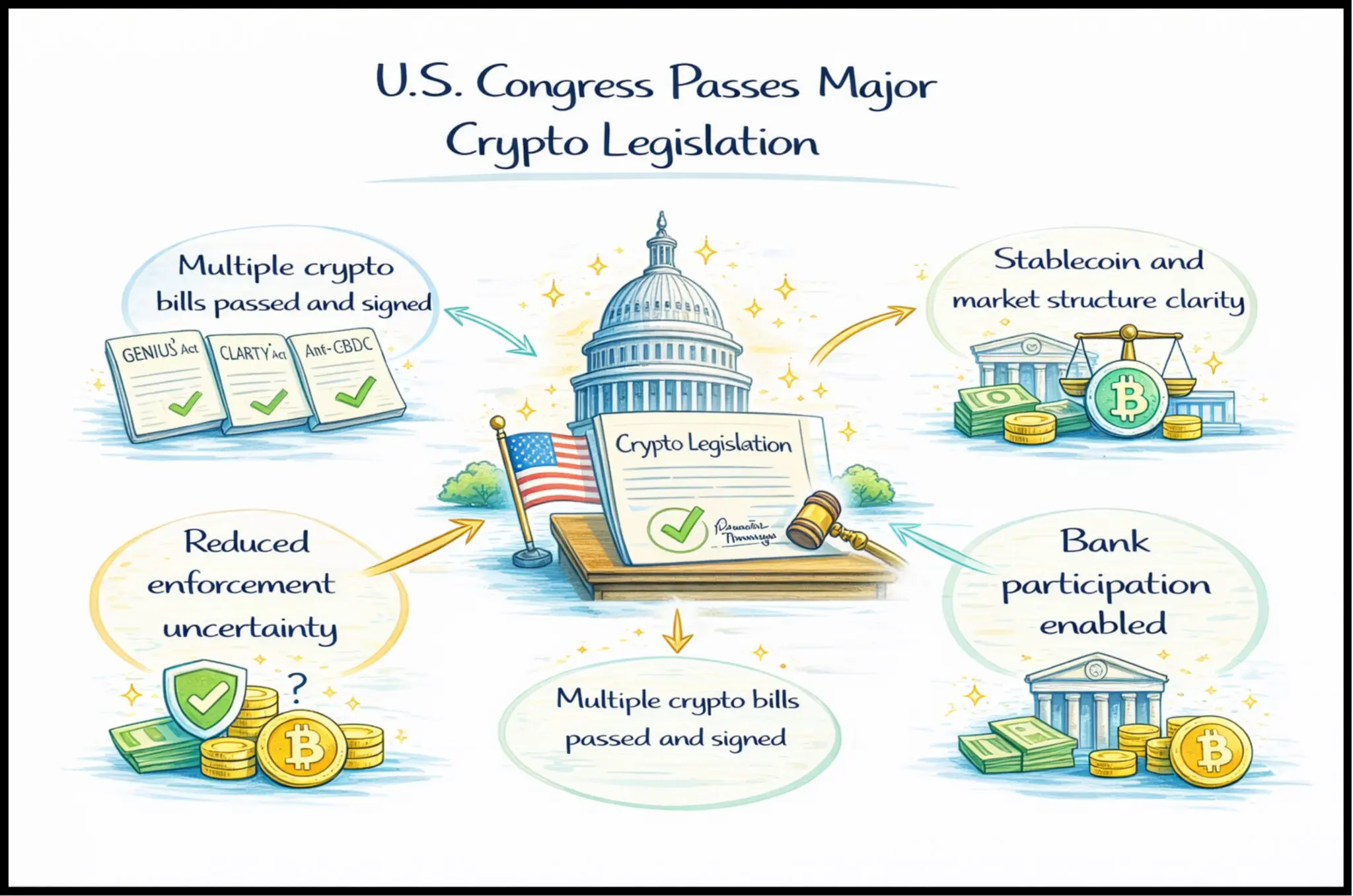

In July 2025, U.S. lawmakers delivered one of the most consequential regulatory packages of the cycle during “Crypto Week,” passing multiple bills that reshaped market structure and stablecoin oversight. The GENIUS Act established a stablecoin framework, the CLARITY Act delivered market structure clarity, and the Anti-CBDC Act codified opposition to central bank digital currencies; President Trump signed the package on July 18.

This legislative shift mattered because it moved the U.S. toward rules-based governance instead of enforcement ambiguity, reducing institutional hesitation. It also created a clearer pathway for banks and regulated intermediaries to engage with crypto rails under defined compliance expectations.

