Loading Ratings...

Comprehensive history of Tectum Cash Token (TCT): build-up, presale, launch, price crash, causes, team response, and current outlook.

Author: Sahil Thakur

Published On: Thu, 25 Dec 2025 03:43:44 GMT

TCT had a launch with big expectations and strong community hype. The team promoted innovation, speed, and a new vision for payments. At first, many investors saw the TCT launch as a chance to join a growing blockchain ecosystem. However, the story changed quickly. Soon after trading began, the token faced heavy selling. As a result, the price collapsed and confidence evaporated. The TCT crash shocked early supporters, raised serious questions about trust, and set the stage for a difficult recovery journey.

Tectum is a high-speed Layer 1 blockchain project. It promotes itself as the world’s fastest blockchain and uses Proof of Utility to support feeless, ultra-fast transactions. The platform focuses on SoftNote. This payment system uses digital cash notes. As a result, users can send Bitcoin and other crypto instantly with zero fees. The Tectum native token, TET, powers the blockchain. People use it to mint SoftNotes, pay network fees, and earn validator rewards.

In 2025, the team launched a second token called Tectum Cash Token, or TCT. It works alongside TET. While TET acts as the gas for the ecosystem, TCT focuses on utility and governance. The goal is to increase community engagement and connect user activity to platform growth. According to official descriptions, TCT links users to value created through real-world crypto payments via the SoftNote Wallet. In practice, TCT holders gain benefits. They receive voting rights on proposals. They also share revenue from SoftNote ePOS operations. In addition, they earn loyalty rewards such as cashback and discounts. They also get priority access to new features and drops. Over time, TCT may support DeFi integrations. It could serve as collateral for lending and borrowing. It can also work alongside TET in staking programs.

Before launching TCT, Tectum invested heavily in marketing and community building. The team hosted AMAs and published educational content like the Tectum 101 series. They also ran Galxe campaigns such as Diamond Hands and Learn and Earn to attract early supporters. Meanwhile, Tectum reported growth in its user base. It claimed more than 70,000 SoftNote Wallets and over 200,000 community members across social networks. This activity helped build excitement ahead of the token release. First, TCT became available inside the Tectum wallet. Early supporters could buy TCT at a discount using TET. This step encouraged ecosystem loyalty. The early presale priced TCT at 0.10 dollars. It included a strict vesting plan with no tokens unlocked at the token generation event. After a three-month cliff, investors unlocked 10 percent each month. Larger purchases made with TET received bonuses of up to 25 percent.

Overall, the road to launch featured bold technical claims and strong community messaging. The team framed TCT as the key to making the ecosystem both powerful and participatory. They emphasized sharing value with the community. Social posts highlighted Tectum’s speed and suggested that TCT holders could benefit from the DAO system. As a result, interest in the presale grew rapidly.

Tectum ran several presale rounds for TCT in November 2025. The public token sale began on November 18, 2025. At that point, the team opened TCT sales on multiple community launchpads such as KingdomStarter, Eesee, Kommunitas, and GemPad. Each platform offered allocations. According to reports, all rounds sold out quickly, often within 24 hours. In total, the presale raised more than 800,000 dollars from early buyers.

The public presale price remained 0.15 dollars per TCT across launchpads. Some platforms offered whitelist rounds. However, the price generally stayed consistent at 0.15 dollars during the crowd sale. Earlier private rounds through the SoftNote Wallet cost 0.10 dollars. That structure rewarded insiders with a lower entry price. Data suggests at least two IDO phases. One took place around November 25 to 26 and another from November 26 to 28. Both priced tokens at 0.15 dollars. One round raised roughly 300,000 dollars. Another added about 200,000 dollars. The remaining funds likely came from earlier sales.

At launch, circulating supply sat near 5 million TCT. This amount matched the public allocation of roughly 5.33 percent of the 100 million total supply. CryptoRank listed an initial market cap of about 750,000 dollars. That value aligns with a 0.15 dollar price and roughly 5 million tokens in circulation. Launchpad buyers usually unlocked 30 percent at the token generation event. They then received the remaining 70 percent gradually over four months. This structure gave investors some immediate liquidity. At the same time, it encouraged holding. The project also introduced a 24-hour refund window. Participants could exit if they changed their minds. Few appeared to use this option.

During the presale, Tectum pushed marketing aggressively. Launchpads promoted claims such as 3.5 million transactions per second. The team stayed active on Telegram and Twitter with frequent updates. Meanwhile, Galxe challenges rewarded holders who kept their allocation until listing. The core message focused on revenue sharing through SoftNote activity. TCT, according to the narrative, allowed holders to participate directly in that value. Many investors responded positively. Several reports stated that public enthusiasm remained high and that launchpad allocations sold out quickly. By the end of November, Tectum had created a large, energized community waiting for the token to list.

The Tectum Cash Token officially launched for trading at the start of December 2025. The first public listing occurred on December 1, 2025 on Uniswap (Ethereum mainnet) . The team announced via social media that “$TCT is now officially LIVE on @Uniswap… The day we all have been waiting for is here!” . This DEX launch allowed early contributors and new traders to swap TCT freely.

Initial market cap & supply: At launch, TCT’s price hovered around the presale level. In fact, it “quickly reached a price near $0.15” in early trading . With ~5 million tokens circulating, this translated to an initial circulating market cap around $750,000 (as previously projected) . The fully diluted valuation (FDV) at $0.15 was about $15 million (100M max supply) . According to the project’s tokenomics, liquidity was provided to facilitate trading – 10% of the supply (10 million TCT) was allocated to liquidity .

The Tectum team likely locked a portion of these tokens in the Uniswap pool alongside ETH/USDT to bootstrap liquidity (and indeed they later emphasized that liquidity was locked). Initial liquidity depth isn’t explicitly reported, but given the modest market cap, it was likely on the order of a few hundred thousand dollars in the Uniswap pool. Notably, on-chain data shows the team did lock the Uniswap LP tokens, as no rug-pull of liquidity occurred (the price crash came from selling tokens, not removing liquidity).

Exchange listings: Following the Uniswap debut, Tectum pursued centralized exchange listings. Just days after the DEX launch, on December 4, 2025, TCT was listed on MEXC. MEXC announced the listing in their Innovation Zone, with trading of the TCT/USDT pair opening Dec 4 at 12:00 UTC . This provided a more accessible venue for users not familiar with Uniswap. Tectum had hinted at “multiple crypto markets” for TCT – press releases noted plans for “several centralized exchanges on December 2” , though in practice MEXC was the primary CEX to list it in that first week. (It’s possible others were planned or slightly delayed; as of this report, no evidence of another major exchange listing TCT in December 2025 has surfaced beyond MEXC.)

The Uniswap and MEXC listings were significant milestones for the project. The team celebrated the Uniswap launch as “a significant step to give broader crypto users the ability to enter the Tectum ecosystem” . Likewise, they hyped the upcoming MEXC listing as the first of many, tweeting a teaser on Dec 2: “Huge $TCT news dropping soon… we have our very first CEX listing lined up for later this week! Can you guess which one?” . This generated excitement and speculation within the community.

Initial trading and momentum: In the very first hours of launch on Dec 1, TCT saw a brief surge above the listing price. According to one analysis, TCT “launched on December 1 at a listing price of $0.20, but was quickly sold off by presale investors taking profits” . In other words, early trades on Uniswap saw the price spike to about $0.20 (around +33% from the presale price), then retreat once some initial holders unloaded.

The price floor on day one fell to roughly $0.14 before stabilizing . By December 3, on the eve of the MEXC listing, TCT had climbed back up to around $0.156 – essentially back near its launch value. At that point the Fully Diluted Market Cap was ~$15–16 million, and the on-chain holder count was extremely low – only ~164 holders on Ethereum as of Dec 3 . This indicated that ownership was still highly concentrated (mostly the presale buyers and perhaps the team’s own wallets).

Low volume concerns: One red flag in the launch week was the lack of trading activity. Volume on Uniswap was quite tepid after the initial launch rush. On December 3, data from GeckoTerminal showed only about $47.5K in 24h trading volume. The limited volume suggested that outside demand for TCT was weak once the initial community had taken positions. This low liquidity environment would set the stage for volatility ahead. (See figure below), which illustrates TCT’s price and volume during its first two days of trading on Uniswap – after an initial pop to ~$0.16–0.17, the price drifted with minimal volume, reflecting a lack of broader market engagement.

By mid-December, TCT reached its all-time low near 0.015 to 0.016 dollars. That drop represented about a 90 percent decline from the 0.15 dollar IDO price. Early price peaks stayed modest. Instead, the chart showed a sharp crash, followed by only a weak recovery. By late December, TCT traded in the 0.01 to 0.02 dollar range. At that level, the price sat more than 90 percent below its peak. The fully diluted market cap hovered near only 2 million dollars.