This event’s core contribution was structural predictability: market participants could price regulatory risk with greater confidence, and institutions could build product and custody strategies around clearer rules. Importantly, the legislation also dampened sensitivity to episodic enforcement shocks, even as macro volatility persisted through tariffs and changing rate-cut expectations. Over the long term, these laws positioned the U.S. as a regulatory leader and accelerated the integration of crypto services into mainstream financial distribution.

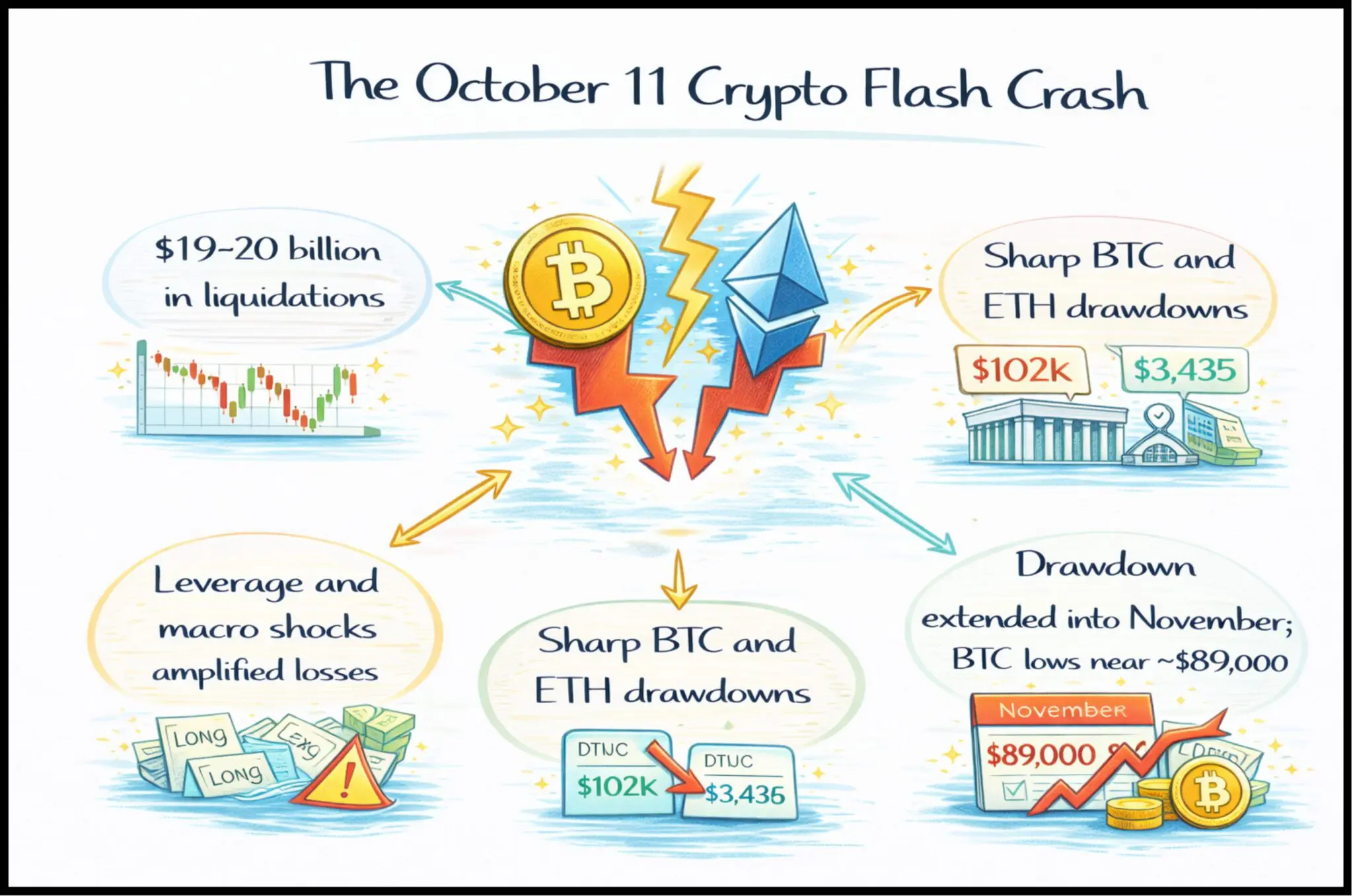

On October 11, 2025, crypto experienced its largest liquidation shock of the year. It was also one of the largest on record. An estimated $19–20 billion was liquidated within 24 hours. Bitcoin fell 12.7% to roughly $102,000. Ethereum dropped 14.3% to approximately $3,435. The selloff was linked to tariff-driven risk-off sentiment and elevated leverage. Broader equity stress also contributed, including declines in AI-related stocks. The move did not remain confined to one session. The downturn extended into November, with Bitcoin falling near $89,000. The episode served as a stress test for market structure. It showed how leverage can rapidly transmit macro shocks into cascading liquidations across venues.

The flash crash highlighted that crypto’s biggest vulnerability in 2025 was not adoption demand, but liquidity fragility under leverage. As macro uncertainty rose and rate-cut expectations shifted, crypto behaved more like a high-beta risk asset, with liquidation mechanics amplifying downside moves beyond what spot-only markets would imply. Strategically, this event strengthened the case for improved risk management, better liquidation design, and more resilient DeFi leverage systems as crypto scales into institution-sized flows.

Prediction markets re-emerged as a major crypto-adjacent growth category in late 2025, driven by Polymarket’s U.S. relaunch following CFTC approval on November 25. The category’s scale became difficult to ignore: Polymarket recorded volumes exceeding $3.74 billion in November alone, while Kalshi reached $5.8 billion, alongside a reported $8 billion valuation as products diversified beyond sports.

This mattered in 2025 specifically because macro conditions were unstable rate surprises, political risk, and trade tensions made forecasting valuable. In that environment, prediction markets positioned themselves as decentralized information tools with practical hedging and signaling utility.

The strategic importance here is utility expansion: crypto rails were being used to price real-world uncertainty rather than solely to speculate on token emissions. By integrating stablecoins and scaling infrastructure, prediction markets demonstrated a credible consumer-facing use case that intersected finance, media, and macro forecasting. Over time, the category’s durability will depend on regulatory alignment and market integrity, but 2025 established that demand exists at meaningful scale.