Timing and severity: The crash came quickly and hit hard. It started right after the MEXC listing on December 4, 2025. Then it unfolded over roughly one week. Within just three to four days, the price fell from the mid-teens cents into the low single-digit cents. By mid-December, TCT had lost about 93 percent of its value from launch. In simple terms, the token moved from around 0.15 dollars to roughly 0.016 dollars by December 10 to 12. The market nearly wiped out in days. Even in crypto, where volatility is common, this drop looked extreme. Not surprisingly, the community reacted with anger and fear.

How it unfolded: Analysts and the team agreed on a core trigger. A large holder began selling aggressively. Shortly after trading opened on MEXC, traders noticed a huge wave of TCT hitting the market. On-chain data traced the selling to an address tied to someone close to project leadership. Community members argued that this wallet sold far more tokens than any normal presale buyer could have accessed. Vesting should have limited that supply. Those tokens should have remained locked. Yet the seller still managed to move and liquidate them. Some claimed that the seller was described as a family member of the CEO (not confirmed). The alleged insider offloaded a massive amount of tokens. As a result, buy support vanished and the price collapsed.

Once that selling started, panic spread. Retail holders saw the sharp decline and rushed to exit. That reaction added even more downward pressure. Meanwhile, price slippage on MEXC spilled into Uniswap through arbitrage. Soon both the centralized and decentralized markets dropped together. Liquidity remained thin, so each sell order hit harder. Orders drained the books. When the price broke below five cents, automatic stop-loss trades likely triggered. The fall accelerated. Within a week, the token moved from roughly a 15 million dollar fully diluted valuation to near 1 to 2 million dollars.

Technical vs. community-led causes: The crash did not stem from an outside hack or a technical failure in the blockchain. Instead, it reflected trust failure and poor allocation controls. On the technical side, the vesting system clearly failed. Tokens meant to remain locked somehow became tradable. That issue might point to flawed smart contract controls. Or it could reflect a manual process handled off-chain. On the human side, an insider chose to sell. Whether motivated by profit, fear, or internal conflict, the decision broke trust. The broader crypto market at the time stayed relatively stable. Therefore, TCT’s collapse appeared isolated and tied mainly to internal token management.

Very quickly, the community recognized that this was not just a normal presale dump. Presale investors usually face strict vesting. Here, the size of the selling signaled insider access. Many holders began calling it a mini rug pull. Discussions on Reddit and Telegram questioned whether the team had betrayed its own supporters. Technically, liquidity stayed in place, so it did not meet a classic rug pull definition. However, the effect felt similar. One person claiming to be a former employee accused leadership of selling at peaks and lacking ethics. These claims remain unverified. Still, they show how deeply the crash damaged confidence.

In objective terms, mismanagement and insider behavior clearly contributed. We do not know whether the insider acted maliciously. Yet we do know that proper safeguards did not exist. The vesting promise failed internally. Furthermore, some users linked this incident to older controversies involving Tectum’s TET token. They believed both cases showed a pattern. In their view, the project did not consistently protect investor interests.

The responsibility for TCT’s crash appears to rest mainly with internal mismanagement. It may also involve insider misconduct. The available evidence points to several factors.

Insider token dump: As discussed earlier, a trusted associate of the core team dumped a large stash of tokens. The team confirmed that the seller was someone close to leadership. This means leadership either neglected safeguards or allowed these tokens to become liquid at launch. That individual should not have had tradable tokens at that stage. Whether the person was a relative of the CEO or another insider, the result looked like an inside job. The crucial issue is that these tokens were supposed to be locked. They were not. This failure suggests that the vesting system broke down. The allocation plan may have included loopholes. Or the team locked some allocations informally, which made them easy to exploit.

Lack of internal controls: The event also exposed weak controls inside Tectum’s token management. If one person could sell enough tokens to crash the price by about 90 percent, then custody was not secure. Many projects use multi-signature wallets and third-party locking services. These help ensure that no single person can move team or advisor tokens. If Tectum skipped those protections and relied on personal trust, that choice amounted to serious mismanagement. Not surprisingly, community members raised broader questions about governance, trust, and oversight afterward.

Possible breach of trust or ethics: Some investors accused the team of outright fraud. The team said a rogue insider betrayed them. Skeptics wondered instead whether leadership enabled the behavior or even encouraged it. A Reddit post by a supposed former employee accused the CEO of unethical conduct. The post claimed that leadership had previously dumped tokens and ignored security concerns. We cannot confirm those claims. Yet the perception looked terrible. At best, leadership appeared negligent. At worst, complicit. Many angry investors began using the word rug pull. Technically, liquidity stayed locked, so it did not match the textbook definition. However, the effect still felt similar. Insiders appeared to profit while regular holders absorbed heavy losses.

External factors: There is little sign that outside forces caused the crash. The broader crypto market stayed fairly stable during that period. No exploit or technical breach was reported. The contract functioned normally. Therefore, all signs point to an internal choice or failure.

In summary, the responsibility sits with Tectum’s team and insiders. The failure to enforce vesting locks shows clear mismanagement. Moreover, the situation strongly suggests insider abuse. Someone with privileged access sold tokens for personal gain, fully aware of the likely consequences. The community reacted by demanding accountability. Many investors accused the team of negligence or fraud. The reputational hit was serious. Trust in both competence and honesty collapsed. Even if one accepts that a rogue insider acted alone, leadership still failed to protect the project.

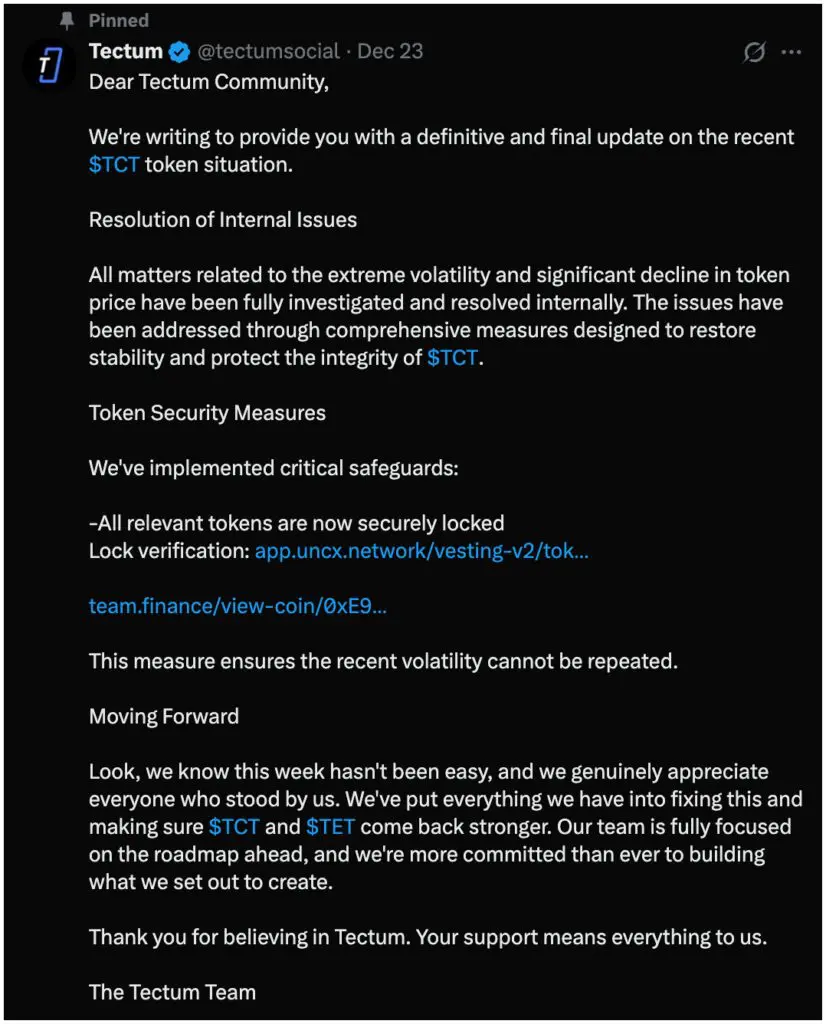

Initial response: The Tectum team eventually addressed the crisis. They did so after several days of rising pressure from the community. On December 11, 2025, they released a public statement. In that message, they confirmed that the sell-off came from someone close to the core team. They described the incident as unexpected. They also said they were negotiating to repair the damage. This likely meant they were speaking with the seller to recover funds or apply another remedy. However, the initial explanation contained few details. As a result, the community continued to worry.

Decisive actions: By December 22, 2025, the team issued what they called a final and definitive update. They shared it across their official channels. In that update, they described several actions.

Internal investigation concluded: They stated that their investigation had finished. They claimed to have identified all relevant wallets and tokens.