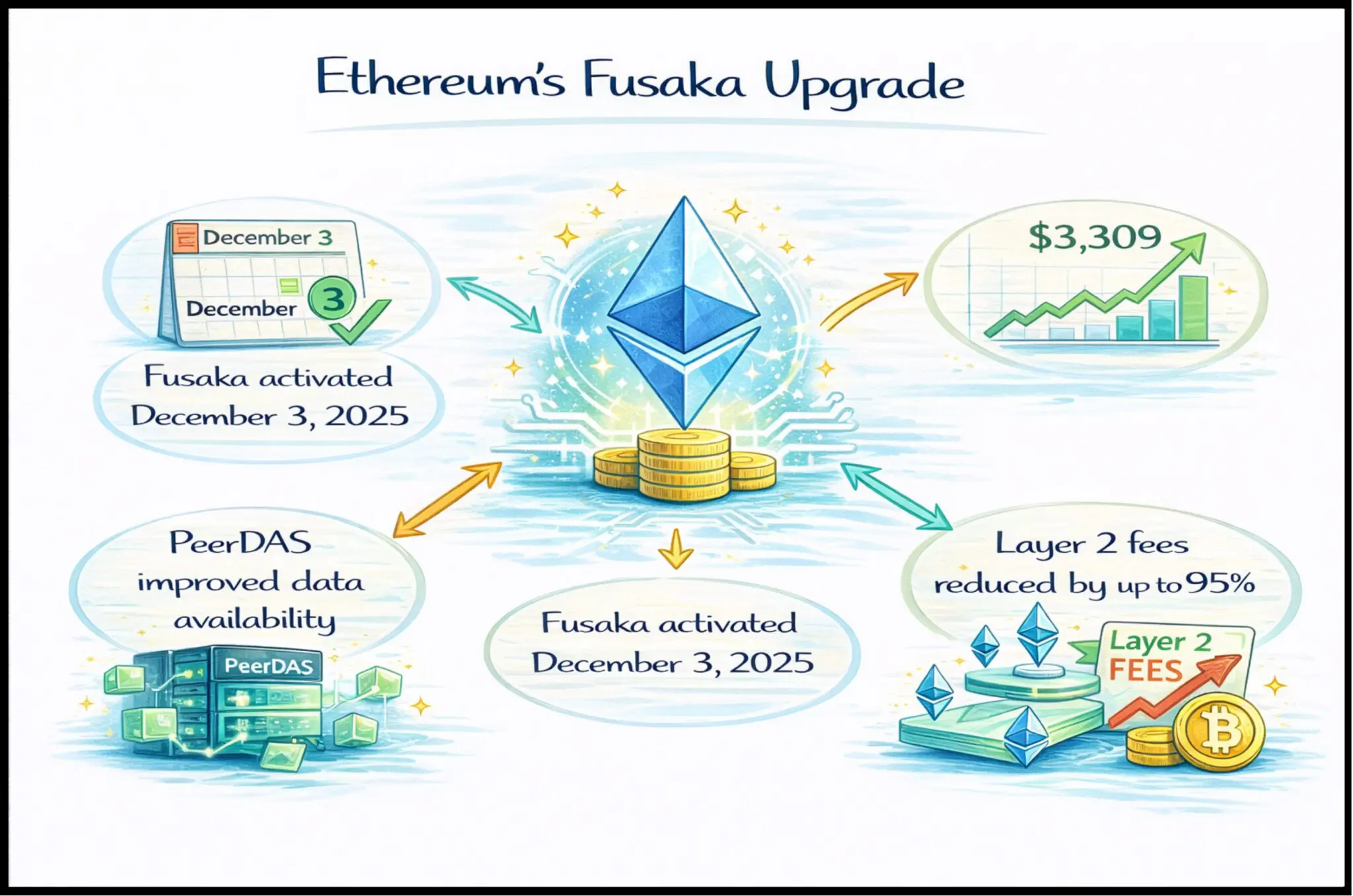

Ethereum’s Fusaka upgrade activated on December 3, 2025. It continued Ethereum’s modular scaling strategy. The upgrade focused on improving data availability and reducing costs for Layer 2 execution environments. It introduced PeerDAS for data availability and increased block gas limits. As a result, Layer 2 fees dropped by up to 95%.

Building on prior upgrades such as Dencun and Pectra, Fusaka reinforced Ethereum’s role as a financial-grade settlement layer. It further moved Ethereum away from a monolithic execution model. The upgrade also aligned with institutional narratives. In your text, Ethereum’s price action was linked to a move toward approximately $3,309. This movement coincided with a BlackRock staking ETF filing catalyst.

Fusaka mattered because it advanced Ethereum’s core strategic tradeoff: pushing execution to L2s while maximizing L1 settlement security and data availability. In the broader 2025 context AI acceleration, institutional integration, and energy constraints; this approach supports scalable onchain applications without requiring Ethereum to compromise its base-layer role.

The limitation is that modular scalability increases system complexity, but 2025 reinforced that Ethereum’s roadmap is optimized for durability and institutional-grade infrastructure rather than short-term throughput narratives.

Alongside macro forces, 2025 was defined by a decisive shift in regulatory posture across major jurisdictions. After years of fragmented enforcement and legal ambiguity, governments increasingly moved toward codified frameworks that treated digital assets as financial infrastructure rather than peripheral experiments. This did not eliminate regulatory risk, but it transformed its nature from existential uncertainty to operational and compliance-based constraints.

This transition reshaped institutional behavior. Banks, asset managers, and public-market investors began engaging with crypto through regulated vehicles, custody arrangements, and balance sheet exposure that required long-term risk assessment rather than short-term opportunism. The result was a deeper but more disciplined capital base, one that prioritized clarity, governance, and durability over rapid expansion. At the same time, regulatory alignment raised barriers to entry, compressing speculative excess while favoring entities capable of operating within formal financial systems.

The Top 10 Crypto Events That Shaped 2025 marked a structural turning point for digital assets. Crypto moved beyond cycles driven by speculative narratives. Instead, markets became governed by policy alignment, institutional balance sheets, and macroeconomic integration. Earlier periods linked crypto volatility mainly to internal market dynamics. In contrast, 2025 showed that external forces now dominate. Global liquidity conditions, trade policy, and legislative clarity exerted direct and sustained influence on crypto market behavior.

Regulatory developments in the United States and Asia reduced existential uncertainty for core crypto segments. These included Bitcoin, stablecoins, and settlement infrastructure. At the same time, regulators imposed higher expectations for compliance, transparency, and risk management. This shift changed the composition of market participants. Institutions became more deeply embedded in crypto markets. Corporate treasuries emerged as active holders. Public equity markets also reopened to crypto-native firms. However, leverage-driven instability and liquidity shocks persisted. The period showed that structural legitimacy does not eliminate systemic fragility, especially during macroeconomic stress.