Locking of tokens: Next, they said that all tokens connected to the incident were now securely locked. They also shared on-chain proof through published transaction links. In practice, this likely involved moving team and treasury tokens into time-lock or vesting contracts. The move came after major damage. Still, it helped prevent further dumping.

Additional safeguards: The team also announced new safeguards. They said they wanted to ensure that similar events could not occur again. They did not share technical details. However, these safeguards probably include multi-signature rules, stricter vesting systems, and better monitoring tools.

Continued commitment: Finally, the team reaffirmed its commitment to the roadmap. They thanked loyal supporters and promised renewed focus on delivery.

This update arrived about three weeks after launch. It attempted to close the chapter. The tone acknowledged internal problems while framing them as a one-time issue. The team also engaged in more public communication. Moderators responded in Telegram chats. Meanwhile, official accounts highlighted progress and positive news. The goal was to stabilize emotions and reset expectations.

Promotion and recovery efforts: Around late December, Tectum also joined a New Year promotional campaign with MEXC. This included trading events and incentives. The move signaled that MEXC still supported the project in some capacity. Meanwhile, the team shifted attention back to technical progress. They promoted upcoming upgrades, app features, and wallet integrations. The broader message became clear. They wanted holders to believe that development continued and value could still grow over time.

Community reception of response: The reaction was mixed. Some investors felt relieved that the team acknowledged the issue and locked affected tokens. Transparency helped a bit. However, skepticism remained widespread. Several observers argued that the fixes did not address the deeper trust problem. Some users also noted that the team did not reveal the insider’s identity. They also saw no compensation for holders. To them, this looked like a case where the offender walked away, while the community held the losses.

In short, the team increased transparency and tightened controls. They tried to rebuild trust through communication and action. Yet the long-term effectiveness of these steps remains uncertain. Many community members continue to watch carefully before granting renewed confidence.

The team later also revealed all the wallet addresses linked to the crash:

Affected Wallet Addresses:

1) 2,950,000 $TCT https://etherscan.io/address/0xd65d2bB4043422471Db74dA8533af78531633794

2) 488,000 $TCT https://etherscan.io/address/0xf0003084c44f696a449f6bab6f846e76be1f3a8b#tokentxns

3) 595,000 $TCT https://etherscan.io/address/0x3546664cb0c52ef5ec381c9254acb691833648ee#tokentxns

4) 595,000 $TCT https://etherscan.io/address/0xf64d93f7dbb5737d7d6545474661fbcfdd8c950d#tokentxns

5) 403,000 $TCT https://etherscan.io/address/0x3743ee8fed907442c6187b5c600c602c8ddf5de7#tokentxns

6) 2,052,000 $TCT https://etherscan.io/address/0xF0E3cA9631dE4C87138F7714F11A766615B6bCaF#tokentxns

By the end of December 2025, the Tectum project still operated. However, it now faced a difficult road back.

Token price and market status: TCT trades around 0.01 to 0.02 dollars. This marks a small recovery from the absolute bottom. Still, it remains roughly 90 percent below launch price. The fully diluted valuation sits near 1 to 2 million dollars. Daily volume stays moderate. Traders still speculate, but long-term confidence remains weak.

On-chain data: Total supply remains at 100 million TCT. No burns have taken place. Holder counts increased since launch. Many small wallets bought during the price collapse. However, concentrated holdings still dominate. Team-controlled addresses remain among the largest, although many are now locked.

Exchanges and liquidity: TCT remains live on Uniswap and MEXC. No major exchanges added new listings after the crash. Liquidity pools remain small, so price can swing sharply. MEXC supports trading, yet volumes depend heavily on market makers. Future listings may require a sustained recovery in trust.

Project updates and roadmap: The team continues to emphasize development. They still promote plans for DeFi use cases, lending platforms, and ecosystem growth through 2026. They also maintain educational content and marketing efforts. On the surface, the project infrastructure remains intact.

Community sentiment: Sentiment now feels cautious. Many early supporters feel betrayed. Others argue that the technology still holds potential. Conversations online have slowed. Moderators continue to fight misinformation and frustration. Rebuilding morale will likely take time.

Roadmap status: It is still too early to judge final outcomes. If the team delivers real product adoption and measurable results, sentiment could improve. If progress stalls, confidence may erode further.

In conclusion, TCT remains active but damaged. The token trades. The project builds. Yet enthusiasm is gone. From here, recovery depends on execution and transparency. Over time, TCT may evolve into a redemption story. Or it may fade into another example of how fragile trust can be when internal systems fail.